Annual Investment Allowance £1m — What Counts And What Doesn't

Annual Investment Allowance £1m: What Counts and What Doesn’t

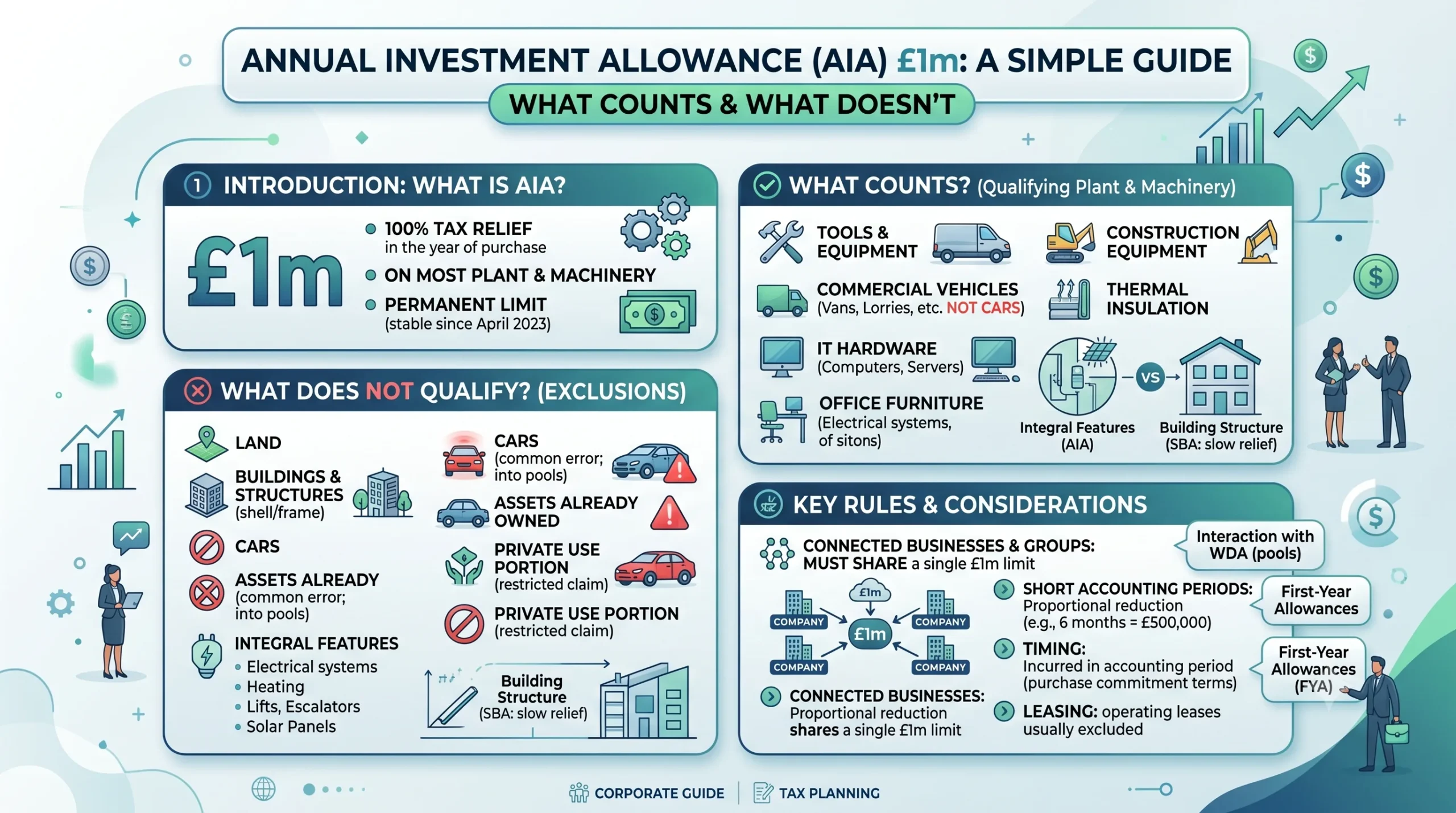

The Annual Investment Allowance is one of the most straightforward capital allowances in the UK tax system in principle, and one of the most frequently misunderstood in practice. The headline — 100% tax relief in the year of purchase, up to £1 million — makes it sound simpler than it is. The complications lie in what qualifies, what is excluded, how the limit works for groups of connected businesses, and what happens at the edges where the rules are less clean than the headlines suggest.

For any business spending on plant and machinery, understanding the AIA boundary can determine whether a tax deduction is claimed this year or spread over many years at much lower rates.

What the AIA Is and the Current Limit

The Annual Investment Allowance gives 100% tax relief on the cost of most plant and machinery. You can claim AIA for items you buy or lease under a hire purchase agreement. The AIA was permanently set at £1 million from 1 April 2023 for companies and 6 April 2023 for unincorporated businesses.

The permanent setting at £1 million removed the uncertainty that had plagued the AIA for years — a sequence of temporary rates, sudden changes, and complex transitional calculations when the rate changed mid-accounting period. The £1 million limit is now stable, and for the majority of small and medium-sized businesses it is large enough that the cap never becomes a constraint.

