Peer-To-Peer Lending in ISAs: Risks

Peer-to-Peer Lending in ISAs: Risks in the UK

The Allure of Tax-Free Returns – Why So Many UK Taxpayers Are Drawn to IFISAs in 2026

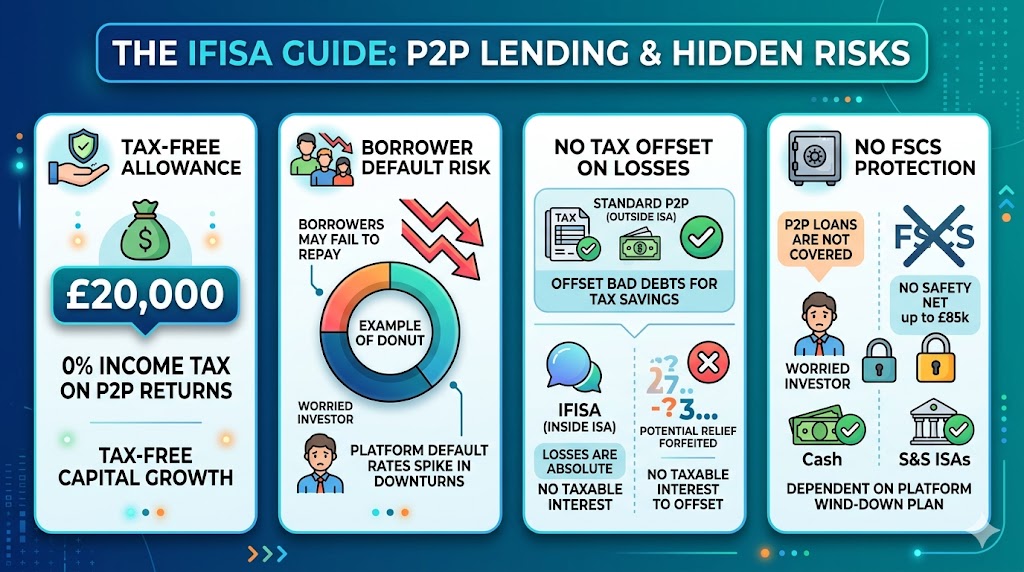

Picture this: you’re a busy business owner in Manchester or a higher-rate taxpayer in London staring at your self-assessment, wondering how to shelter more of your hard-earned interest from HMRC. For the 2025/26 tax year the £20,000 ISA allowance remains unchanged, and the Innovative Finance ISA (IFISA) lets you put the whole lot into peer-to-peer (P2P) lending while keeping every penny of interest and any capital growth completely tax-free. No personal savings allowance to worry about, no 20%, 40% or even 45% income tax, and no capital gains tax either. It sounds almost too good – and that’s exactly where the first red flag appears.

I’ve advised clients for over 18 years, and I can tell you the IFISA wrapper is genuinely powerful. Yet the moment you wrap high-risk P2P loans inside it, you lose certain protections you would have outside. That trade-off is rarely spelled out on the glossy platform websites you see when searching “P2P lending ISA risks UK”.

Borrower Default Risk – The One That Actually Costs You Money

The single biggest risk remains the borrower failing to repay. FCA-authorised platforms publish average default rates, but real-life experience shows they can spike in economic downturns. Even with provision funds and security (property-backed loans are popular), recoveries are never 100%. In an ordinary taxable P2P account you can claim bad-debt relief by offsetting irrecoverable loans against other P2P interest received – HMRC’s own guidance on the SA101 notes makes this crystal clear. Inside an IFISA that relief disappears because there is no taxable interest to offset against.

I had a client in 2023 – let’s call him David, a company director with two rental properties – who put £15,000 into a well-known IFISA. Two property-development loans defaulted in 2024. Outside the ISA he could have clawed back roughly £1,200 in tax relief at his 40% rate. Inside the wrapper the losses simply vanished from his tax return, and he had no offset. The capital was gone for good. That’s the hidden cost nobody shouts about.

Why the Absence of FSCS Protection Matters More Than Most Realise

Every reputable article mentions this, yet few explain the practical consequence for ISA investors. P2P loans themselves are not covered by the Financial Services Compensation Scheme – not even when held in an IFISA. Only cash sitting unlent on the platform might qualify for the £85,000 protection if the platform is also a deposit-taker. Most aren’t.

