Inheritance Tax Pension Rules Changes

Understanding UK Inheritance Tax Pension Rules Changes 2025-26: Core Facts and Basics

What Are the Key Changes to Pension Rules and Inheritance Tax?

From April 6, 2025, UK inheritance tax (IHT) rules undergo significant reform, especially affecting pensions. Notably, from April 6, 2027, unused pension funds and death benefits will be included in the deceased’s estate for IHT purposes, potentially facing a 40% tax charge. This represents a major shift because until now, unused pension funds were generally exempt from inheritance tax liabilities. These changes mean a higher tax burden and new planning challenges for pension holders and their beneficiaries. HMRC confirms death in service and relevant life plans remain IHT-exempt, offering some relief options.

UK-Specific Statistics and Facts on the New Pension IHT Rules

For context, an estate’s liability to inheritance tax will also be tied more strictly to UK tax residence status instead of domicile from April 2025 onwards. Individuals resident in the UK for at least 10 of the prior 20 years are liable on worldwide assets while non-residents pay IHT only on UK assets for up to 10 years after leaving. Estates over £1 million will face IHT on pensions and other assets, with tapering allowances applying under the new rules after April 2026. Additionally, dependants over age 75 drawing pensions can face combined IHT and income tax liabilities of up to 67%, a significant increase from previous norms.

Basics of the Inheritance Tax Shift: Residence Basis and Pension Inclusion

Think of your tax responsibility like a postcode for your financial affairs. Previously, inheritance tax was tied largely to your domicile (essentially your permanent home country). Now, from April 6, 2025, it will depend on UK tax residence status, meaning you’re liable on your worldwide assets if you have been a UK resident for enough years. This simplifies some aspects and complicates others, especially for those who move between countries.

How Does Including Unused Pension Funds Affect You?

Unused pension funds were a safe harbour from IHT, but as of April 2027, these will count as part of your estate. Picture your pension pot as a treasure chest; if it’s untouched at death, HMRC now wants a share. This can lead to a 40% IHT charge that families must plan for carefully, especially if the deceased was over 75, where additional income tax burdens arise for beneficiaries.

Practical First Steps in Navigating New Rules

Many clients forget that pension pots are now on the IHT radar, which can drastically affect how much inheritance is passed on. It’s wise to start reviewing your pension arrangements and overall estate strategy soon to consider possible tax-saving measures like trusts, or pension drawdown strategies that might reduce the taxable value of a pension at death.

What Are Some Immediate Planning Considerations?

- Review your UK residency status and how the new residence-based IHT will affect your liability.

- Collaborate with advisory professionals to assess the impact of unused pension inclusion on your estate.

- Consider adjusting your pension drawdown or beneficiary nominations to minimize tax impacts.

- Stay informed on transitional rules that apply to estates with valuations over the new £1 million cap.

This introduction has laid the foundation on the evolving pension and inheritance tax landscape in the UK for 2025-26, setting the stage for more practical, advanced insights and planning advice in the following sections.

What Are the New Caps on Business and Agricultural Property Reliefs?

From 6 April 2026, the UK government introduces a £1 million cap on the combined value of property qualifying for 100% Business Property Relief (BPR) and Agricultural Property Relief (APR). Previously, these reliefs were uncapped, allowing full exemption from inheritance tax on qualifying assets regardless of size. Now, only the first £1 million of combined qualifying assets will receive 100% relief; any amount above this threshold will attract a reduced relief of 50%, effectively doubling the inheritance tax rate on excess assets to 20%. This cap applies individually and to trusts, making careful planning essential to optimise relief usage.

How Does This Impact Business Owners and Agricultural Landowners?

Picture owning a thriving family business or valuable farming land — it used to be that all these assets could pass to your heirs free from inheritance tax, but not anymore in full. For businesses and farmers with assets exceeding £1 million, the new rules mean a higher IHT bill on anything above the cap, potentially affecting succession plans. This is especially crucial for family-run enterprises that rely on BPR and APR to preserve wealth across generations.

Key Features and Practical Considerations of the Relief Changes

Think of the £1 million cap like a tax-free zone for your prized business or farm assets. Up to this limit, 100% relief applies, letting these assets pass free of IHT. Beyond £1 million, assets qualify only for a 50% relief, leading to a 20% IHT charge. This allowance resets every seven years, similar to the nil-rate band, and is also subject to CPI inflation adjustment from April 2030. Importantly, the £1 million allowance is not transferable between spouses or between trusts settled by the same settlor.