Where it does constrain — for businesses spending heavily on equipment, fit-outs, or specialist assets — understanding what sits inside the AIA limit and what sits outside it is the difference between a large upfront deduction and a much more modest annual writing-down allowance.

What Qualifies for AIA

The AIA applies to expenditure on plant and machinery used in a qualifying activity. The term “plant and machinery” has a broad meaning in capital allowances, and HMRC’s guidance and case law have shaped its boundaries over many decades.

Items that clearly qualify include:

- Tools, equipment, and machinery used in a trade

- Commercial vehicles — vans, lorries, tractors, and similar

- Computers, servers, and IT equipment

- Office furniture and fixtures (in most cases)

- Integral features in commercial buildings — electrical systems, cold water systems, heating, cooling and ventilation systems, lifts, escalators, and solar panels

- Thermal insulation added to existing buildings

- Construction equipment

The key question is always whether the item constitutes plant or machinery in the context of the trade. An item used for both business and private purposes may qualify only to the extent of business use.

Integral Features: An Important and Often Missed Category

Integral features — such as electrical systems, cold water systems, lifts, escalators, and certain lighting systems installed in commercial buildings — qualify for AIA and are not treated as part of the building structure itself.

This matters because the structure of a building does not qualify for AIA. The building is a separate asset attracting structures and buildings allowance (SBA) at 3% per year on cost — much slower relief than the AIA’s 100%. Correctly identifying which parts of a building fit-out or installation are integral features (and therefore AIA-eligible) versus structural (and therefore SBA only) can produce a significant timing difference in tax relief.

An office refurbishment that costs £400,000 might include electrical rewiring (integral feature — AIA available), new partitioning walls (structural — SBA only), a new heating system (integral feature — AIA available), new carpeting (plant — AIA available), and ceiling works (structural — SBA only). Separating these costs correctly is not optional — it is required for an accurate capital allowances claim.

What Does Not Qualify for AIA

The exclusions are important enough that every business making significant capital investments should work through them explicitly.

Land. No capital allowances of any kind apply to the purchase price of land. If a business purchases a commercial property for £500,000, of which £100,000 is attributable to land, that £100,000 is excluded from all allowances.

Buildings and structures. The shell of a building — walls, roof, floors — does not qualify for AIA. It may qualify for SBA if it is a new or newly renovated commercial building, but that is a different relief at a much slower rate.

Cars. Cars do not qualify for AIA. They instead go into a capital allowance pool and attract writing-down allowances over several years. This is one of the most frequently encountered exclusions. The distinction between a car and a van matters considerably — a van qualifies for AIA; a car does not. HMRC defines a car for this purpose as a vehicle primarily suited to the carriage of passengers, which catches dual-cab pickup trucks with rear seating in some configurations. If a business is buying a vehicle with any ambiguity about classification, checking HMRC’s guidance on the car/van distinction before the year end is important.

Assets already owned. AIA applies only to new expenditure incurred during the accounting period. An asset transferred from private use to business use, or contributed to the business by a connected party, does not qualify for AIA — it enters the pool at market value and attracts only writing-down allowances.

Assets used partly for non-business purposes. Where an asset is used partly for private purposes, the AIA is restricted to the business-use proportion. A director who buys a laptop and uses it 60% for business and 40% for personal use can claim AIA on 60% of the cost.

Items where the exclusive business use test is not met in certain professions. Self-employed individuals in some sectors face more restrictive rules on certain categories of expenditure.

The Connected Persons and Group Limit: Where the Trap Lies

The £1 million AIA limit applies to each business entity — but connected businesses must share a single limit.

Where two or more businesses are connected to each other — for example, companies under common control, or a sole trader and a company that they also control — the £1 million AIA limit must be shared between them.

This is the rule that most medium-sized groups and family business structures overlook. A family where one spouse runs a sole trade catering business and another spouse operates a limited company providing related hospitality services may, if those businesses are connected through common control, have to share the £1 million AIA between them. If both businesses are investing heavily in equipment in the same year, the combined limit constrains the total deduction available.

Connected persons for this purpose include relatives (spouses, civil partners, siblings, parents, and their spouses), companies under common control, and certain partnership arrangements. The definition is broad enough to catch many family business structures.

Worked example: A building contractor operates two limited companies — one for residential work and one for commercial work. Both are under his sole control. In the year to 31 March 2027, Company A spends £700,000 on plant and machinery. Company B spends £500,000. Combined qualifying expenditure: £1.2 million.

If the group had an unlimited AIA, 100% of £1.2 million would attract immediate full relief. With a shared £1 million limit, the additional £200,000 falls into the main pool at 18% writing-down allowance — a first-year deduction of £36,000 rather than £200,000. The difference — £164,000 of deferred relief — has a meaningful present value.

How AIA Interacts With the Writing-Down Allowance

Where expenditure exceeds the AIA limit — or where the AIA is not claimed on a particular item — the asset enters a capital allowances pool. For most plant and machinery, this is the main pool attracting an 18% writing-down allowance on the reducing balance each year. Some assets — long-life assets, or assets with a useful economic life exceeding 25 years — enter the special rate pool at 6%.