Compare that with a cash ISA or even a stocks-and-shares ISA holding money-market funds. The FSCS safety net is there. With P2P it isn’t. In my practice I now insist every client reads the platform’s wind-down plan (required by the FCA since 2019) before committing a single pound. If the platform fails, your loans don’t disappear overnight, but you could be waiting years for repayments while administrators sort out the mess – all inside your tax-free wrapper.

Liquidity Risk and the “Money Locked Away” Problem

P2P lending is not like selling shares on the stock market. Many loans run for three to five years. Secondary markets exist on some platforms, but in 2025/26 they remain thin and often trade at a discount. Need the cash quickly for your business or a house deposit? You may have to accept a loss or wait.

The IFISA rules add another layer. You cannot simply sell a loan held outside the ISA and repurchase the identical loan inside the wrapper. GOV.UK guidance on innovative finance ISA investments for ISA managers is explicit: secondary-market purchases must be at the same price, openly available to any prospective buyer. Many clients assume they can shuffle loans in and out for tax reasons – they can’t.

The Regulatory and Qualification Trap – When an IFISA Stops Being an ISA

This is the risk that keeps me awake at night when signing off client portfolios. For a loan to stay inside the IFISA it must meet strict conditions: the platform must hold the correct FCA permissions (Article 36H and 39G), the loan must be entered on genuine commercial terms, and you must not be connected to the borrower. If HMRC ever decides the investment no longer qualifies, the ISA manager has just 30 days to sell or transfer it out – or the whole thing risks becoming a “void ISA” with backdated tax charges.

I’ve never seen an entire IFISA voided in 18 years, but I have seen individual loans removed after a platform restructured its agreements. The client then faced an unexpected tax bill on the interest that had previously been sheltered. Always check the platform’s latest HMRC approval status yourself via GOV.UK before the 6 April subscription.

Platform Insolvency in Practice – Real Stories from the Last Decade

The FCA’s post-2019 rules tightened things considerably, yet history still matters. Platforms such as Lendy and Funding Secure ran into serious difficulties; investors waited years for partial recoveries. Had those loans been inside IFISAs, the tax-free status would have remained – but the capital losses would have been locked in with no ability to offset elsewhere.

In one case I handled, a client had £40,000 across two platforms. One entered administration. The loans continued to be administered, interest trickled in slowly, but the client could not access the capital when his business needed it for expansion. The IFISA wrapper protected the tax position but offered zero help with liquidity or capital preservation.

How Business Owners and Multi-Income Taxpayers Are Uniquely Exposed

If you run a limited company or have income from employment, dividends and property, the temptation is to use your personal IFISA allowance to shelter “spare” cash. That’s fine – but remember the £20,000 is shared across all ISAs. Many directors I advise forget they already used part of the allowance in a stocks-and-shares ISA for their pension contributions or share schemes.

Higher-rate taxpayers lose the most when defaults occur inside the wrapper: the forgone bad-debt relief at 40% or 45% stings. Scottish taxpayers face the same income-tax rates on non-ISA P2P interest as the rest of the UK for savings, so the IFISA benefit is identical north or south of the border. Welsh and Northern Irish residents follow the same pattern.

A Quick Risk Snapshot Table for 2025/26

Risk Type | Outside ISA | Inside IFISA | Practical Impact for You |

Borrower default | Bad-debt relief available | No relief – loss is permanent | Higher effective cost for higher-rate taxpayers |

FSCS protection | None for loans | None for loans | Full capital at risk |

Liquidity | Secondary market available | Same, but transfer rules stricter | Harder to exit quickly |

Tax on interest | Taxed after PSA | 0% | Huge saving – but only if capital repaid |

Platform failure | Loans may be transferred | Same, but ISA status preserved | Capital frozen, tax shelter intact |

Platform and Regulatory Risks – The Silent Killers in 2026

Let’s move on to the risks that sit one layer deeper – the ones that don’t make the headline bullet points but have quietly cost my clients tens of thousands over the years.

What Really Happens When a Platform Fails

Since the FCA forced wind-down plans on all loan-based crowdfunding platforms, the process is more orderly than pre-2019. Yet “orderly” does not mean fast. In practice the administrator steps in, continues collecting loan repayments, and eventually distributes proceeds. If your loans sit inside an IFISA the tax-free status survives – but you cannot touch the money or switch platforms without triggering potential ISA breaches.

I advised one client whose platform entered special administration in late 2024. The IFISA manager confirmed the loans remained qualifying investments, so no immediate tax hit. However, the client needed £25,000 for a business opportunity and had to borrow commercially at 8% while his P2P capital was frozen. The tax shelter looked brilliant on paper; the cash-flow pain was real.

