Understanding Your HMRC Tax Refund Deadline: How to Avoid Missing Out in the UK (2026/27 Guide)

Picture this. You’re staring at your payslip or self assessment calculation wondering, “Did I pay too much tax this year? Have I missed a refund I’m entitled to? And when is the deadline to claim it?” You’re not alone. Each year, thousands of UK taxpayers, whether employees, freelancers or business owners, discover they’ve overpaid income tax, but many lose money simply because they don’t act on time.

Let’s start with the big picture. In the 2026/27 tax year, millions of taxpayers have the chance to reclaim overpaid tax, yet many miss out due to misunderstandings around deadlines, eligibility, and how to check if they’re owed anything. This article will guide you through exactly what you need to know about HMRC’s tax refund deadline rules, how to verify your tax position step by step, and what practical action you can take, whether you’re an employee, self employed, or running your own business.

Understanding Your HMRC Tax Refund Deadline in 2026/27

Why You’re Searching for This: User Intent Behind “HMRC Tax Refund Deadline Warning”

Your intent is clear. You want practical, actionable advice on:

- How to check if you’ve overpaid tax in 2026/27 (or previous years)

- Understanding the deadlines HMRC sets for claiming tax refunds

- Calculating your accurate income tax liability

- Knowing where and how to correct mistakes caused by incorrect tax codes, multiple jobs, or self employment income

- Clarifying complex issues like the Scottish and Welsh tax rates, emergency tax codes, and the high income child benefit tax charge

- Real world examples and worksheets to help you get your tax affairs in check and understand whether to expect a refund or owe more

In short, you need a thorough, step by step explanation that matches your situation and walks you through practical next steps in plain English.

2026/27 Income Tax and Allowances at a Glance

Before jumping into refund deadlines, it pays to ground ourselves in the latest tax landscape for 2026/27 (effective from 6 April 2026 to 5 April 2027):

| Tax Band | Taxable Income (England, Wales, Northern Ireland) | Tax Rate |

|---|---|---|

| Personal Allowance | Up to £12,570 | 0% |

| Basic Rate | £12,571 to £50,270 | 20% |

| Higher Rate | £50,271 to £125,140 | 40% |

| Additional Rate | Over £125,140 | 45% |

Note: The Personal Allowance remains frozen at £12,570 for 2026/27 and, following the 2025 Autumn Budget, is now set to remain at this level until April 2031. The same freeze applies to the basic and higher rate thresholds. National Insurance thresholds are also unchanged this year, affecting both employees and the self employed.

Source: HMRC’s official 2026/27 tax tables at gov.uk/income-tax-rates.

How does this connect to your refund? Any misapplication of these bands or your allowances, especially if you have multiple jobs or additional income, could mean you’ve paid too much or too little tax. From 6 April 2026, dividend tax rates have also risen by 2 percentage points for basic and higher rate taxpayers (now 10.75% and 35.75% respectively), so anyone receiving dividend income from a limited company or share portfolio should double check their position.

Common Reasons Taxpayers Get Refunds (and Miss Them)

Some typical scenarios that lead to eligibility for a tax refund include:

- Incorrect tax codes. Sometimes HMRC issues emergency or wrong codes, causing automatic over deductions.

- Multiple jobs or pensions. Employees with two jobs or pensions often pay basic rate tax on one job and emergency tax on the other, leading to overpayment.

- Self employment errors. Underpayments or overpayments due to misreported income, expenses, or late submissions.

- Job changes partway through the year. New employers may apply default tax codes.

- Benefits, loans, or grants. Some income misclassifications trigger over or underpayments.

- The high income child benefit charge. When income rises above £60,000, repayments of child benefit through Self Assessment or PAYE must be made, and these are often incorrectly calculated.

- Gig economy earnings. Side hustles or irregular contract work can cause confusion at Self Assessment time.

In my years advising London based clients, I’ve seen a pattern. Many genuinely don’t realise they can claim back tax on underreported side income or because their employer applied the wrong code during a job switch.

How Does HMRC Set a Tax Refund Deadline?