Cars always enter a pool, at rates determined by their CO2 emissions:

- Zero-emission cars: first-year allowance of 100% (but this is a separate relief, not AIA)

- Cars with CO2 emissions up to 50g/km: main pool at 18%

- Cars with CO2 emissions above 50g/km: special rate pool at 6%

The key point is that once expenditure is in a pool, the writing-down allowance applies year on year to the declining balance. On a £200,000 asset in the main pool at 18%, the Year 1 relief is £36,000, Year 2 approximately £29,520, Year 3 approximately £24,206, and so on — never reaching zero. It takes many years for the pool value to reduce to near-zero, and the original capital cost is effectively never fully relieved in present value terms.

This is precisely why claiming the AIA on every qualifying asset up to the limit is important. The time value of the deferred relief can be significant.

The £1,000,000 Threshold

A permanent pillar of the UK tax system, the Annual Investment Allowance offers 100% tax relief on qualifying plant and machinery. Understanding the boundary between immediate deduction and decades-long pooling is the cornerstone of capital planning.

What Defines 'Plant & Machinery'?

The AIA applies to expenditure used for a qualifying trade activity. This encompasses everything from the server in your office to the specialized heating systems in your warehouse. Identifying these assets correctly is the first step toward a valid claim.

AIA Eligible Categories

Core Trade Equipment

Tools, machinery, and specialized computers essential for your specific business operations.

Commercial Vehicles

Vans, lorries, and tractors qualify; however, passenger cars are strictly excluded from AIA.

Integral Building Features

Electrical, heating, and cooling systems that are part of the building but distinct from its structure.

The Cost of Deferral

When investment exceeds the £1m limit or falls into exclusions, it enters "pools." The difference in relief timing between AIA and the standard Main Pool (18% Writing-Down Allowance) has a significant impact on cash flow and the present value of tax savings.

AIA (100%) vs. Main Pool (18% WDA) Relief Profile

Visualizing the relief of a £200,000 investment over a 5-year period. WDA never reaches zero, creating a permanent deferral of tax value.

The Fit-Out Split

In a commercial refurbishment, not all costs are equal. Structures and Buildings Allowance (SBA) offers only 3% relief annually. Maximizing AIA involves precisely identifying the "Integral Features" hidden within structural work.

Pro-Tip:

Electrical installations and HVAC systems can account for up to 25-40% of a modern office fit-out. Separating these ensures immediate 100% relief rather than 33-year straight-line depreciation.

Composition of a £600k Commercial Fit-Out

Hidden Constraints & Timing Traps

The £1,000,000 headline figure is not guaranteed. Two primary factors can reduce this limit: the length of your accounting period and the existence of connected business entities.

Accounting Period Reduction

The AIA is scaled down for periods shorter than 12 months. A 6-month first year halves the allowance to £500,000.

The Connection Trap

If you control two companies, you don't get two limits. One shared £1m allowance must be allocated between them.

No SVG used in diagram

Final AIA Exclusion Checklist

Ensure these items are categorized into pools, not AIA.

Passenger Cars

Automatically enter the 18% or 6% pool based on CO2 emissions.

Building Shell

Walls, roofs, and floors fall under SBA (3%), not AIA.

Transferred Assets

Items already owned or moved from private use do not qualify.

Accounting Period Complications: The AIA Is Not Always a Full £1 Million

For businesses with accounting periods that are not twelve months — either because they are a new business with a short first period, or because they have changed their year-end date — the AIA is proportionally reduced.

The AIA is proportionate to the length of the accounting period. A nine-month accounting period has an AIA of £750,000. A three-month period has £250,000.

This is a trap for new businesses that start trading mid-year with a short first period. A company that incorporates in October and has a first accounting period ending 31 March — a six-month period — has an AIA of only £500,000. If it spends £700,000 on equipment in that six-month period, £200,000 falls outside the AIA and enters the pool.

For companies that change their year-end date and have an accounting period of more than twelve months — say eighteen months after a change — the AIA cannot exceed £1 million regardless of the period length. It is not scaled up beyond the annual maximum.

The Timing of Expenditure Within the Period

AIA is claimed on expenditure incurred during the accounting period. For most businesses, this means the date the asset was purchased or the hire purchase contract was signed. Where there is a gap between ordering an asset and receiving it — particularly for bespoke equipment or large plant — the timing of the legal commitment matters.

For hire purchase agreements, the expenditure is treated as incurred when the agreement is entered into, not when the final payment is made. A business that signs a hire purchase agreement for £200,000 of equipment on 30 March — two days before the year end — can claim AIA for that period even if delivery occurs in April.

For outright purchases, the expenditure is incurred when the obligation to pay becomes unconditional — typically when title passes or when a contractual liability is created. A purchase ordered in March with delivery and invoicing in April falls in the April accounting period, not March.

Leasing: When AIA Does Not Apply

A business that leases equipment — under an operating lease rather than a hire purchase or finance lease — does not own the asset and therefore cannot claim AIA on it. The lease payments are instead deductible as a revenue expense in the normal way.

