Operating Mixed CIS And PAYE Workforces

Operating a Mixed CIS and PAYE Workforce in the UK (2026 Context)

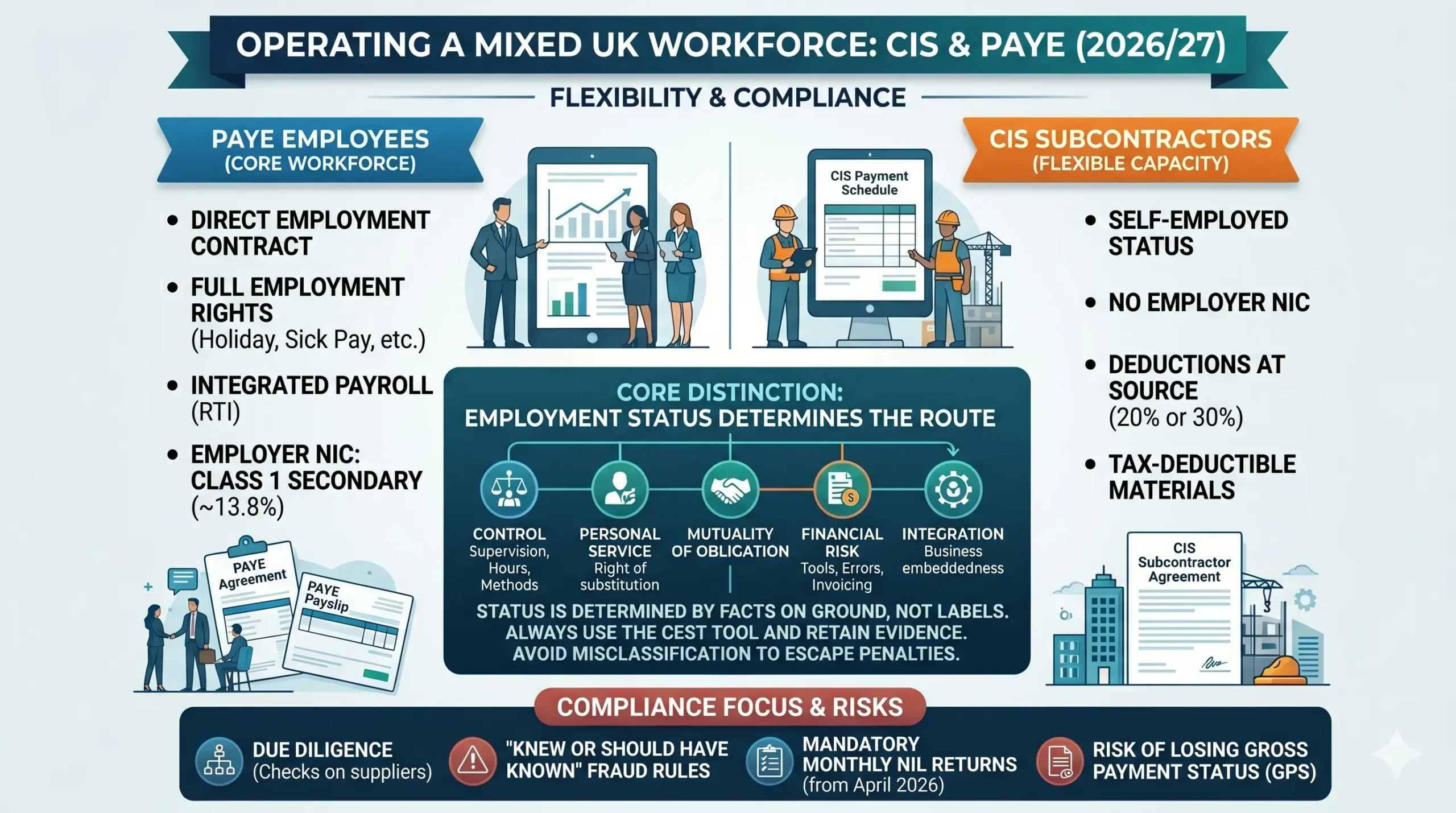

Many UK construction businesses, developers, and trades operate a hybrid workforce: core employees paid through PAYE alongside self-employed subcontractors under the Construction Industry Scheme (CIS). This model offers flexibility—stable staffing for ongoing operations and scalable specialist or peak-period capacity—while carrying distinct compliance demands, cost implications, and risks.

Why Businesses Use Mixed Workforces

A mixed approach allows contractors to maintain direct control and employment rights obligations over key personnel (e.g., site managers, apprentices, or long-term tradespeople) while engaging external specialists (e.g., electricians, scaffolders, or groundworkers) on a project or as-needed basis without the full overhead of employment.