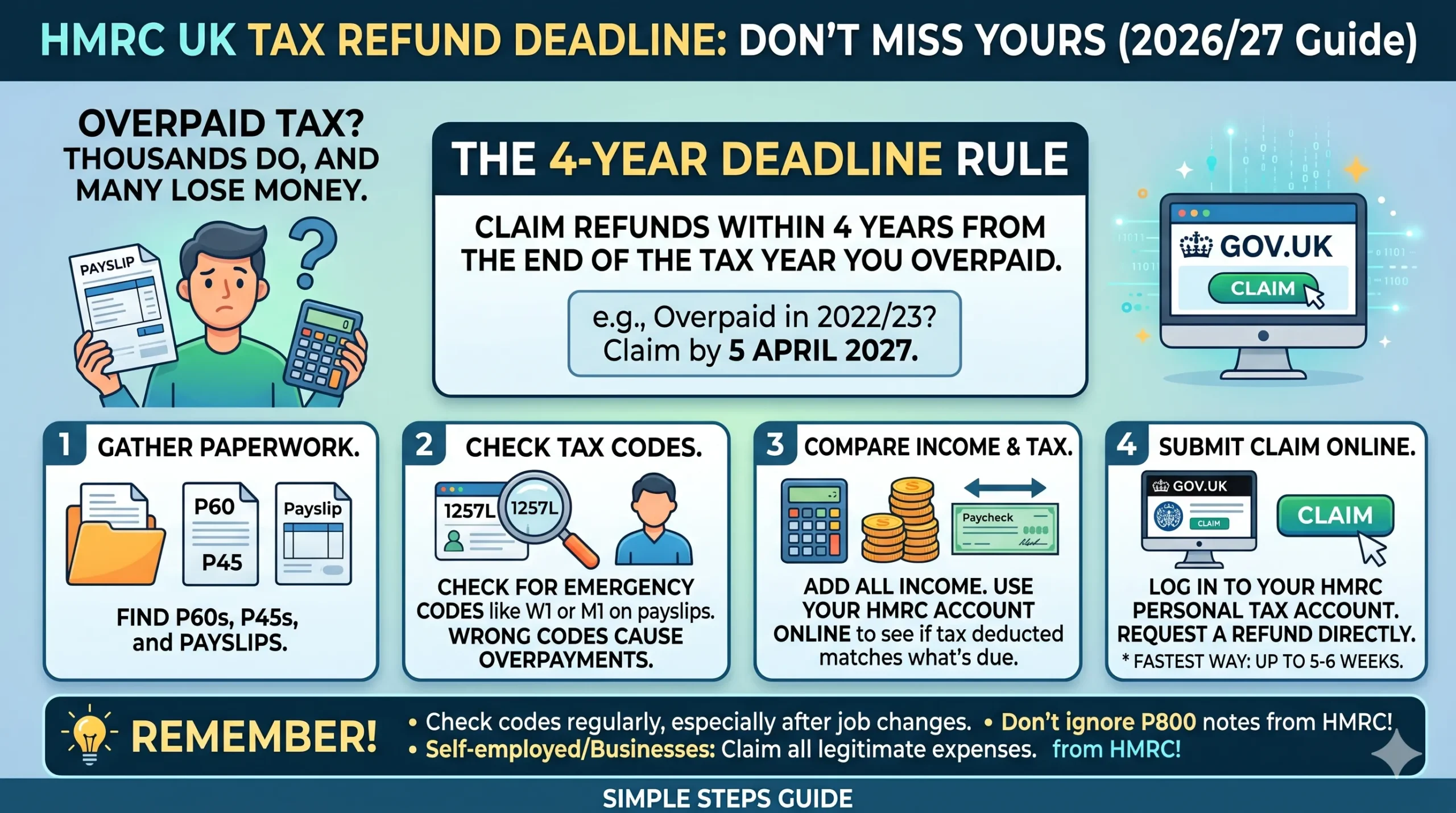

Here’s the crucial part many overlook. Generally, for income tax, you have 4 years from the end of the tax year in which you overpaid to claim a refund.

- For example, if you overpaid during the 2022/23 tax year (6 April 2022 to 5 April 2023), your deadline to claim a refund is 5 April 2027.

- For the current 2026/27 year, that means you have until 5 April 2031 to claim any overpayments.

If you miss this window, HMRC will usually not pay back the refund. Exceptions exist where you’ve made a mistake on a tax return or where HMRC made the error, which may extend the time limits (typically 12 months to notify specific errors).

How to Check if You Have a Refund Due: Step by Step Guide for UK Taxpayers

Don’t worry. It’s simpler than it sounds once you break it down.

Step 1: Gather your paperwork

- P60s (end of year statements from employers)

- P45s if you changed jobs mid year

- Payslips showing tax deductions

- Self Assessment tax returns and computations (if applicable)

- Bank statements or invoices for self employed income

Step 2: Check your tax code(s)

Your tax code informs your employer how much tax free pay you receive. Use your recent payslip or check your personal tax account online at gov.uk/personal-tax-account to verify your current code. Think of your tax code like a postcode for your income. It tells HMRC precisely which allowances apply to you.