For hire purchase agreements, the treatment is different: the business is treated as the owner of the asset from the outset, and AIA applies to the capital cost of the asset (not the total HP payments, which include a finance charge). The finance charge element is separately deductible as a revenue expense.

Finance leases — where the risks and rewards of ownership pass to the lessee — are also treated as effectively creating ownership for capital allowances purposes in most cases, and AIA may be available.

The practical question for a business deciding whether to buy, hire purchase, or lease equipment involves both the capital allowances position and the cash-flow, VAT, and balance sheet implications. AIA on a purchase or HP agreement provides immediate 100% relief; operating lease payments are deducted as incurred but typically spread over the lease term. Neither is universally better — the comparison depends on the business’s tax position, interest rates, and cash-flow requirements.

First-Year Allowances: A Distinct Relief

Alongside AIA, some categories of expenditure attract first-year allowances — 100% relief in the year of purchase — but outside the AIA framework and not subject to the £1 million cap.

Zero-emission cars and zero-emission goods vehicles attract a 100% first-year allowance. This is separate from the AIA and is not capped at £1 million.

For a business buying ten electric vans at £50,000 each — a total of £500,000 — the full amount qualifies for 100% first-year allowance regardless of what other AIA expenditure has been incurred. This relief sits alongside the AIA, not within it.

Other categories attracting first-year allowances include certain energy-efficient plant, water-efficient technologies, and new zero-emission business assets on the government’s approved lists. These are updated periodically, and the qualifying product lists should be checked via GOV.UK before a claim is made.

Structures and Buildings Allowance: The Fallback for Excluded Items

For expenditure on buildings and structures that do not qualify for AIA, the SBA provides 3% per year relief on a straight-line basis from the date the building is first used. The structures and buildings allowance applies to the cost of new commercial buildings and their renovation, excluding land costs and any expenditure that qualifies as plant and machinery.

At 3% per year, the SBA provides full relief over approximately 33 years — a much longer timeline than AIA or even writing-down allowances. For a business investing in commercial premises, correctly identifying and separating the plant and machinery elements (AIA-eligible) from the structural elements (SBA-eligible) is one of the highest-value exercises in capital allowances planning.

A commercial fit-out of £600,000 might decompose as:

- Heating and ventilation systems: £80,000 (integral feature — AIA)

- Electrical installation: £60,000 (integral feature — AIA)

- Lighting systems: £30,000 (integral feature — AIA)

- Shop fitting, furniture, and displays: £120,000 (plant — AIA)

- Structural alterations and wall construction: £180,000 (SBA only)

- Decorative works: £130,000 (may be SBA or potentially plant depending on function)

The split between AIA-eligible and SBA-only is the difference between a first-year deduction of approximately £290,000 versus a £8,700 annual deduction on the structural element. The exercise of correctly categorising mixed fit-out expenditure is worth doing carefully.

Common Planning Mistakes

Claiming AIA on cars. Cars go into pools regardless of whether they are labelled as company vehicles. Van-versus-car classification errors are among the most common capital allowances mistakes.

Failing to split connected group expenditure. Two companies under common control must share the £1 million limit. Many owner-managed business groups simply claim full AIA in each entity without recognising the restriction.

Ignoring integral features. Some accountants still treat all building fit-out costs as structural, missing the AIA available on integral features. This is a systematic understatement of capital allowances in commercial property investment.

Treating private use as full business use. For sole traders and partnerships, any private use of an asset requires the AIA claim to be restricted pro-rata. Using 100% AIA on a vehicle that is partly privately used is incorrect and creates a compliance risk.

Not claiming AIA in the year of acquisition. The AIA must be claimed in the accounting period the expenditure is incurred. It is not possible to defer the claim to a later year — unlike writing-down allowances, there is no carry-forward mechanism for AIA. A business that failed to claim AIA in a prior year loses the opportunity permanently.

Year-End Capital Allowances Checklist

For businesses approaching their year end with capital expenditure decisions to make, the following questions focus on the key planning opportunities:

Question | Planning Action |

Have all asset purchases been correctly classified as AIA-eligible? | Review the asset register for cars, land, and structural items incorrectly claimed under AIA |

Does the business have connected entities sharing the £1m limit? | Identify the most tax-efficient allocation of AIA across connected businesses |

Are there integral features in commercial property that have been missed? | Commission a capital allowances survey for significant property expenditure |

Is there planned equipment expenditure that could be brought into this accounting period? | Consider accelerating purchase decisions to maximise current-period AIA |

Are any zero-emission vehicles being purchased that could attract a first-year allowance? | Ensure these are claimed as FYA, not AIA |

Has the AIA limit been reduced because of a short accounting period? | Verify the proportionate cap and plan expenditure accordingly |

Annual Investment Allowance £1m

What Counts & What Doesn't

An interactive explainer for UK businesses. Updated for the Autumn Budget 2025 changes — the new permanent 40% First-Year Allowance from 1 January 2026 and the main rate WDA cut from 18% to 14% from April 2026.

What Qualifies for £1m AIA

The AIA covers plant and machinery used in a qualifying activity. The term is broader than it sounds — decades of HMRC guidance and case law have shaped its boundaries. Tap each tile for detail.