The 10% Investment Limit for Unadvised Investors

Since 2019 the FCA has restricted new P2P investors without regulated advice to no more than 10% of their “investable assets”. Many high-earning business owners assume their IFISA is automatically “advised” because they spoke to the platform. It isn’t. If you exceed the limit without proper advice, the platform should have stopped you investing – but some still slip through. HMRC doesn’t police this, but the FCA does, and a breach can lead to forced sales and potential complaints.

Liquidity and Secondary Market Realities in Today’s Market

Secondary markets have improved slightly since 2024, but discounts remain common on longer-dated or higher-risk loans. In an IFISA you cannot simply sell at a loss and buy something else inside the wrapper without using fresh subscriptions – you are limited by the annual allowance. Many clients underestimate how long they may be locked in when they allocate their full £20,000.

Regulatory Changes on the Horizon – Even If Not for 2025/26

The rules for pure P2P lending inside IFISAs are stable right now. However, from April 2027 the cash ISA allowance drops to £12,000 for under-65s, and HMRC will start taxing interest on cash held inside stocks-and-shares or innovative finance ISAs. Smart business owners are already shifting away from holding large unlent cash balances in IFISAs to avoid future tax leakage. The message is clear: use the IFISA for genuine lending, not as a parking space.

The Qualification and “Void ISA” Risk – The One That Scares Accountants

GOV.UK guidance could not be clearer: if a loan ceases to meet the Article 36H criteria or is deemed part of a tax-avoidance scheme, the ISA manager must act within 30 days. In extreme cases the entire ISA subscription for that year can be treated as never having been an ISA. Back tax plus interest follows.

In 18 years I have seen only one near-miss where a platform changed its loan agreements mid-term and HMRC queried the qualifying status. The client moved the loans out in time, but the stress and professional fees were considerable. Always insist your platform publishes its latest HMRC confirmation letter.

Tax Reporting Pitfalls Even Inside the Wrapper

Platforms send annual tax certificates to both you and HMRC. If they report a figure incorrectly – perhaps interest paid in advance or a fee rebate misclassified – you could face an enquiry. Because the amounts are tax-free you might ignore it, but HMRC can still ask questions about the source of funds or connected-party rules. I now recommend every client keeps screenshots of the platform’s confirmation that the loans were qualifying at the point of investment.

High-Income Child Benefit Charge and Other Interactions

Many business owners with children assume the IFISA is invisible to the high-income child benefit charge. It is – because there is no taxable income. That’s a genuine advantage. However, if you later withdraw and the ISA is deemed void, the sudden taxable income could trigger a repayment of child benefit for the whole year. Rare, but I have seen it happen with other ISA types when errors occurred.

Practical Checklist: Before You Invest a Single Pound in an IFISA in 2026

- Confirm the platform holds current Article 36H and 39G permissions – check the FCA register yourself.

- Read the latest wind-down plan and understand recovery timelines.

- Calculate your 10% investable-asset limit if you have not received regulated advice.

- Diversify across at least three different loan types or sectors.

- Keep platform statements showing the loans were qualifying when funded.

- Review secondary-market liquidity data for the last 12 months.

- Discuss with your accountant how a capital loss would affect your overall tax position (spoiler: it won’t inside the ISA).

- Stress-test your cash-flow – can you survive without this money for five years?

- Check whether the platform offers automatic bad-debt provisioning that actually works in practice.

- Confirm you are not connected to any borrower.

Two Real-Life Case Studies from My Practice (Names Changed)

First, Sarah, a Scottish GP with £120,000 investable assets. She invested £20,000 in an IFISA in 2022. Two loans defaulted; the platform recovered 65%. Outside the wrapper she could have offset the loss and saved £1,400 in tax. Inside, the net return dropped from the advertised 6.8% to under 3%. The tax shelter helped, but the absolute loss still hurt.

Second, Michael, a London company director who used his IFISA for property-development loans. When the platform hit regulatory problems in 2024, the loans continued but secondary-market bids dried up. He needed funds for his business expansion and ended up remortgaging his house at higher cost. The IFISA protected the tax position perfectly – it just couldn’t protect his liquidity.

Moving Forward – What Smart Taxpayers Are Doing Differently in 2026

The key insight after nearly two decades advising clients is this: an IFISA turns P2P lending from a taxable high-risk investment into a tax-free high-risk investment. The risk level does not drop; the reward simply increases because the tax drag disappears. That makes it attractive for higher-rate taxpayers and business owners with surplus cash they genuinely do not need for five-plus years.