How Are Trusts Affected?

Trustees now receive their own £1 million allowance for qualifying property, applicable to 10-year anniversary and exit charges. However, from 30 October 2024, this allowance is shared proportionally between multiple trusts established by the same settlor. Also, transfers of qualifying assets into trusts face stricter anti-forestalling rules, making timing critical to avoid unexpected IHT charges.

Practical Tax Planning Strategies for Business and Agricultural Owners

What Actions Can Owners Take Before the April 2026 Deadline?

Many clients overlook the benefit of making lifetime gifts of business interests or agricultural land into trusts before the relief cap takes effect. Since BPR and APR remain uncapped until 6 April 2026, gifting assets before this date can potentially lock in 100% relief and avoid entry charges. Owners should act swiftly with expert advice owing to the complex two-year ownership rule and anti-forestalling provisions.

Are There Structural Changes to Consider?

Families might explore restructuring ownership, such as through family investment companies, allowing more flexible succession planning and tax efficiency under the new relief limits. Reviewing shareholdings, adjusting trusts, or considering alternative business models help mitigate IHT exposure, although these strategies require professional guidance and tailored legal input.

How Does This Affect AIM-Listed Shares?

For shares admitted to trading on recognised stock exchanges but not listed (e.g., AIM), the rate of business property relief also drops from 100% to 50%. This adjustment affects investments in growth companies, making awareness of market status crucial for inheritance tax planning.

UK Inheritance Tax & Pension Reforms Guide

Navigating the critical changes to IHT rules between 2025 and 2027. Understand the new caps, the residence rules, and why your pension is no longer a safe harbour.

The Timeline of Change

The landscape of UK estate planning is shifting rapidly. Here are the core deadlines you need to prepare for.

April 6, 2025: Global Residence Rule

IHT liability switches from domicile to UK tax residence. Residents for 10 of the prior 20 years are liable on worldwide assets.

April 6, 2026: BPR & APR Caps

Introduction of the £2.5 million cap on Business and Agricultural Property Reliefs. Assets above this face an effective 20% IHT rate.

April 6, 2027: Pension Inclusion

Unused pension funds and death benefits enter the taxable estate, potentially facing a 40% IHT charge.

The End of the Pension Safe Harbour

Historically, unused pension pots were largely shielded from HMRC upon death. From April 2027, this changes drastically. Pensions will be treated as part of your taxable estate.

The "Double Tax" Threat

For dependents over age 75 drawing inherited pensions, funds can be subject to both a 40% IHT and up to 45% Income Tax on the remainder. This creates an effective tax rate of up to 67%.

- ✓ Included: Unused pension funds and standard death benefits.

- ✓ Exempt: Death-in-service benefits and relevant life plans.

Pension IHT Rate Change

The 67% Wealth Erosion (If Deceased >75)

The New Residence Rule

Inheritance tax liability is moving away from the concept of "domicile." It will now function much like a postcode for your financial affairs based on physical presence.

The 10 out of 20 Rule:

If you are a UK resident for at least 10 out of the last 20 years, your worldwide assets are liable for UK Inheritance Tax. Non-residents pay IHT only on UK assets for up to 10 years after leaving.

20-Year Residency Tracking

10 years of residency triggers global tax liability.

Business & Agricultural Property Reliefs

From April 2026, the uncapped 100% relief era ends. A new £2.5 million threshold will dictate the tax efficiency of business and farm successions.

The £2.5m Safe Zone

The first £2.5m of combined qualifying assets receive 100% relief. They pass to heirs free of IHT.

Spousal Transfer

Unused allowances are transferable between spouses, shielding up to £5 million combined.

The 20% Excess

Assets above the cap receive only 50% relief, resulting in an effective 20% inheritance tax rate.

Impact on a £4m Business

Under previous rules, a £4m qualifying business passed 100% tax-free. Under the new rules (assuming a single individual):

- First £2.5m (100% Relief) £0 Tax

- Remaining £1.5m (50% Relief) £300,000 Tax

AIM-Listed & EIS Shares Warning:

These shares drop to 50% relief immediately, bypassing the £2.5m allowance entirely. Market status awareness is critical.