Emergency tax codes often look like 1257L W1 or 1257L M1 (week 1 or month 1 basis). If you’ve been taxed on an emergency code for too long, that probably means overtaxation.

Step 3: Calculate your total taxable income

Add together all salary and other taxable benefits. For the self employed, use turnover minus allowable expenses.

Step 4: Apply the 2026/27 tax bands and personal allowance

Using the table earlier, deduct your personal allowance (£12,570 if applicable), then tax the remaining at 20%, 40%, or 45%.

Here’s a simple worksheet snippet you can fill in:

| Item | Amount (£) |

|---|---|

| Total employment income | |

| Self employment income | |

| Investment or dividend income | |

| Less personal allowance | £12,570 |

| Taxable income | (Calculate) |

Then apply:

- 20% on income up to £50,270

- 40% on income from £50,271 to £125,140

- 45% on income over £125,140

Multiply the respective bands by the rates, then sum the tax due.

Step 5: Compare tax deducted so far

Look at your P60 or tax calculation statement. Has your “tax deducted” exceeded the total tax due from step 4? If yes, you’re owed a refund.

Special Considerations

Multiple income streams

If you have a job plus self employment income, HMRC’s Pay As You Earn (PAYE) system may struggle to get your tax bands right on your employment income, often under taxing or over taxing your self employment income.

Scottish and Welsh variations

Scottish taxpayers continue to pay different rates ranging from 19% to 48% across six bands in 2026/27. Welsh taxpayers follow the same rates and bands as the rest of the UK (excluding Scotland), as the Senedd has kept Welsh rates at 10p in each band for the eighth consecutive year.

Example Scenario: Sarah from Manchester

Sarah works two part time jobs. One applies a standard tax code, the other has erroneously taxed her on an emergency code all year. She noticed that the total tax deducted across both jobs exceeds what her total income tax should be under the 2026/27 bands. After reviewing her HMRC personal tax account and using a simple tax calculation worksheet, she discovered she had overpaid £850. Rather than waiting, Sarah contacted HMRC and claimed the refund well before the 4 year deadline.

How Businesses and Self Employed Can Avoid Tax Refund Pitfalls

If you run a business or are self employed, the situation can be more complex. Expenses, allowances, and accurate income reporting can all affect your tax bills and potential refunds.

For example:

- Do you know which expenses you can deduct legitimately?

- Are you aware that applying a flat rate or simplified expenses might reduce your taxable profit?

- Have you kept records to justify capital allowances on equipment?

With Making Tax Digital for Income Tax Self Assessment now mandatory for many sole traders and landlords with qualifying income above £50,000 from April 2026, keeping accurate digital records has become more important than ever.

Step by Step: Using HMRC’s Personal Tax Account to Check Your Status

- Register or log in to your personal tax account at gov.uk/personal-tax-account

- Review your employment income and tax code details

- Check if HMRC has flagged any under or overpayments

- Use the available calculators to input your income and expenses

- Request a refund online or via paper for older years

Don't Leave Your Money

With HMRC

In 2026/27, millions of UK taxpayers are eligible for refunds due to frozen allowances and complex regional codes. Discover how to check your status and beat the 4-year deadline.

The 2026/27 Tax Landscape

The UK tax system is currently defined by a freeze on the Personal Allowance at £12,570. As wages rise while thresholds remain static, more taxpayers are pushed into higher bands, increasing the likelihood of payroll errors and incorrect emergency codes.

Income Bands (England, Wales, NI)

Frozen Thresholds

The Personal Allowance is set to remain at £12,570 until April 2031. This "fiscal drag" is a primary reason for unexpected tax bills and overpayments.

Dividend Update

From April 2026, dividend rates rose by 2%. Basic rate: 10.75%, Higher rate: 35.75%. Ensure your share portfolio tax is accurately reported.

Regional Variations: The Coding Trap

Taxpayers in Scotland face six distinct bands, while Wales maintains parity with England but under its own administration. If your tax code doesn't start with 'S' (Scotland) or 'C' (Wales) when it should, you are likely paying the wrong amount.

Why Refunds Happen

-

⚡

Emergency Codes 1257L W1/M1 codes often overtax you for months after a job change.

-

⚡

Multiple Jobs HMRC often applies the full allowance to one job, leaving the second overtaxed.

-

⚡

Unclaimed Expenses Freelancers often forget home office or travel costs in Self Assessment.

The High Income Child Benefit Trap

If your income exceeds £60,000, you must repay a portion of your Child Benefit. This "sliding scale" clawback reaches 100% at £80,000. Many parents are hit with surprise tax bills because this isn't automatically deducted from their PAYE salary.