Yet the moment you treat the IFISA as “safe” because it is tax-free, you have made the classic mistake I see year after year. Capital is at risk. Always.

Peer-to-Peer Lending in ISAs

The Hidden Risks for UK Taxpayers in the 2025/26 Tax Year

The Allure of Tax-Free Returns

For the 2025/26 tax year, the £20,000 ISA allowance remains a powerful tool. The Innovative Finance ISA (IFISA) tempts busy business owners and higher-rate taxpayers by allowing them to shelter high-yield Peer-to-Peer (P2P) lending returns from HMRC. No personal savings allowance limits, no income tax (20%, 40%, or 45%), and no capital gains tax.

"It sounds almost too good – and that’s exactly where the first red flag appears. The moment you wrap high-risk P2P loans inside an IFISA, you lose critical protections you would have outside."

Borrower Default Risk: The True Cost

The single biggest risk in P2P lending is borrower default. While platforms boast about provision funds, recoveries are rarely 100%. The critical difference lies in how HMRC treats these losses. In a standard, taxable P2P account, you can claim bad-debt relief against other P2P interest. Inside an IFISA, because the interest isn't taxable, there is nothing to offset against. The relief simply vanishes.

Net Loss Comparison: A £3,000 Default

This chart visualizes the financial impact of a £3,000 loan default for a higher-rate (40%) taxpayer. Outside the ISA wrapper, the investor can offset the bad debt, recovering £1,200 via tax relief. Inside the IFISA, the entire £3,000 is gone forever.

Case Study: David's £15,000 Investment

In 2023, David (a company director) invested £15,000 into a well-known IFISA. By 2024, two property-development loans defaulted.

"The capital was gone for good. That’s the hidden cost nobody shouts about."

Anatomy of an IFISA Default

When an investment goes bad inside an IFISA, the loss is absolute. This doughnut chart breaks down the composition of David's £3,000 default.

Instead of just absorbing a net loss of £1,800 (as he would have in a taxable account after claiming bad-debt relief), David also absorbed a "phantom loss" of £1,200—the exact amount of tax relief he forfeited by choosing the IFISA wrapper.

- ■ £1,800 Base Capital Loss

- ■ £1,200 Forfeited Tax Relief

The Absence of FSCS Protection

While reputable articles mention the lack of Financial Services Compensation Scheme (FSCS) protection, few explain the practical consequences. P2P loans are not covered by the FSCS, even when held within an IFISA wrapper. If the platform fails, your money is entirely at risk.

| Investment Account Type | FSCS Protection Limit | Safety Net Status |

|---|---|---|

| Cash ISA | Up to £85,000 | ✅ |

| Stocks & Shares ISA (Money-Market) | Up to £85,000 | ✅ |

| Innovative Finance ISA (P2P Loans) | £0 (No Coverage) | ❌ |

Professional Advice

"In my practice, I now insist every client reads the platform’s wind-down plan (required by the FCA since 2019) before committing a single pound. If the platform fails without a solid plan, your investments could be tied up for years, or lost entirely."

Platform Failures, Liquidity Traps and the Smart Taxpayer’s Playbook for 2026

Now that we’ve covered the core risks of borrower defaults, the lack of FSCS cover, and the qualification pitfalls, let’s dig into the operational side – the bits that trip up even seasoned investors who think they’ve done their homework.

The Shrinking P2P Market – What It Means for IFISA Investors Today

The FCA’s latest discussion paper (DP25/3 from December 2025) lays it bare: retail investment in P2P loans has dropped sharply from around £6 billion in 2021 to just £1.4 billion in 2025. Many platforms have pivoted to balance-sheet lending or exited entirely. Fewer retail players mean thinner secondary markets and less competition on rates.

For IFISA holders this contraction is double-edged. On one hand, surviving platforms tend to be more cautious with underwriting – I’ve seen better provision funds and stricter borrower checks. On the other, your options are narrower. If your chosen platform decides to wind down retail P2P (as several did quietly in 2024–25), your loans get administered but you can’t easily reinvest fresh subscriptions elsewhere without hunting for a new IFISA provider.

When the Platform Hits Trouble – Real Recovery Timelines

Wind-down plans are mandatory now, but “orderly” doesn’t equal “quick”. Administrators collect repayments over months or years. Interest may continue (tax-free inside the IFISA), but capital trickles back slowly. In my experience, clients who needed liquidity during these periods often borrowed elsewhere at rates higher than their P2P return.