Tools, equipment & machinery

Anything used in the trade — workshop kit, manufacturing machinery, kitchen equipment, dental chairs, hairdressing chairs. Both new and second-hand qualify for AIA.

Commercial vehicles

Vans, lorries, tractors, forklifts and similar. Not cars — and the van-vs-car line is HMRC's most-disputed boundary. Dual-cab pickups with rear seating are sometimes reclassified as cars.

Computers, servers & IT

Hardware, servers, networking equipment, point-of-sale systems. Software is normally treated as capital and qualifies if it has an enduring benefit; ongoing SaaS subscriptions are revenue.

Office furniture & fixtures

Desks, chairs, shelving, partitioning that functions as furniture, kitchen fittings. Decorative items used in trade premises (such as restaurant decor) often qualify on case-law grounds.

Integral features High value

Electrical systems, cold water systems, heating, cooling, ventilation, lifts, escalators, solar panels and certain lighting in commercial buildings. Often missed in property fit-outs.

Thermal insulation

Insulation added to existing commercial buildings qualifies. Insulation in newly constructed buildings is treated as part of the structure (SBA, not AIA).

Construction equipment

Diggers, plant hire equipment, scaffolding, generators, compressors. Equipment leased out for short hire to others generally qualifies for AIA.

HP & finance leases

If you acquire under hire purchase or a finance lease, you are treated as owner for capital allowances and can claim AIA on the capital cost (not the finance charge element).

What's Excluded from AIA

The exclusions matter. Claiming AIA on something that doesn't qualify creates a real compliance risk, and missing relief that does qualify is permanent — there is no carry-forward of unclaimed AIA.

Cars

Cars never qualify for AIA — they go into a pool based on CO₂ emissions. Up to 50g/km enters the main pool (14% from April 2026); above 50g/km enters the special rate pool at 6%. Zero-emission cars get a 100% FYA (extended to 31 March 2027 / 5 April 2027) — outside the AIA cap.

Land

No capital allowances of any kind apply to land cost. If a £500,000 property purchase has £100,000 attributable to land, that £100,000 attracts no relief — ever.

Buildings & structures

The shell — walls, roof, floors, foundations — does not qualify for AIA. New commercial buildings may attract Structures & Buildings Allowance at 3% straight-line (around 33 years to full relief). Far slower than AIA.

Assets already owned

Assets brought into the business from private use, or contributed by a connected party, enter the pool at market value and attract only writing-down allowances. No AIA.

Gifts & second-hand from connected parties

Gifted assets and assets bought from connected persons (relatives, controlled companies) generally don't qualify. The rules are designed to prevent value-shifting between related entities.

Mixed-use assets

Where an asset is used partly for non-business purposes, AIA is restricted to the business-use proportion. A laptop used 60% for business: claim AIA on 60% of cost only.

Operating leases

If you lease under an operating lease, the lessor owns the asset — you can't claim AIA. The lease payments are deducted as a revenue expense as they fall due.

Late claims

AIA must be claimed in the accounting period the expenditure is incurred. Unlike WDA, there is no carry-forward. Forget to claim AIA in year one and the asset enters the pool at full cost — the immediate-deduction opportunity is permanently lost.

The Autumn 2025 Budget Changes — Live in 2026/27

The capital allowances landscape changed materially in the Autumn Budget 2025. The AIA itself is unchanged at £1m, but the surrounding reliefs have shifted. Here is what's new.

New 40% First-Year Allowance

A permanent 40% FYA for new main-rate plant and machinery, sitting alongside AIA and Full Expensing. It fills the gap for unincorporated businesses (who can't use Full Expensing) and for spend above the £1m AIA cap. Crucially, it includes assets bought for leasing (except overseas leasing) — Full Expensing does not.

Excluded: cars, second-hand assets, assets leased overseas. The remaining 60% goes into the main pool for WDA at the new 14% rate.

Main pool WDA cut: 18% → 14%

The main rate of writing-down allowance reduces from 18% to 14%. This affects any spend that doesn't get full immediate relief — historic pool balances, expenditure above £1m without FYA, and most cars at 50g/km or under. The Treasury expects this to raise £1.5bn a year from 2026/27 onwards.

Unchanged: the special rate pool stays at 6% (integral features, long-life assets, high-emission cars).

£1m AIA — still permanent

The £1m Annual Investment Allowance, permanent since April 2023, is untouched. It remains the first port of call for most SMEs because it gives 100% immediate relief — better than the new 40% FYA and broader than Full Expensing (which excludes special-rate assets and second-hand).

Hierarchy of preference (main pool, new): AIA 100% > Full Expensing 100% (companies only) > 40% FYA > 14% WDA.

100% FYA for zero-emission cars & EV charge points

Originally due to end in April 2026, the 100% First-Year Allowance for new zero-emission cars and electric vehicle charge-point equipment has been extended for a further year. This sits outside the AIA cap — a business can claim £1m AIA and the EV first-year allowance on top.

Catch: the car must be new (not second-hand), and zero CO₂. Hybrid cars still go into the pool based on emissions.