Your 4-Year Claim Window

Overpayment Year

The tax year you paid too much (e.g., 2022/23).

Active Monitoring

Check your Personal Tax Account for P800 notices.

The Hard Stop

April 5th, exactly 4 years after the year end.

Claim Forfeited

After this date, HMRC legally retains your overpayment.

Ready to Claim?

Most refunds take 5-6 weeks to process. Using the online "Personal Tax Account" is the fastest route to getting cash back into your bank account.

Refund Form Checklist

| Situation | Form |

|---|---|

| Left work mid-year | P50 |

| Student finished job | P53 |

| Moving abroad | P85 |

| Self Assessment | Online Return |

How to Claim Your HMRC Tax Refund: Practical Steps, Deadlines & Pitfalls for UK Taxpayers and Business Owners (2026/27)

None of us loves tax surprises, but here’s some good news. If you’ve paid too much tax in 2026/27 (or previous tax years going back 4 years), you can claim a refund from HMRC provided you do it on time. The key is understanding how to spot an overpayment, how to claim your money back, and what deadlines you must respect to avoid losing out. Building on everything covered in Part 1, this second part dives deeply into the refund claim process for employees, self employed people, and business owners, with practical guidance, checklists, and real world examples drawn from over 18 years of advising clients across the UK.

When and How to Claim an HMRC Tax Refund

How Long Do You Have to Claim?

You typically have four years from the end of the relevant tax year to claim a refund.

- Example: For the 2022/23 tax year (6 April 2022 to 5 April 2023), you have until 5 April 2027.

- For the current 2026/27 year, that means you can submit refund claims up to 5 April 2031.

This deadline holds for most refund claims, whether you’re a PAYE payer or a Self Assessment filer. If you miss this window, HMRC will usually decline your claim. Exceptions exist for some error corrections, but generally act within this four year period for peace of mind.

Claiming Refunds as an Employee (PAYE)

Most employees overpay tax due to incorrect codes or changing jobs. HMRC recognises this and has streamlined refund routes to make claiming easier. Here are your key options:

Automatic refunds via PAYE code correction

If HMRC adjusts your tax code during the year (for example, from emergency to correct code), the overpaid tax is usually refunded through your pay in the next one or two pay periods. This is the simplest way refunds happen without you lifting a finger.

Claiming via HMRC personal tax account

If HMRC has not automatically corrected your tax code or refunded overpayments, you can check and claim through your personal tax account online at gov.uk/personal-tax-account. Log in with your Government Gateway ID, review the “Check how to claim a tax refund” tool, and follow the prompts. You’ll need details like your P60, P45, or payslips to hand.

Submitting form P50 (if you have left work and won’t be working again in the tax year)

This is useful if you left your job early in the tax year and believe you overpaid. You can submit online or by post, and HMRC typically processes refunds within five to six weeks.

If you receive a P800 notice

HMRC sends this when it thinks you have a tax refund or bill after the tax year ends. Since the changes that took effect from 31 May 2024, you must claim P800 refunds online (or by phone) rather than waiting for an automatic cheque in most cases. If you don’t claim your P800 refund online within 45 days, HMRC will then issue a cheque to your registered address, but the online route remains the fastest, often crediting your bank within five working days. Don’t ignore P800 notices. Act promptly to avoid losing your refund.

Self Employed and Business Owner Refunds: Special Considerations

The self employed must be extra vigilant with refunds due to more complex income and expenses reporting. Key points:

- You may have overpaid tax if you claimed insufficient allowable expenses or did not include reliefs like trading losses or pension contributions.

- Recalculating your taxable profit carefully is vital. I’ve seen clients miss out on hundreds or thousands of pounds by underclaiming legitimate expenses like home office costs, travel, and equipment depreciation.

- Filing a correct and complete Self Assessment tax return promptly triggers automatic refunds if you overpaid.

- If you have multiple sources of income, such as employment plus self employment, you must ensure correct payments on both, or risk over or underpayments.

- Early tax payments on account can lead to refunds if your profits fall short during the year.

Step by Step Guide: Claiming an HMRC Tax Refund (Employees and Self Employed)

Step 1: Confirm your total income and tax paid

Collect P60s, P45s, payslips, and (if self employed) your accounts. Sum all taxable income streams.

Step 2: Check your applicable personal allowance and tax bands

For 2026/27, most UK taxpayers enjoy the £12,570 personal allowance. Use the 2026/27 brackets for your calculations (see the table in Part 1).

Step 3: Calculate your expected tax liability

Use the rates from earlier. Deduct any allowable expenses or reliefs.