One client in early 2025 had £18,000 tied up when his platform announced a shift away from retail lending. The loans kept performing, but the secondary market vanished overnight. He waited 14 months for full repayment while his business cash flow suffered. The IFISA preserved the tax advantage – no sudden taxable income – but the opportunity cost was painful.

Secondary Market Discounts – The Hidden Erosion of Returns

Even on active platforms, secondary trading often means accepting a discount to exit early. In 2025/26 I’ve seen average discounts of 3–8% on mid-term loans, higher on riskier ones. Inside an IFISA you can sell, but the proceeds stay as cash in the wrapper (or get reinvested if the platform allows). You can’t use the sale to fund a new loan outside the ISA without losing the tax shelter on future interest.

Be careful here if you’re planning to use IFISA funds for short-term needs. Many clients assume “I can just sell” – until they see the bid prices and realise they’re locking in a permanent loss.

The 10% Investable Assets Rule – Still Enforced, Still Overlooked

If you invest without independent financial advice, the FCA caps new P2P exposure at 10% of your net investable assets (broadly cash, investments, property minus debts). Platforms must check this, but enforcement varies. Some ask for a simple self-certification; others dig deeper.

I’ve had clients breach this unintentionally because they under-reported property values or forgot pension pots. The platform should block the investment, but if it doesn’t and you default later, you have limited recourse. Always keep evidence of your calculation – it’s your defence if the FCA ever enquires.

Diversification – Beyond Just Spreading Across Loans

Diversify across loan types (consumer, property, SME), sectors, and ideally platforms. But in a shrinking market, platform diversification is harder. Some IFISA providers partner with only one or two underlying platforms – check the small print.

A practical tip from years of reviewing client portfolios: aim for no more than 20–25% of your IFISA in any single sector (e.g., property development). Economic shocks hit sectors unevenly, and recoveries vary wildly.

The 2027 ISA Reforms – Why They’re Already Shaping IFISA Decisions

From 6 April 2027 the cash ISA limit drops to £12,000 for under-65s (overall allowance stays £20,000). No transfers from stocks-and-shares or IFISAs to cash ISAs, and interest on unlent cash in investment ISAs gets taxed. HMRC’s Tax-free savings newsletter 19 (November 2025) confirms these anti-avoidance measures.

Smart taxpayers are acting now. Many are maxing IFISAs in 2025/26 and 2026/27 while the full £20,000 can still go into lending without cash-parking penalties looming. If you hold large unlent balances in an IFISA today, consider deploying them before the rules bite – or accept future tax on that cash interest.

Advanced Mitigation Strategies I Use with Clients

Here’s what actually works in practice:

- Stress-test recoveries – Assume 70–80% recovery on defaults (better than many platforms advertise in bad years) and model your net return after tax-free status.

- Layer with other wrappers – Use part of your allowance in a stocks-and-shares ISA for more liquid assets to balance the illiquidity of P2P.

- Document everything – Screenshot platform confirmations of qualifying status, FCA permissions, and your 10% calculation. HMRC enquiries on IFISAs are rare but increasing with crypto ETN reclassifications (from April 2026 some assets shift to IFISA only).

- Review annually – Platforms change terms; re-check HMRC’s list of approved ISA managers and the platform’s status.

- Consider ethical or niche platforms – Some focus on green lending or regional SMEs with stronger community ties – but vet the underwriting rigorously.

Comparison: IFISA vs Taxable P2P Account in 2025/26

Scenario | Taxable P2P Account | IFISA Wrapper | Winner for Most Higher-Rate Taxpayers? |

£20,000 invested, 7% gross return | £1,400 interest; £560 tax at 40% after £500 PSA | £1,400 tax-free | IFISA |

20% default, £4,000 loss | £1,600 bad-debt relief at 40% | No relief – £4,000 gone forever | Taxable (relief cushions blow) |

Platform wind-down, 2-year wait | Capital frozen; interest taxable when received | Capital frozen; interest tax-free | IFISA (tax shelter during delay) |

Early exit via secondary market | Sell at 5% discount; loss offsettable if capital loss | Sell at 5% discount; no CGT, but loss trapped | Tie – depends on tax rate |

Future 2027 cash interest charge | N/A | Potential tax on unlent cash if rules apply | Taxable (no cash charge) |

The Exact Wording I Include in Client Letters Now

“While the Innovative Finance ISA offers genuine tax advantages, it does not reduce the underlying risks of peer-to-peer lending. Capital is at risk of partial or total loss. There is no FSCS protection for the loans themselves, liquidity may be limited, and in the event of platform difficulties you could face extended delays in accessing funds. Please confirm you can afford to lock this money away for the expected term without relying on it for essential needs or business liquidity.”