The new "best relief" hierarchy in 2026/27

AIA Relief Calculator (2026/27)

Indicative only. Models a 12-month accounting period ending after 6 April 2026, with the new 14% main pool WDA. Best route is auto-selected based on asset type, business type and remaining AIA.

⚠️ Indicative model only. Real claims depend on the period mix (pre/post 6 April 2026 spend in a straddling period uses time-apportioned rates), the AIA share between connected businesses, and many other factors. Tax saving uses 25% as a default; small profits rate of 19% applies below £50k profits. Always check a real claim with a qualified tax adviser.

The Connected Persons Trap

The £1m limit applies to each business — unless businesses are connected, in which case they share a single £1m. This is the most-overlooked rule in family business groups.

Who counts as "connected"?

- Companies under common control — two or more companies controlled by the same person or group of persons.

- A company and its participators — including the director-shareholder of a close company.

- Relatives — spouses, civil partners, siblings, parents, children, and their spouses.

- Partnerships with common control or substantially common partners.

Live worked example — drag the sliders

Excess of £200,000 enters the main pool at 14% (post-April 2026 rate). Year-1 WDA is £28,000 versus £200,000 of immediate relief had the AIA been unlimited — a deferral worth £172,000 of relief into future years.

Frequently Asked Questions

If I'm a sole trader, can I use Full Expensing too?

No — Full Expensing (100%, no cap) is restricted to companies within the charge to corporation tax. Sole traders and partnerships rely on AIA for 100% relief, and from 1 January 2026 they can also access the new permanent 40% First-Year Allowance for spend above the £1m AIA cap. This is the gap the new FYA was designed to close.

I'm changing my accounting period — does the £1m still apply?

The AIA is proportionate to period length. A 6-month period gives a £500,000 cap. A 9-month period gives £750,000. For long periods (more than 12 months), the AIA cannot exceed £1m regardless of length — it doesn't scale up. When the AIA rate has changed mid-period (less of an issue now that £1m is permanent), separate calculations apply to the pre- and post-change portions.

When is expenditure "incurred" for AIA purposes?

For outright purchases, when the obligation to pay becomes unconditional — usually when title passes or a binding contract is entered into. For hire purchase, it's the date the HP agreement is signed (provided the asset is brought into use within four months). This matters at year-end: a contract signed two days before year-end can fall into the AIA for that period even if delivery is the following month.

If I miss claiming AIA in year one, can I claim it later?

No. AIA must be claimed in the accounting period the expenditure was incurred. Once that return is finalised, the opportunity is gone — the asset enters the pool at full cost and attracts only WDA (now 14% main pool / 6% special pool). For amendable returns, there is normally a 12-month window to amend; for older periods, the relief is effectively lost.

Can I claim AIA on a second-hand machine?

Yes — AIA covers both new and second-hand plant and machinery, provided it's not acquired from a connected party. This is a key advantage of AIA over the new 40% FYA, which is restricted to new assets only. For second-hand main-pool spend above the £1m AIA cap, you're back to 14% WDA.

Does claiming AIA reduce my future depreciation deduction?

It doesn't — depreciation in the accounts and capital allowances in the tax computation are separate. Depreciation is added back to profits in the tax computation and capital allowances are deducted. Claiming 100% AIA in year one gives an immediate tax deduction; depreciation in your accounts continues over the asset's useful life as normal.

My building fit-out cost £500,000. How much qualifies for AIA?

It depends on the split between plant/integral features and structural work. A typical commercial fit-out might be 40–55% AIA-eligible. For material spend, commission a capital allowances survey — specialist surveyors typically identify 5–15% more eligible spend than a standard accountant review. The cost-benefit is overwhelmingly favourable on any property project above about £200,000.

Does the AIA reduce my National Insurance or VAT?

No. AIA reduces taxable trading profit — so it lowers Corporation Tax (for companies) or Income Tax (for sole traders/partnerships). It has no effect on VAT (a separate tax recovered through input VAT on the invoice), Class 2 or Class 4 NICs on sole traders' profits beyond the indirect effect of reducing profit, or employer NICs.

Capital allowances planning is high-leverage. On a £500,000 spend, choosing the right relief mix is worth £30,000–£80,000 of present-value tax relief versus the wrong one. Always speak with a qualified UK tax adviser before any material capital project.

Educational content — not personal tax advice. Sources: GOV.UK Capital Allowances guidance, HMRC New first-year allowance & main rate WDA policy paper (Nov 2025), Finance Act 2025, ICAEW Tax Faculty, Deloitte Taxscape. Always verify on gov.uk before acting.

What to do now

The practical job is to map the estate properly before any death, transfer or trust charge happens. That means separating agricultural value from market value, checking tenancy start dates, identifying whether any land is under an environmental agreement, and reviewing whether any assets are actually BPR rather than APR. It also means checking lifetime gifts from 30 October 2024 onwards, because those gifts can now affect how much of the £2.5 million allowance is left.

Where the estate is complex, the figures should be modelled under the current HMRC apportionment approach rather than guessed. HMRC says its tool can be used where the estate has up to eight agricultural and eight business property assets; larger or more complex estates may need professional advice. That is a sensible dividing line, because once there are multiple farms, trusts, mixed assets or historical gifts, the ordering rules start to matter as much as the headline allowance.