Step 4: Compare with tax paid (from P60, Self Assessment statement, or payslips)

If the tax paid is greater than your calculated liability, you’ve likely overpaid.

Step 5: Log into your personal tax account or prepare required forms

PAYE employees use HMRC digital services or form P50 if eligible. Self employed taxpayers rely on Self Assessment returns or may request refunds by letter if filing errors are corrected later.

Step 6: Submit your refund claim

Ensure supporting documents like payslips and expense receipts are accessible in case HMRC requests verification.

Step 7: Await processing

Expect around five to six weeks for refund processing via HMRC digital routes. Postal claims or complex cases may take longer. Provide correct bank details to expedite direct payments.

Example: Mark, the Freelancer with Multiple Income Streams

Mark from Bristol is self employed as a graphic designer but also does some part time bookkeeping for a local firm. His employer deducts tax via PAYE, but Mark’s freelance income is reported annually. When Mark did his 2025/26 Self Assessment, he initially missed claiming some home office expenses. Upon review, he amended his return and included these, reducing his taxable profit. As a result, Mark was entitled to a refund of £750 for 2025/26. He submitted the amendment online, and HMRC confirmed the credit within six weeks, paying the refund directly to his bank.

Crucial Checklists for Avoiding Common Pitfalls

For employees

- Check your tax code every year, especially after job changes.

- Look out for emergency tax codes like 1257L W1.

- Review your P60 for consistency at year end.

- Use your personal tax account regularly.

For self employed and business owners

- Always claim all genuine business expenses.

- Keep detailed records (receipts, invoices) for HMRC verification.

- Review your tax calculation before submitting your Self Assessment.

- Pay close attention to taxes on payments on account.

- Submit amendments promptly if mistakes are found.

Table: Examples of Forms Used to Claim Refunds (2026/27)

| Your Situation | Form or Method | Notes |

|---|---|---|

| PAYE employee, left work mid year | P50 | Claim refund if no further work in year |

| Student who stopped working | P53 | Claim refund for that tax year |

| Self Assessment filer | Online Self Assessment filing | Automatic refunds if overpaid |

| Ongoing PAYE job, incorrect tax code | Personal tax account or contact HMRC | Refund given via payroll adjustment or direct payment |

| Left UK and want refund | P85 | Submit to claim any due refund |

What Happens If You Miss the Refund Deadline?

Unfortunately, if the 4 year deadline passes, HMRC will usually reject the refund claim. This is why it’s vital to:

- Review your tax position annually

- Act promptly on P800 notifications or notices from HMRC

- Be proactive in checking your personal tax account online at gov.uk/personal-tax-account

HMRC Tax Refund

Deadline Tracker

A complete interactive guide for UK employees, freelancers and business owners. Check what you're owed before HMRC closes the door.

Find Your Refund Deadline

HMRC gives you four years from the end of the tax year to claim overpaid income tax. Miss it, and the money is gone for good.

Pick the tax year you overpaid in

At a glance

| Tax Year | Year End | Claim By |

|---|---|---|

| 2022/23 | 5 Apr 2023 | 5 Apr 2027 |

| 2023/24 | 5 Apr 2024 | 5 Apr 2028 |

| 2024/25 | 5 Apr 2025 | 5 Apr 2029 |

| 2025/26 | 5 Apr 2026 | 5 Apr 2030 |

| 2026/27 | 5 Apr 2027 | 5 Apr 2031 |

Source: gov.uk/claim-tax-refund

2026/27 Tax Bands Calculator

Enter a gross annual income to see how it splits across the bands. Toggle between rest-of-UK and Scotland.

England, Wales & Northern Ireland

You'll see six bands ranging from 19% to 48% for 2026/27. The Scottish Government raised the starter and basic rate thresholds by 7.4% this year. Your tax code starts with "S".

Welsh rates are still set at 10p in each band, so you pay the same overall rates as England and NI. Your tax code starts with "C".

Between £100,000 and £125,140 your Personal Allowance tapers away, creating an effective marginal rate of around 60%. Pension contributions can pull you back below £100k.

Are You Owed a Refund?

Five quick questions. No personal data leaves this widget.

High Income Child Benefit Charge

If you or your partner earn more than £60,000, you may owe some Child Benefit back. Work out the impact in seconds.

Income vs charge band

Child Benefit 2026/27: £27.05/week first child, £17.90/week each additional child.

How the charge works: 1% of total Child Benefit clawed back for every £200 of income above £60,000. Full clawback at £80,000.

New for 2025/26 onwards: You can now pay the HICBC through your PAYE code rather than only via Self Assessment.