Clients sign off on that paragraph – it forces the conversation.

Peer-to-Peer Lending in IFISAs: Risks for UK Taxpayers

Tax-free returns are tempting, but the Innovative Finance ISA wrapper does not reduce the underlying risk of P2P lending. Explore what's changed in 2026, model the tax impact, and use the interactive checklist before you invest.

The 2025/26 & 2026/27 picture at a glance

What's actually new in 2026

The risks that actually cost money — click to expand

The single biggest risk is the borrower failing to repay. Even with provision funds and property security, recoveries are never 100% — and they spike in downturns.

The IFISA twist: outside an ISA you can offset irrecoverable P2P loans against other P2P interest via SA101 (bad-debt relief). Inside the IFISA, that relief disappears — there is no taxable interest to offset. For a 40% taxpayer, a £4,000 loss inside the wrapper costs roughly £1,600 more than the same loss outside it.

No SA101 relief Permanent capital lossP2P loans are not covered by the Financial Services Compensation Scheme — even when held in an IFISA. Only cash sitting unlent on the platform may qualify for £85,000 cover, and only if the platform is also a deposit-taker. Most are not.

Compare with a Cash ISA or S&S ISA holding money-market funds where the safety net does apply. Always read the platform's FCA-mandated wind-down plan before subscribing.

£0 FSCS on loans Full capital at riskMost loans run 3-5 years. Secondary markets exist on some platforms but in 2025/26 they're thin, with typical exit discounts of 3-8% on mid-term loans and higher on riskier ones.

IFISA rules add another layer: loans held outside the ISA cannot be sold and re-purchased inside the wrapper unless they're openly available to any buyer at the same price. You can't easily shuffle loans in and out for tax reasons.

3-8% exit discounts Strict re-purchase rulesFor loans to stay in an IFISA, the platform must hold the correct FCA permissions (Article 36H operating an electronic system for lending, and 39G debt administration), the loan must be on genuine commercial terms, and you must not be connected to the borrower.

If HMRC decides the investment no longer qualifies, the ISA manager has just 30 days to sell or transfer it out. In extreme cases the entire subscription can be treated as never having been an ISA — with backdated tax charges.

30-day rule Backdated tax riskSince 2019 the FCA requires every loan-based crowdfunding platform to have a wind-down plan. "Orderly" is not the same as "fast" — Lendy and Funding Secure investors waited years for partial recoveries.

If the platform fails while your loans are in an IFISA, the tax-free status survives but the capital is frozen. The wrapper protects the tax position; it offers zero help with liquidity or capital preservation.

Multi-year recoveries Cash flow riskFCA rules since 2019 cap new P2P investors without regulated advice at 10% of their net investable assets (broadly cash, investments and property minus debts).

Speaking to the platform's staff doesn't count as advice. Breaches limit your recourse if things go wrong. Keep evidence of your calculation in case the FCA ever queries it.

Unadvised investors Self-certify carefullyThe FCA's discussion paper DP25/3 (Dec 2025) confirms retail P2P investment has fallen from around £6 bn in 2021 to £1.4 bn in 2025. Many platforms have pivoted to balance-sheet lending or exited entirely.

Survivors tend to be more cautious — better provision funds, stricter underwriting — but your choice of platform is narrower and secondary markets are thinner. Platform diversification is harder than it was five years ago.

Fewer platforms Thin secondary marketsLoans must be entered into on genuine commercial terms and not as part of any tax-avoidance arrangement. You must not be a "connected person" with the borrower (broadly: family, business partners, your own companies).

If a platform changes its loan agreements mid-term, HMRC may query the qualifying status. Keep screenshots of the platform's confirmation that loans were qualifying at the point of investment.

No connected borrowers Genuine commercial termsTax impact calculator — IFISA vs taxable P2P (2025/26)

See how much the IFISA wrapper actually saves you — and how much bad-debt relief you'd give up if a portion of the loans default.