Strategic Next Steps

Proactive planning is essential before the 2026 and 2027 deadlines. Consider these practical approaches with your advisory professionals.

Accelerate Lifetime Gifts

Transfer business or agricultural land into trusts before April 2026 to potentially lock in 100% relief (subject to 7-year survival).

Adjust Pension Drawdowns

Review drawdown strategies to minimize the taxable value of pensions at death, effectively managing the 40% threat.

Restructure Ownership

Explore Family Investment Companies (FICs) and adjust trust structures to maximize the new rolling allowances.

Significant Changes to Business Property Relief and Agricultural Property Relief

From 6 April 2026, the UK government introduces a £1 million cap on the combined value of property qualifying for 100% Business Property Relief (BPR) and Agricultural Property Relief (APR). Previously, these reliefs were uncapped, allowing full exemption from inheritance tax on qualifying assets regardless of size. Now, only the first £1 million of combined qualifying assets will receive 100% relief; any amount above this threshold will attract a reduced relief of 50%, effectively doubling the inheritance tax rate on excess assets to 20%. This cap applies individually and to trusts, making careful planning essential to optimise relief usage.

How Does This Impact Business Owners and Agricultural Landowners?

Picture owning a thriving family business or valuable farming land — it used to be that all these assets could pass to your heirs free from inheritance tax, but not anymore in full. For businesses and farmers with assets exceeding £1 million, the new rules mean a higher IHT bill on anything above the cap, potentially affecting succession plans. This is especially crucial for family-run enterprises that rely on BPR and APR to preserve wealth across generations.

What Is the Structure of the New £1 Million Allowance?

Think of the £1 million cap like a tax-free zone for your prized business or farm assets. Up to this limit, 100% relief applies, letting these assets pass free of IHT. Beyond £1 million, assets qualify only for a 50% relief, leading to a 20% IHT charge. This allowance resets every seven years, similar to the nil-rate band, and is also subject to CPI inflation adjustment from April 2030. Importantly, the £1 million allowance is not transferable between spouses or between trusts settled by the same settlor.

How Are Trusts Affected?

Trustees now receive their own £1 million allowance for qualifying property, applicable to 10-year anniversary and exit charges. However, from 30 October 2024, this allowance is shared proportionally between multiple trusts established by the same settlor. Also, transfers of qualifying assets into trusts face stricter anti-forestalling rules, making timing critical to avoid unexpected IHT charges.

What Actions Can Owners Take Before the April 2026 Deadline?

Many clients overlook the benefit of making lifetime gifts of business interests or agricultural land into trusts before the relief cap takes effect. Since BPR and APR remain uncapped until 6 April 2026, gifting assets before this date can potentially lock in 100% relief and avoid entry charges. Owners should act swiftly with expert advice owing to the complex two-year ownership rule and anti-forestalling provisions.

Are There Structural Changes to Consider?

Families might explore restructuring ownership, such as through family investment companies, allowing more flexible succession planning and tax efficiency under the new relief limits. Reviewing shareholdings, adjusting trusts, or considering alternative business models help mitigate IHT exposure, although these strategies require professional guidance and tailored legal input.

How Does This Affect AIM-Listed Shares?

For shares admitted to trading on recognised stock exchanges but not listed (e.g., AIM), the rate of business property relief also drops from 100% to 50%. This adjustment affects investments in growth companies, making awareness of market status crucial for inheritance tax planning.

Inheritance Tax & Pension Rules Changes

A comprehensive guide to the most significant overhaul of UK estate planning law in decades — what's changing, when, and what it means for you.

Key Dates at a Glance

The UK IHT reforms roll out in three distinct phases between 2025 and 2027. Understanding the timeline is the first step in planning effectively.

Pensions & Inheritance Tax from April 2027

The single biggest change: pension pots previously outside your estate will now count toward IHT calculations.

New rule (from 6 April 2027): Unused pension funds and death benefits will be counted as part of your estate and subject to 40% IHT above the nil-rate band — unless passed to a surviving spouse, civil partner, or registered charity.

| Asset | Value | IHT Before Apr 2027 | IHT From Apr 2027 |

|---|---|---|---|

| Family Home | £450,000 | Taxable | Taxable |

| ISAs & Savings | £100,000 | Taxable | Taxable |

| Inherited DC Pension | £650,000 | Exempt | Now Taxable |

| Own DC Pension | £200,000 | Exempt | Now Taxable |

| Total Estate | £1,400,000 | £500,000 taxable | £1,400,000 taxable |

| IHT Bill (est.) | — | £0* | ~£140,000 |

*Estate below combined nil-rate bands of £1M (couple transferring allowances). Post-2027 pension inclusion pushes estate well above threshold. Illustrative scenario only.