Tax Code Decoder

Spot an emergency or wrong code on your payslip before it costs you. Click any code to read what it means.

The Refund Process, End to End

From spotting an overpayment to money in your bank account.

-

1

Gather your paperwork

P60s, P45s, payslips, Self Assessment computations and any expense receipts for the year you're checking.

-

2

Verify your tax code

Sign in to your Personal Tax Account at gov.uk/personal-tax-account. Watch out for W1, M1, BR and 0T codes left in place too long.

-

3

Run the maths

Apply the 2026/27 bands (or Scottish bands) to your taxable income. Compare to what was actually deducted on your P60.

-

4

Choose your route

PAYE only? Claim through the Personal Tax Account or by phone. Left work mid-year? Form P50. Left the UK? Form P85. Self-employed? Amend your Self Assessment.

-

5

Submit and wait

Online P800 claims hit your bank in around 5 working days. Postal or complex cases take 5 to 6 weeks. Self Assessment amendments typically clear within 6 weeks.

-

6

Mind the deadline

Four years from the end of the tax year. Miss it and HMRC keeps the money, with very few exceptions.

Frequently Asked Questions

Quick answers to the questions clients ask most.

Can I change my tax code if it's wrong?

What happens if I've underpaid tax across multiple jobs?

Can I claim overpaid National Insurance back too?

Do Scottish or Welsh rates change the refund deadline?

Are there any exceptions to the four year rule?

I left the UK mid-year. Am I due a refund?

Just registered for Self Assessment. Can I still claim older refunds?

What happens if I ignore a P800?

Advanced HMRC Tax Refund Checks: Multi Income, Scottish & Welsh Variations, Emergency Tax & High Income Child Benefit Charge Explained (2026/27 UK Guide)

Be careful here, because I’ve seen clients trip up when juggling multiple incomes, navigating regional tax differences, or dealing with emergency tax codes. This final section digs deeper into those complex, often overlooked refund scenarios that can genuinely cost UK taxpayers and business owners hundreds or thousands of pounds if not handled correctly, especially as tax rules subtly shift in 2026/27.

Handling Multiple Income Sources: Why Tax Errors Happen & How to Fix Them

If you’re balancing employment with self employment, multiple jobs, pensions, or rental income, HMRC’s calculations can easily go awry. Why? Because each income stream is taxed differently and often via different systems (PAYE for employment, Self Assessment for freelancing).

Common issues include:

- Multiple jobs under PAYE. HMRC often applies your personal allowance to your primary job only. The secondary job may be taxed on an emergency code or at basic rate without allowances, causing overpayment.

- Employment plus self employment. Self employed income taxed through Self Assessment might not trigger accurate PAYE code adjustments, resulting in under or overpayments.

- Pensions and investments plus work income. Overlapping income reporting can distort tax bands and overtax you.

Here’s an original checklist to audit multiple income tax situations:

| Step | Action |

|---|---|

| Identify all income streams | List all jobs, pensions, self employment, dividends |

| Check tax codes on all PAYE jobs | Confirm none are emergency codes unless justified |

| Calculate combined taxable income | Use 2026/27 tax bands and allowances |

| Check if tax paid matches expected liability | Compare aggregated tax paid from payslips and returns |

| If overpaid, claim refund via Self Assessment or HMRC account | Follow refund steps from Part 2 |

Scottish and Welsh Taxpayer Variations in 2026/27

If you live in Scotland or Wales, tax rates and bands can differ from the rest of the UK, which often causes confusion when checking refunds.

- Scottish rates. There are six bands ranging from 19% (starter rate) to 48% (top rate). For 2026/27, the Scottish Government raised the starter and basic rate band thresholds by 7.4%, while keeping the higher, advanced, and top rate thresholds frozen.

- Welsh rates. The Senedd has again set Welsh rates of income tax at 10p in each band, so Welsh taxpayers continue to pay the same overall rates as those in England and Northern Ireland.

If HMRC or your employer uses the wrong regional rates or tax codes, you could be over or under taxed. For example:

| Jurisdiction | Band Threshold (2026/27) | Basic Rate | Higher Rate | Top Rate |

|---|---|---|---|---|

| England, Wales, NI | £12,571 to £50,270 | 20% | 40% | 45% |

| Scotland (starter to basic) | £12,571 to £16,537 | 19% (starter) | 42% (higher from £43,663) | 48% (top, above £125,140) |

Always confirm your residency status and tax codes with HMRC through your personal tax account at gov.uk/personal-tax-account to avoid misapplication. Scottish taxpayers should have a tax code starting with “S”, and Welsh taxpayers should see a code starting with “C”.