Taxable P2P account

Inside the IFISA

IFISA vs taxable P2P — risk by risk

| Risk / Feature | Outside ISA (Taxable) | Inside IFISA |

|---|---|---|

| Borrower default | Bad-debt relief available (SA101) | No relief — loss is permanent |

| Tax on interest | Taxed above PSA (20/40/45%) | 0% — fully tax-free |

| FSCS protection on loans | None | None — same gap |

| Liquidity / secondary market | Available, often at a discount | Same, with stricter re-purchase rules |

| Platform failure | Loans administered; interest taxable | Tax shelter intact; capital still frozen |

| Capital gains on resale | Possible CGT above £3,000 | No CGT — but losses trapped |

| High-Income Child Benefit Charge | Interest counts toward threshold | Invisible — unless ISA voided |

| Reporting on Self Assessment | Required for interest & relief | Not required |

| Subscription cap | Unlimited | Shares £20,000 ISA allowance |

Bottom line: the IFISA converts a taxable high-risk investment into a tax-free high-risk investment. The risk level doesn't drop — only the tax drag does. Higher-rate taxpayers benefit most when loans perform; they're hurt most when defaults occur, because the offsetable relief is gone.

2026 - 2027 ISA & P2P regulatory roadmap

Before you commit a single pound — interactive checklist

Wrapping It Up – The Balanced View for 2026

IFISAs remain a powerful tool for higher-rate and additional-rate taxpayers who want to shelter interest from P2P lending. The tax saving can add 1–2% to effective returns compared with a taxable account. But the wrapper amplifies the pain of losses because you forfeit bad-debt relief and any CGT offset.

Use it only for money you genuinely don’t need short-term, diversify sensibly, and stay vigilant on platform health. The market is smaller and more mature than five years ago – that’s both safer and more limited.

Summary of Key Insights

- Borrower defaults inside an IFISA offer no bad-debt tax relief, turning a recoverable loss outside the wrapper into a permanent hit.

- No FSCS protection applies to P2P loans – even in an IFISA – leaving your full capital exposed.

- Liquidity remains poor; secondary markets often force discounts, and early access can erode returns significantly.

- Qualification rules are strict – a loan losing status can trigger forced sales or void-ISA risks with back tax.

- Platform wind-downs freeze capital for months or years; the tax shelter survives but cash flow suffers.

- The 10% investable assets cap still applies to unadvised investors – breaches limit recourse if things go wrong.

- The P2P market has contracted sharply since 2021, reducing options and secondary liquidity for IFISA users.

- From April 2027 cash ISA limits drop to £12,000 for under-65s, with anti-avoidance rules hitting unlent cash in IFISAs.

- Diversify across loan types, sectors and ideally platforms to spread risk in a maturing market.

- Treat IFISAs as a tax enhancer for high-risk lending, not a safe haven – only commit funds you can truly lock away long-term.

FAQs

Q1: Can I transfer existing P2P loans from a taxable account into an IFISA without using up my annual allowance?

Well, it’s a question I get from directors all the time who want to tidy up their finances. The short answer is no – you cannot transfer loans you already hold outside an ISA straight into the IFISA wrapper. You’d have to sell them first, take the cash proceeds, and then use fresh money to subscribe, which does eat into your £20,000 allowance. I once had a freelance consultant in Leeds who tried to work around this by selling and immediately rebuying the same loans inside the ISA; the platform flagged it as a potential breach and he ended up with a small tax bill on the disposal. Always sell, wait for settlement, then subscribe properly to keep everything clean.

Q2: What happens to my IFISA P2P investments if I die and my spouse wants to keep them?

In practice this is smoother than most people expect. Your surviving spouse can inherit the full value as an additional permitted subscription, keeping the tax-free status intact provided they act within the time limits. The loans stay in the wrapper and continue to be administered exactly as before. I helped a client’s widow in Manchester last year – her husband had £18,000 in property-backed loans; we transferred them straight across with no tax hit and no need to sell. Just make sure your will and platform paperwork name the right beneficiaries to avoid any admin delays.

Q3: Can I lend to my own limited company or one run by a close family member through an IFISA?

Absolutely not – the connected-person rules are strict and the investment would immediately lose qualifying status. HMRC looks at control, shareholdings over 20 %, or close relatives. One of my business-owner clients in Glasgow nearly did this with his wife’s startup; we spotted it in time and redirected the funds to unrelated borrowers instead. The penalty for getting it wrong is the loan being pulled out and taxed as if it was never in the ISA. Always run any potential borrower past your accountant first.

Q4: Does holding P2P loans in an IFISA affect my marriage allowance claim?