Business & Agricultural Property Relief Changes

From 6 April 2026, uncapped 100% relief ends. This affects family businesses, farms, and AIM share portfolios.

| Asset Value | Relief % | Effective IHT Rate | Status |

|---|---|---|---|

| First £1,000,000 | 100% | 0% | Maintained |

| Above £1,000,000 | 50% | 20% | New from Apr 2026 |

| AIM Shares (any value) | 50% (was 100%) | 20% | Reduced Apr 2026 |

| Death-in-Service Lump Sums | Full exemption | 0% | No change |

IHT Estate Estimator

Rough estimate of your potential IHT exposure under post-April 2027 rules. For illustration only — not tax advice.

Strategic Planning Actions

With major changes ahead, proactive planning is essential. Here are the most effective strategies to consider with your adviser.

Frequently Asked Questions

Answers to the most common questions about the 2025–2027 UK Inheritance Tax and pension reforms.

For general information only. Updated March 2026. Always seek qualified financial and legal advice.

Sources: HMRC gov.uk · Finance Bill 2025–26 · Royal London · Legal & General · Burges Salmon

Advanced Pension Inheritance Tax Planning Strategies in the UK 2025-26: Protecting Your Legacy Effectively

Key Changes Affecting Pension Inheritance from April 2027

From April 6, 2027, unused pension funds, including defined contribution schemes like SIPPs and SSAS, will be included in an individual’s estate for inheritance tax purposes at the standard 40% rate above the nil-rate band. This marks a major shift from prior rules where pensions were mostly exempt from IHT if the member died before age 75, with post-75 deaths facing income tax but not IHT. The new rule means that pension pots passing to anyone other than a spouse or civil partner will face IHT, increasing the tax liabilities for beneficiaries substantially. It’s important to note that spouse or civil partner transfers remain exempt.

Why This Matters for Your Estate and Beneficiaries

Imagine your pension as a sleeping giant now waking up in terms of tax exposure. Many people relied on pensions as a tax-efficient way to pass wealth to children or grandchildren; this legacy planning advantage diminishes significantly. In fact, if your estate, including pensions, exceeds the £325,000 nil-rate band (or £500,000 with the residence nil-rate band), your beneficiaries may face a double whammy of inheritance tax and, for those over 75, income tax on withdrawals from inherited pensions.

Strategic Pension Withdrawals Before Death

One effective approach is carefully timing pension withdrawals to reduce the value remaining in the pension pot at death. If you are in a lower income tax bracket before 75, consider drawing down funds strategically, which not only funds your lifestyle but reduces the pension value exposed to IHT. This approach requires balancing withdrawal rates, potential investment growth, and tax brackets in retirement years.

Using Spousal Bypass Trusts and Other Trust Vehicles

Spousal bypass trusts can be an invaluable tool allowing pension benefits to bypass the estate entirely, thereby reducing IHT exposure. By placing pension wealth into these trusts, you maintain control over the distribution, protect assets from future tax charges, and help ensure beneficiaries receive the intended legacy. It’s critical that nominations for pension beneficiaries align with trust arrangements to maximise tax efficiency.

Gifting and Pension Income Strategy

Using pension income during your lifetime to make gifts can help in two ways: reducing the pension pot and utilising the £3,000 annual gift exemption or other tax-free gift allowances. Many overlook this practical tactic, but it can significantly reduce the overall IHT bill when planned proactively. Professional advice ensures gifts are effective and compliant with HMRC rules.

Reassessing Pension Nominations

Regularly reviewing pension death benefit nominations ensures the right people or trusts inherit these assets tax efficiently. This is especially vital to avoid pension monies defaulting to estates, which now could incur higher IHT. Keeping nominations updated in line with new legislation and personal circumstances prevents unintended tax consequences and family disputes.

Considering Alternative Investments for IHT Efficiency

As pensions become more exposed to inheritance tax, some investors explore other vehicles like AIM portfolios (bearing in mind from April 2026 that BPR on AIM shares reduces to 50%), SEIS/EIS, and ISAs to diversify and maintain tax advantages in their overall estate planning strategy. These routes have different risk profiles and tax treatments but can be part of a holistic approach.