Summary of key insights

APR has not disappeared, but it is no longer an unlimited 100% shelter for every qualifying farm asset. From 6 April 2026, the first £2.5 million of combined APR and BPR value gets 100% relief, and qualifying value above that generally gets 50% relief. Couples can still do well, especially where spouse exemptions and transferable allowances are used correctly. The main risks now are valuation mistakes, old tenancy assumptions, trust timing, and poor record-keeping around lifetime gifts and transfers.

Key Takeaways

- The Annual Investment Allowance provides 100% tax relief on qualifying plant and machinery expenditure up to £1 million per year. It has been permanently set at this level since April 2023.

- Cars, land, buildings, and assets already owned by connected parties do not qualify for AIA. Cars enter capital allowances pools based on CO2 emissions.

- Connected businesses must share the £1 million AIA limit. Two companies under common control have a combined cap of £1 million, not £1 million each.

- Integral features — electrical, heating, ventilation, cold water systems, and lifts — in commercial buildings qualify for AIA and should not be treated as structural expenditure.

- Zero-emission cars and vans attract a 100% first-year allowance separately from the AIA. This relief sits outside the £1 million cap and does not consume the AIA limit.

- For short accounting periods, the AIA is proportionally reduced. A six-month period has an AIA of £500,000.

- The AIA cannot be deferred — it must be claimed in the period the expenditure is incurred. Failure to claim in the correct period means the opportunity is permanently lost.

FAQs

Q1: Can a sole trader claim AIA on equipment purchased in the final weeks of their accounting year if the invoice has not yet been paid?

A1: Well, it is worth noting that the timing of an AIA claim depends on when the expenditure is incurred — not when it is paid. For most purchases, expenditure is incurred when the unconditional obligation to pay arises, which is typically when the contract is entered into or when the goods are delivered and title passes, whichever is later under the terms of the agreement. A sole trader who orders and receives equipment in late March, with an invoice dated in March that they pay in April, has incurred the expenditure in March — and that expenditure falls in the accounting period ending 5 April. The fact that payment follows in the next tax year does not push the expenditure into the later period. This distinction matters enormously when a business is trying to accelerate AIA claims into the current year. Conversely, equipment ordered and paid in March but not delivered until April is typically incurred in April when delivery and title transfer occur. The safest approach is to ensure both delivery and the contractual commitment occur before the year end where current-year AIA is needed. Keeping the delivery note, invoice, and purchase order dated consistently in the same period is good practice for avoiding any HMRC challenge on timing.

Q2: Does AIA apply to assets a business owner contributes from their personal ownership into a partnership or limited company?

A2: In my experience, this is one of the most frequently misunderstood aspects of AIA eligibility, and it catches business owners at the point of incorporation or when formalising a partnership. The AIA is available only on new expenditure — that is, money spent acquiring the asset from an unconnected third party during the accounting period. When a sole trader incorporates and transfers personally-owned assets into a new limited company, those assets enter the company’s capital allowances pool at their market value. However, because the transfer is between connected parties rather than a new purchase from the market, AIA cannot be claimed on that value. The same applies to a partner introducing assets into a partnership. The assets are eligible for writing-down allowances at the normal pool rates — 18% for main pool assets — but the AIA 100% first-year deduction is not available. This means a business owner who has, say, £80,000 of machinery that they transfer to a newly incorporated company at market value will receive only the first-year writing-down allowance of £14,400, not the full £80,000. Planning the timing of major asset purchases — buying directly through the company rather than personally and then transferring — avoids this problem entirely.

Q3: Can a landlord with a residential rental property claim AIA on furniture and white goods supplied to tenants?

A3: Well, this is an area where the rules are quite specific and where landlords often make costly assumptions. Residential landlords cannot claim AIA on assets they provide to tenants. Instead, they have access to the replacement of domestic items relief, which allows the cost of replacing existing items — furniture, appliances, curtains, soft furnishings — to be deducted against rental income in the year of replacement. The key word is replacement: this relief does not apply to furnishing a property from scratch, only to replacing existing items with equivalent ones. It is a revenue relief, not a capital allowance, and it sits within the rental income calculation rather than the capital allowances regime. For landlords who also operate furnished holiday lets, the position was different — FHLs did qualify for capital allowances including AIA on furniture and equipment. However, the FHL regime was abolished from April 2025, and from that date, former FHL properties are treated as standard residential lettings for tax purposes, which removes the AIA entitlement. Commercial landlords — those letting properties to businesses — can claim AIA on plant and machinery installed in their commercial properties, including integral features. The residential versus commercial distinction is therefore the starting point for any landlord wondering about capital allowances.

Q4: How does AIA work for a partnership where the partners have different profit-sharing ratios, and who claims the relief?