Emergency Tax Codes: Why They’re a Trap and How to Escape Them

When starting a new job or during tax code uncertainty, HMRC issues emergency tax codes (for example, 1257L W1, 1257L M1, or 0T), which assume no prior income and tax on a week or month basis rather than cumulative. This simplifies HMRC’s work but often overtaxes you until corrected.

Key points from experience:

- Emergency codes often stay in place for months if employees don’t check their payslips.

- Overpayment accumulates unnoticed, sometimes waiting years before refund claims are made.

- Switching between jobs multiple times can compound emergency code errors.

What to do:

- Check your tax code regularly, especially after job changes.

- If you’re still on an emergency code past the first month or two, contact HMRC or your employer’s payroll team immediately.

- Use your personal tax account online to check and request corrections.

- Claim retrospective refunds for overpayments after the tax year end if not adjusted in year.

High Income Child Benefit Charge (HICBC)

A less well known trap for many. The threshold was raised in April 2024 and remains the same for 2026/27. If you or your partner’s adjusted net income exceeds £60,000, the high income child benefit charge kicks in, clawing back some or all of the child benefit received.

- The charge is 1% of child benefit received for each £200 of income above £60,000.

- It reaches 100% clawback at £80,000.

- Child benefit for 2026/27 is £27.05 per week for the first or only child and £17.90 per week for each additional child.

- From summer 2025, HMRC introduced an option to pay the HICBC through your PAYE tax code rather than only through Self Assessment, which helps employees with otherwise straightforward affairs avoid filing a return purely for this charge.

- Many taxpayers still fail to anticipate the HICBC when submitting Self Assessment, leading to unexpected tax bills.

- Overpayment of child benefit due to unreported income changes can trigger penalties.

You can find more on the official rules at gov.uk/child-benefit-tax-charge.

Real World Case Study: Emily’s Journey from Emergency Tax to Tax Refund

Emily, working in Glasgow, jumped from a temporary retail assistant position to a permanent admin role in 2025. Her new employer put her on an emergency tax code for six weeks, during which she overpaid £400 in tax. On top of that, Emily’s side hustle selling crafts online was reported late in her 2025/26 Self Assessment, meaning she paid insufficient tax earlier. By actively reviewing her HMRC tax code and Self Assessment in early 2026, Emily identified these issues. She contacted HMRC to correct her code and claimed a refund for the overpaid employment tax while adjusting her self employment tax liability accurately. This saved her almost £1,200 in overpaid taxes and interest charges.

Comprehensive Worksheets for Your Tax Refund Check (2026/27)

Income and Tax Paid Worksheet

| Income Source | Amount (£) | Tax Paid (£) | Tax Code Used | Notes or Allowable Expenses |

|---|---|---|---|---|

| Salary (Job 1) | ||||

| Salary (Job 2) | Check tax code carefully | |||

| Self employed profits | N/A | Include actual profit minus expenses | ||

| Dividends | ||||

| Pension income | ||||

| Other income | e.g. rental, investment |

Top 10 Key Takeaways: Don’t Miss Your HMRC Tax Refund

- Verify your tax codes regularly to avoid overpayment caused by emergency or incorrect codes.

- Keep detailed records of all income streams and expenses to ensure accurate Self Assessment calculations.

- Use HMRC’s personal tax account online to monitor your tax liability and claim refunds.

- Remember the four year deadline to claim tax refunds from the end of the relevant tax year.

- Multiple income sources require close attention to tax bands and code applications to avoid errors.

- Scottish and Welsh taxpayers should confirm correct regional rates and codes, as different rules apply.

- Emergency tax codes can cause substantial overpayments, so be proactive in resolving them.

- The high income child benefit charge can cause unexpected tax bills and reduce child benefit payouts.

- Self employed and business owners must claim all allowable expenses to minimise taxable profits properly.

- Promptly act on HMRC P800 notices and other communications to claim refunds or resolve underpayments.

FAQs

Q1: Can someone change their tax code if it’s incorrect, and how does this affect refund deadlines?

Yes. HMRC can amend your tax code if it’s wrong, which often triggers a refund via adjustments in your payslip. However, it’s crucial to spot an incorrect code early. If left uncorrected, you might overpay tax and risk delays in claiming refunds. The four year refund claim deadline runs from the end of the relevant tax year, so promptly requesting a code change maximises your chances of reclaiming overpaid tax within that time.

Q2: What happens if tax is underpaid due to having multiple jobs, and can this affect refund deadlines?