Navigating Complexity: Getting Professional Advice and Staying Informed

Given the intricate interplay between pensions, inheritance tax, trusts, and income tax, it’s wise to engage with financial advisers who understand the latest rules and can craft bespoke plans. Lived experience shows many estates face large unexpected tax bills because they relied on outdated assumptions around pension taxation.

Staying Ahead of Future Regulatory Changes

Tax policy evolves, and staying informed on government updates—via official HMRC guidance and trusted advisory firms—is key. Annual reviews of your pension and estate plan help adapt to shifting rules, identify emerging tax planning opportunities, and protect your legacy for loved ones.

Summary of Key Points

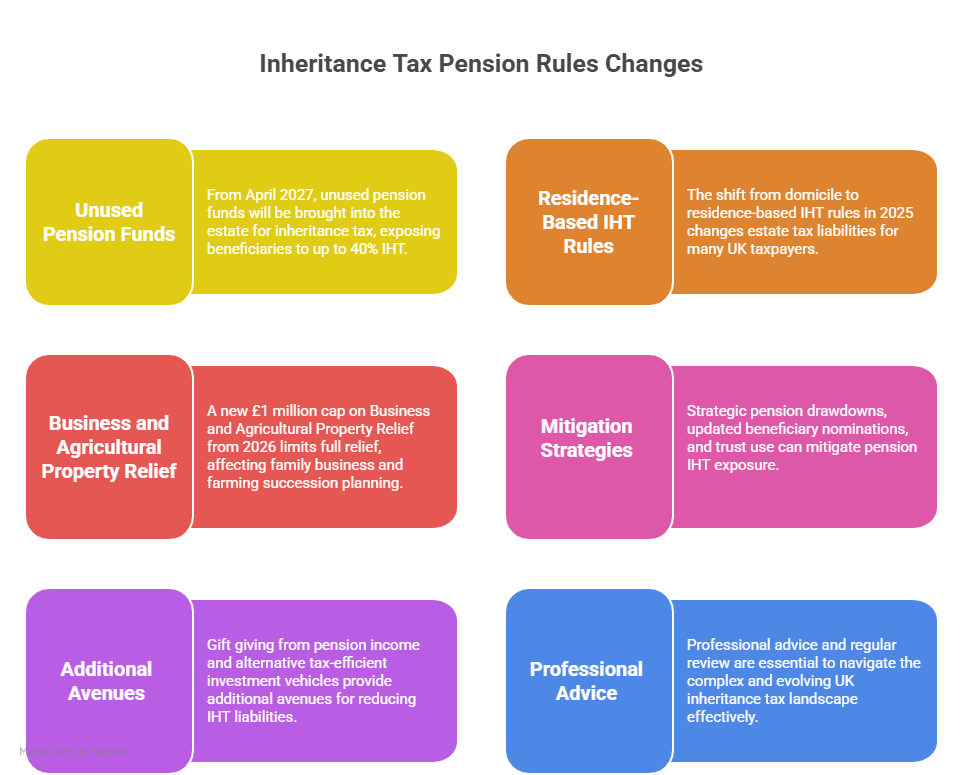

- From April 2027, unused pension funds will be brought into the estate for inheritance tax, exposing beneficiaries to up to 40% IHT.

- The shift from domicile to residence-based IHT rules in 2025 changes estate tax liabilities for many UK taxpayers.

- A new £1 million cap on Business and Agricultural Property Relief from 2026 limits full relief, affecting family business and farming succession planning.

- Strategic pension drawdowns, updated beneficiary nominations, and trust use can mitigate pension IHT exposure.

- Gift giving from pension income and alternative tax-efficient investment vehicles provide additional avenues for reducing IHT liabilities.

- Professional advice and regular review are essential to navigate the complex and evolving UK inheritance tax landscape effectively.

Readers are encouraged to consult HMRC’s official resources (gov.uk) and seek bespoke advice tailored to their circumstances to ensure compliance and optimal planning outcomes. This approach not only minimises tax liabilities but also safeguards the financial futures of beneficiaries

FAQs

Q1: What happens to unused pension funds in the UK under the new inheritance tax rules after April 2027?