A4: Well, this is an area that trips up many partnership accountants. The AIA belongs to the partnership as a business entity, not to the individual partners in proportion to their profit shares. The partnership claims AIA in the partnership tax return, and the allowance reduces the taxable profit of the partnership as a whole. That reduced profit is then shared between partners according to their profit-sharing ratio for the period. So if a partnership spends £200,000 on equipment and claims £200,000 of AIA, the entire £200,000 reduces partnership profit before it is split. A partner with a 30% share benefits from 30% of the AIA-generated reduction — they are not entitled to their own separate AIA claim on top of the partnership’s claim. Where multiple partnerships are connected — for example, two farming partnerships with overlapping partners — the connected party rules require them to share the £1 million AIA limit. The allocation of the shared limit between the two partnerships is a matter for the partners to agree, but HMRC must be notified of the allocation if both partnerships are claiming AIA. In practice, the allocation should favour the entity with the higher corporation tax or income tax rate on its profits, to maximise the tax value of the relief used.

Q5: Is the AIA available on the purchase of a commercial property that includes plant and machinery, and how should the purchase price be split?

A5: In my experience, commercial property purchases are one of the most significant AIA opportunities that businesses fail to exploit fully, and the split of the purchase price is the critical exercise. When a business buys a commercial property, the purchase price covers land (no allowances), the building structure (SBA only at 3%), and embedded plant and machinery — primarily integral features such as electrical systems, heating, ventilation, and cold water systems. The portion of the purchase price attributable to qualifying plant and machinery can be claimed under AIA in the year of purchase, giving 100% immediate relief on that element. The challenge is establishing what proportion of the price relates to each category, and this requires a formal capital allowances survey by a surveyor or specialist adviser. The split is not arbitrary — it must be agreed with the seller at the point of sale through what is called a section 198 election, which fixes the values attributed to each category of allowance for both parties. If no section 198 election is made, the default rules apply and HMRC may dispute the split later. For a commercial property purchase of £500,000, a properly conducted survey might identify £80,000 to £120,000 of embedded plant and machinery — giving AIA relief worth between £15,200 and £22,800 at 19% corporation tax, or considerably more at 25%.

Q6: Can a business claim AIA on a second-hand asset purchased from an unconnected seller, and does it matter that the asset is not new?

A6: Well, it is worth noting that AIA is not restricted to new assets — it applies to second-hand plant and machinery purchased from unconnected parties in exactly the same way as brand-new equipment. A manufacturing company that buys a used lathe from another business for £40,000 can claim the full £40,000 under AIA in the year of purchase, provided the asset qualifies as plant or machinery and the seller is not a connected party. The condition that prevents AIA on second-hand assets is connection, not age. If a business buys used equipment from its own director, a connected company, or a related family member, AIA is not available and the asset enters the writing-down allowance pool instead. For an unconnected third-party seller — a liquidation sale, an auction, a trade-in arrangement, or a private sale — the AIA applies in full. This creates a planning opportunity for businesses looking to acquire well-maintained used equipment at below-new prices: the tax relief is identical to buying new, while the cash outlay is lower. One practical point to note: where an asset was previously used in a business for which capital allowances were already claimed, the seller’s allowances position is closed out on disposal, and the buyer starts fresh with their own AIA claim on the price they paid.

Q7: Does the AIA apply to software purchased by a business, and is there a distinction between off-the-shelf software and bespoke development?

A7: Well, this is genuinely one of the more technically nuanced areas of capital allowances, and the answer depends critically on the type of software involved. Off-the-shelf software — commercial products purchased or licensed for use in the business — is generally treated as plant and machinery and qualifies for AIA. This includes business software packages, subscription software that involves an upfront licence cost, and similar commercial products that a business buys to use as a tool in its trade. Bespoke software developed specifically for a business — commissioned development costs, internal development staff costs, and similar — is treated differently. Development costs of this nature may be treated as capital expenditure on an intangible asset rather than plant and machinery, in which case they fall under the intangible assets regime rather than capital allowances, and AIA does not apply. The distinction is whether the software results in the acquisition of a separate identified asset (bespoke development, likely intangible) versus the purchase of a tool or product (off-the-shelf, likely plant). The Research and Development tax relief regime can interact with software development costs for qualifying businesses, providing an alternative route to relief. A business investing heavily in software should review whether each category of expenditure falls under AIA, the intangibles regime, or R&D relief — they are not interchangeable and can produce very different relief amounts and timings.

Disclaimer

The information provided in this article is for general guidance only and is not intended to constitute professional advice, tax advice, financial advice, legal advice, or any other form of regulated guidance. Although every effort has been made to ensure accuracy at the time of publication, Fair View Accounting Services, including its director, employees, contractors, writers, and content-creation team, accepts no responsibility for any loss, damage, penalty, or consequence arising from reliance on the information contained herein.

UK tax legislation changes frequently, and HMRC interpretations, thresholds, and rules may vary depending on the individual circumstances of each taxpayer. Nothing in this article should be considered a substitute for obtaining formal, personalised advice from a qualified accountant or tax professional. Readers should not take action—or refrain from taking action—based solely on the content published on this website.

Fair View Accounting Services does not guarantee the completeness, accuracy, or ongoing validity of the information provided and assumes no liability for omissions or errors, whether typographical, factual, or technical. By using this content, the reader acknowledges that all responsibility for decisions remains solely with the user.