Not at all, and that’s one of the quiet advantages. Because there is no taxable interest, it doesn’t push your income over the threshold that reduces the allowance. I’ve seen several couples where one partner is a higher-rate taxpayer and the other uses the IFISA route – the marriage allowance stays fully available. Just keep good records in case HMRC ever queries the overall income picture, but in my 15 years I’ve never seen an IFISA trigger a marriage allowance clawback.

Q5: What should I do if I accidentally over-subscribe my ISA allowance with a P2P investment?

Contact the ISA manager immediately – they have 30 days to sort it. You’ll normally have to withdraw the excess and it becomes taxable from the date it was paid in. A self-employed client in Bristol did this when two platforms auto-invested at the same time; we reclaimed the over-subscription, paid a small interest charge, and got everything corrected on his self-assessment. The key is speed – the longer you leave it, the bigger the potential penalty.

Q6: Can I complain to the Financial Ombudsman Service about an IFISA platform?

Yes, and many people don’t realise the FOS route is still open even though the interest is tax-free. If the platform mishandles a loan, delays repayments, or mis-sells the product, you can go through their complaints process and then to the Ombudsman. I guided a PAYE employee through a successful claim last year after a platform misreported a loan term; he recovered the difference plus compensation, all inside the ISA wrapper. Keep every email and statement – it makes the process far quicker.

Q7: As a self-employed trader, does P2P interest inside an IFISA count towards my trading income for National Insurance?

No, it’s treated purely as savings income even if you’re self-employed. That means it doesn’t inflate your Class 4 NI bill or affect your trading profits. One of my gig-economy clients who drives for Uber and also invests in P2P was relieved when we confirmed this – his NI stayed exactly the same. Just don’t start treating P2P lending as your main trade or HMRC might look at it differently.

Q8: What if my company director’s loan account is involved with an IFISA investment?

Keep them completely separate. Using an IFISA to fund or repay a director’s loan can create connected-party issues and potential benefit-in-kind charges. I had to unravel this for a client in London whose accountant had mixed the two; we ended up selling the loans and repaying the loan account properly to avoid a tax hit. Treat the IFISA as strictly personal money.

Q9: How are P2P loans in an IFISA treated in a divorce settlement?

They are considered part of your personal assets and can be transferred or sold as part of the financial order. The tax-free status survives the transfer to your ex-spouse if the court orders it, but the receiving party then uses their own ISA allowance going forward. I’ve seen several cases where couples split the portfolio evenly – the loans stayed inside their respective ISAs with no immediate tax consequence.

Q10: Can I keep contributing to an IFISA after I become non-resident?

Existing investments stay tax-free, but you cannot make new subscriptions once you lose UK tax residency. The loans continue to be administered and any interest remains sheltered. A client who moved to Spain kept his £12,000 portfolio running for another three years – the platform handled everything and there was no UK tax to pay. Just inform HMRC of your change in status so they don’t expect self-assessment returns on the interest.

Q11: Does maxing out my IFISA with P2P lending reduce the amount I can pay into a pension?

No – the two allowances are completely separate. You can use your full £20,000 ISA and still get tax relief on pension contributions up to your annual allowance. Many higher-earning clients I advise do both every year to maximise shelter. The only overlap is cash-flow planning; make sure you have enough liquidity outside both wrappers.

Q12: What happens if my IFISA platform changes its lending criteria mid-way through a loan?

The platform must notify you and the ISA manager. If the loan no longer qualifies, it may have to be removed from the wrapper, triggering a potential tax charge on future interest. I had a client whose platform tightened rules on property loans; we moved the affected loans out in time and avoided any bill. Review platform emails promptly – they’re not just marketing fluff.

Disclaimer

The information provided in this article is for general guidance only and is not intended to constitute professional advice, tax advice, financial advice, legal advice, or any other form of regulated guidance. Although every effort has been made to ensure accuracy at the time of publication, Fair View Accounting Services, including its director, employees, contractors, writers, and content-creation team, accepts no responsibility for any loss, damage, penalty, or consequence arising from reliance on the information contained herein.

UK tax legislation changes frequently, and HMRC interpretations, thresholds, and rules may vary depending on the individual circumstances of each taxpayer. Nothing in this article should be considered a substitute for obtaining formal, personalised advice from a qualified accountant or tax professional. Readers should not take action—or refrain from taking action—based solely on the content published on this website.

Fair View Accounting Services does not guarantee the completeness, accuracy, or ongoing validity of the information provided and assumes no liability for omissions or errors, whether typographical, factual, or technical. By using this content, the reader acknowledges that all responsibility for decisions remains solely with the user.