PAYE employees bring:

- Employer National Insurance Contributions (Class 1 secondary NIC) at 13.8% above the secondary threshold.

- Entitlements to holiday pay, sick pay, maternity/paternity pay, and employment protections.

- Full integration into payroll with Real Time Information (RTI) reporting.

CIS subcontractors typically involve:

- No employer NIC for the engager (the subcontractor handles their own Class 2/4 NIC via Self Assessment).

- Deductions at source: 20% for registered subcontractors or 30% for unregistered (applied to the labour element only, after verifiable materials).

- Greater flexibility to scale without ongoing commitments.

The model works well when status is clear and correctly applied, but missteps in classification or administration can trigger HMRC enquiries, penalties, and unexpected liabilities.

Core Distinction: Employment Status Determines the Route

The fundamental rule, unchanged in 2026, is that CIS applies only where there is no contract of employment. If a worker is an employee under common law principles, they must be on PAYE. You cannot route an employee through CIS.

Key factors HMRC and tribunals examine include:

- Control: Degree of supervision, hours, methods of work.

- Personal service: Right of substitution.

- Mutuality of obligation: Ongoing expectation of work and payment.

- Financial risk: Who bears the cost of mistakes, provides tools/equipment, and handles invoicing.

- Integration: How embedded the worker is in the business.

HMRC’s Check Employment Status for Tax (CEST) tool provides a useful (though not infallible) indication. Run it for each new engagement or material change in working practices, and retain the output and supporting evidence. Status is engagement-specific; a worker can be an employee for one contract and a subcontractor for another with a different party or under different terms.

Common pitfall: Assuming past self-employed treatment or a subcontractor’s own registration automatically justifies CIS. HMRC looks at the actual relationship, not labels or history. Recharacterisation can lead to unpaid employer NIC, penalties, and interest for the engager.

Mixed CIS & PAYE Workforces

The 2026/27 UK Compliance Landscape

Navigating the Hybrid Model

In 2026, the construction industry relies on a strategic blend of core employees and specialist subcontractors. While this offers unparalleled scalability, HMRC has significantly sharpened its focus on classification accuracy. Operating a mixed workforce is no longer just about payroll; it is a critical exercise in supply-chain due diligence and financial risk management.

The Status Gateway

Employment status is the legal foundation. HMRC uses five core "common law" tests to determine if a worker should be on PAYE. If these indicators are high, the Construction Industry Scheme (CIS) cannot be legally applied.

Cost & Overhead Comparison

A worker earning £4,000 gross per month costs the employer significantly more under PAYE due to Class 1 Secondary National Insurance (NIC) and statutory benefits.

*Estimates based on projected 2026/27 thresholds and 13.8% Secondary NIC rates.

2026 Compliance Roadmap

Classification Risk Distribution

Mapping the relationship between worker integration and the likelihood of an HMRC enquiry. High integration combined with high duration triggers a "Red Zone" risk.

📝 Verification Rates

🚩 Red Flag Audit

- ● Long-term (>12 months) exclusive service.

- ● Provision of tools, uniforms, or transport.

- ● Fixed hourly rates instead of per-project quotes.

The hidden overhead for every PAYE employee.

Failure to file nil returns leads to escalating fines.

Mandatory evidence for every engagement review.

Practical Operation: Running Both Systems Side-by-Side

Businesses with mixed workforces typically maintain:

- A PAYE scheme for employees (RTI FPS/EPS submissions, P60s, etc.).

- Separate CIS contractor registration for subcontractor payments.

You can (and often should) register for both through the same HMRC online account when setting up as a new employer/contractor.

Key operational points:

- Verification: Before first payment to a subcontractor, verify their CIS status via HMRC (online or phone). Record the response.

- Deductions: Calculate on the labour portion only. Materials must be genuinely incurred and evidenced (invoices in the subcontractor’s name). Mixed contracts (construction + non-construction elements under one agreement) usually bring the entire payment into CIS.

- Monthly CIS returns: From 6 April 2026, mainstream contractors must file a return every month, even nil returns (or notify inactivity in advance). Late filing attracts penalties (£100 fixed, escalating).

- Payment to HMRC: CIS deductions are due monthly or quarterly alongside PAYE liabilities.

- Statements: Provide deduction statements (CIS25 or equivalent) to subcontractors.

For limited company subcontractors receiving CIS deductions, they can offset these against their own PAYE/NIC liabilities via the Employer Payment Summary (EPS), improving cash flow.

2026 Updates and Heightened Compliance Focus

Recent reforms tighten the regime:

- Anti-fraud measures: From April 2026, HMRC can act where a business “knew or should have known” of fraudulent activity in the supply chain (aligned with VAT Kittel principles). This can include immediate loss of Gross Payment Status (GPS) for up to five years, assessments, and personal liability for officers.