A1: Well, it’s worth noting that from April 2027, unused pension funds will be counted as part of your estate for inheritance tax purposes. This means that if your estate exceeds the inheritance tax threshold, your pension pot — previously exempt — could now trigger a 40% tax charge. I’ve seen clients who hadn’t touched their pensions during retirement suddenly face unexpected bills after passing. Careful planning or withdrawing funds strategically before death can reduce this exposure.

Q2: Can pension death benefits still be tax-free if left to a spouse or civil partner?

A2: Yes, pensions left to a spouse or civil partner remain free from inheritance tax, just as before. This exemption is crucial and can save families significant sums. However, if left to other beneficiaries like children or friends, the new rules mean pensions will be included in the estate and liable for IHT, so nominations need regular review.

Q3: How do the new inheritance tax rules affect beneficiaries over 75 inheriting pensions?

A3: Inheriting a pension after the original holder’s 75th birthday can be a tax minefield. Now with pensions in the estate, beneficiaries may face both a 40% inheritance tax and income tax on withdrawals. That combined hit could approach 67%, which is why advanced planning like using trusts or drawdown can make a big difference.

Q4: Are death-in-service benefits affected by the April 2027 inheritance tax changes?

A4: No, death-in-service benefits remain outside the scope of inheritance tax, which is a relief for many families. This exemption means that lump sums paid upon death from an employer’s death-in-service scheme are not included in the estate for IHT calculations.

Q5: How can self-employed individuals adjust their pension and estate planning to cope with these changes?

A5: For the self-employed, the key is flexibility. Many use SIPPs, so reviewing pension drawdowns to reduce fund values before death is wise. Plus, making lifetime gifts or setting up trusts can help. I recall a freelance consultant in Manchester who reduced potential IHT by systematically drawing down part of her pension over a few years.

Q6: What impact do the changes have on business owners who use pensions as part of their succession or inheritance plans?

A6: Business owners often see pensions as a tax-efficient inheritance tool. With these changes, that advantage diminishes, so they should reconsider their plans. Exploring alternatives like business property relief on other assets or rearranging pension beneficiary designations is vital to avoid big tax bills on retirement pots.

Q7: Is there any relief for estates below the inheritance tax threshold when pensions are included?

A7: Yes, estates valued under the nil-rate band—currently £325,000—will still pay no inheritance tax, even with pensions included. Also, the residence nil-rate band may add further relief if you’re leaving a home to direct descendants. So smaller estates usually won’t be affected drastically.

Q8: How does UK residency status influence inheritance tax on pensions after the April 2025 residency rule change?

A8: Residency is now key. If you’ve been UK resident for at least 10 of the last 20 years, your worldwide assets—including pensions—are subject to UK IHT. This can surprise those who were previously relying on domicile rules. Non-residents typically only pay IHT on UK assets.

Q9: What happens if multiple pension schemes are involved in the estate? How is IHT calculated?

A9: All unused pension pots are aggregated into the estate. The total adds to your other assets to determine if IHT applies. Executors should coordinate with pension providers to declare total pension value and arrange payment or deduction of IHT, which can be a complex task if multiple schemes are involved.

Q10: Can someone with more than one job affect their pension inheritance tax situation?

A10: Holding multiple jobs often means multiple pension schemes, increasing the unused pension value in an estate. Each will count towards IHT, so juggling several pots means more careful planning. Checking beneficiary nominations on every scheme is crucial to avoid unnecessary tax.

Disclaimer

The information provided in this article is for general guidance only and is not intended to constitute professional advice, tax advice, financial advice, legal advice, or any other form of regulated guidance. Although every effort has been made to ensure accuracy at the time of publication, Fair View Accounting Services, including its director, employees, contractors, writers, and content-creation team, accepts no responsibility for any loss, damage, penalty, or consequence arising from reliance on the information contained herein.

UK tax legislation changes frequently, and HMRC interpretations, thresholds, and rules may vary depending on the individual circumstances of each taxpayer. Nothing in this article should be considered a substitute for obtaining formal, personalised advice from a qualified accountant or tax professional. Readers should not take action—or refrain from taking action—based solely on the content published on this website.

Fair View Accounting Services does not guarantee the completeness, accuracy, or ongoing validity of the information provided and assumes no liability for omissions or errors, whether typographical, factual, or technical. By using this content, the reader acknowledges that all responsibility for decisions remains solely with the user.