Underpayment frequently occurs when your personal allowance applies fully to one job, leaving other jobs taxed at emergency rates or basic rates without allowances. This might not warrant a refund but rather a tax bill. Act swiftly to notify HMRC, as balancing payments must be settled by set deadlines (generally 31 January after the tax year), or penalties may apply. Refund deadlines don’t apply here unless tax is subsequently overpaid.

Q3: Are there special tax refund considerations for self employed individuals with fluctuating incomes?

Definitely. Fluctuating income complicates estimated tax payments and can cause over or underpayments. Self employed taxpayers should review their actual annual profits versus payments on account. If profits are lower, a refund might be due, but it must be claimed by amending your Self Assessment within four years. Missing this window forfeits potential refunds even if you overpaid substantially.

Q4: Can overpaid National Insurance Contributions (NICs) be reclaimed alongside income tax, and do the same deadlines apply?

Yes. NIC overpayments, common when switching jobs or due to multiple employers, can be reclaimed. However, these refunds are subject to slightly different deadlines and processes. Employees usually have six years from the end of the relevant tax year to claim NIC refunds, which differs from the four year window for income tax. It’s worth monitoring both deadlines carefully to avoid losing entitlements.

Q5: How do regional differences, like Scottish or Welsh tax rates, impact refunds and deadlines?

Scottish taxpayers face distinct income tax bands and rates compared with the rest of the UK, and Welsh taxpayers’ rates, although currently the same as those in England and Northern Ireland, are administered separately. Erroneous tax code applications can lead to overpayments, but refund deadlines remain consistent at four years from the tax year end. Check your regional tax codes frequently (Scottish codes start with “S”, Welsh codes with “C”) and report discrepancies promptly to claim refunds within the allowed timeframe.

Q6: Is there an exception to the four year tax refund claim deadline for mistakes made by HMRC or the taxpayer?

Yes. If an error was made by HMRC or the taxpayer deliberately concealed information, additional rules apply. For accidental mistakes notified within 12 months, you might qualify for extended time to claim refunds. Intentional errors can limit or prevent claims altogether. Always act quickly on notices and seek expert advice if unsure.

Q7: How does moving abroad mid tax year affect UK tax refund deadlines and claims?

Leaving the UK partway through a tax year complicates tax residency and liability. You may be eligible for a refund if you overpaid for the portion of the year you didn’t reside in the UK. Typically, you’ll need to submit form P85 or file a Self Assessment, ensuring claims are made within the four year window from the tax year’s end in which you left.

Q8: Can freelancers or gig workers who recently registered for Self Assessment still claim refunds for older tax years?

Yes. New registrants can claim refunds for up to four years prior to registration, provided evidence of overpayment exists. Consider a freelancer in Leeds who registered in 2026 but discovers an overpayment from 2023/24. They must still file an amended return or contact HMRC to claim refunds, with the four year limit strictly applied.

Q9: Are refunds automatically issued after submitting a Self Assessment, or must taxpayers proactively claim them?

After filing a Self Assessment, refunds for genuine overpayments are typically processed automatically, but it can vary. Complex returns or amendments might delay this. Always review your tax calculation summary, and if no refund is forthcoming within a reasonable timeframe (usually six weeks), contact HMRC directly to chase payments.

Q10: What are the risks of ignoring a P800 notice, and does it affect refund deadlines?

A P800 notice suggests you likely have a tax refund or a bill. Ignoring it risks missing time sensitive refund claims because HMRC moved to a system where you must actively claim refunds online (after 31 May 2024), rather than receiving automatic payments by cheque in the post. While HMRC will eventually issue a cheque if you don’t claim online within 45 days, acting promptly through your personal tax account ensures you reclaim overpayments within the four year deadline and receive the money far faster.

Disclaimer

The information provided in this article is for general guidance only and is not intended to constitute professional advice, tax advice, financial advice, legal advice, or any other form of regulated guidance. Although every effort has been made to ensure accuracy at the time of publication, Fair View Accounting Services, including its director, employees, contractors, writers, and content-creation team, accepts no responsibility for any loss, damage, penalty, or consequence arising from reliance on the information contained herein.

UK tax legislation changes frequently, and HMRC interpretations, thresholds, and rules may vary depending on the individual circumstances of each taxpayer. Nothing in this article should be considered a substitute for obtaining formal, personalised advice from a qualified accountant or tax professional. Readers should not take action—or refrain from taking action—based solely on the content published on this website.

Fair View Accounting Services does not guarantee the completeness, accuracy, or ongoing validity of the information provided and assumes no liability for omissions or errors, whether typographical, factual, or technical. By using this content, the reader acknowledges that all responsibility for decisions remains solely with the user.