- Nil returns reinstated: Mandatory filing discipline returns.

- Exemptions: Payments to certain public bodies/local authorities are exempt.

- Gross Payment Status: Stricter compliance tests (including VAT) continue; GPS allows subcontractors to receive payments gross but demands strong record-keeping and timely filings.

These changes increase supply-chain due diligence expectations. Contractors should review subcontractor onboarding, monitor for red flags (e.g., unusually low rates, rapid turnover), and document verification steps.

Cost and Cash Flow Comparisons

Consider a simplified monthly example (2026/27 rates; thresholds subject to annual updates):

- PAYE worker earning £4,000 gross/month: Employer pays ~£4,000 + ~£350–£400 secondary NIC (depending on exact thresholds), plus holiday/sick provision. Deducts employee tax/NIC and reports via RTI.

- CIS subcontractor invoicing £4,000 + £800 materials = £4,800 total: Deduct 20% on £4,000 labour (£800), pay net £4,000. No employer NIC. Subcontractor claims materials and pays tax/NIC via Self Assessment (with credit for CIS deduction).

The CIS route often appears cheaper short-term but shifts administrative burden and tax risk. Over-reliance on CIS for workers who function like employees can prove expensive if reclassified.

Record-Keeping and Risk Management

Maintain clear separation:

- Distinct contracts: employment contracts vs. subcontractor agreements.

- Timesheets, site records, and payment trails that reflect the relationship.

- Regular status reviews (e.g., annually or on contract renewal).

- Robust invoicing: Labour and materials clearly separated.

Red flags for HMRC:

- Subcontractors working exclusively or predominantly for one engager over long periods.

- Provision of tools, uniforms, or supervised hours by the engager.

- “Employee-like” integration without employment rights.

- Invoice splitting to avoid CIS on mixed elements.

Tribunal cases often turn on the full factual picture rather than contract wording alone.

🏗️ Operating a Mixed CIS & PAYE Workforce (2026/27)

Strategic compliance, cost optimisation, and risk management for UK construction businesses navigating hybrid staffing models under the latest HMRC rules.

Core Staffing & Control

- Employer NIC at 13.8% above secondary threshold (~£9,100/yr in 2026/27)

- Full RTI reporting, auto-enrolment pensions, statutory leave/sick pay

- Ideal for site managers, long-term trades, apprentices

Scalable & Flexible

- No employer NIC; subcontractor handles Class 2/4 via SA

- Deductions at source: 20% (registered) or 30% (unregistered) on labour only

- Ideal for specialists, peak workloads, project-based roles

🔑 Status Determination Rules

Golden Rule: If it walks, talks, and works like an employee, it must be PAYE. CIS only applies to genuine self-employment.

HMRC evaluates actual working practices, not contract titles. Key tests:

Personal Service – Can they send a substitute?

Mutuality of Obligation – Must you offer work? Must they accept?

Integration – Embedded in your team or operating independently?

Tip: Use HMRC’s CEST tool per engagement and save the results.

💷 Monthly Cost Comparison (2026/27 Estimates)

Gross: £4,000

Employer NIC (~13.8% above threshold): ~£442

Admin/Leave/Sick buffer: ~£250

Est. Total: £4,692

Labour Element: £3,200

CIS Deduction (20/30%): £640

Materials (passed through): £800

Net Pay to Sub: £3,360

Employer NIC: £0

*2026/27 estimates only. Actual NIC, tax, and statutory costs vary by individual circumstances, Scottish/Welsh tax codes, and exact threshold uplifts. Always verify with a qualified accountant.

🚨 2026/27 HMRC Compliance Focus

From April 2026, HMRC applies VAT-style Kittel principles to CIS. If your business knew or should have known a subcontractor was involved in supply-chain fraud, penalties include immediate loss of Gross Payment Status (GPS) for up to 5 years, assessments, and potential personal liability for directors. Maintain robust onboarding checks.

The discipline of monthly CIS returns is reinstated. Even with zero payments to subcontractors, you must file a nil return or formally notify inactivity in advance. Late filing triggers escalating penalties starting at £100.

GPS applicants face tougher compliance tests, now explicitly cross-referenced with VAT filing history. Consistent late submissions or VAT discrepancies can trigger automatic GPS reviews or revocations.

CIS handles payment-stage deductions. IR35 (off-payroll) assesses the underlying employment status. A subcontractor can be CIS-verified but still fall inside IR35. Run parallel status tests for high-value or embedded limited company contractors.

📖 Frequently Asked Questions

🛡️ Implementation & Defence Checklist

Click items to track your compliance progress. Data resets on page refresh.

- Run CEST for every new/changed engagement & save output

- Verify CIS status before first payment (HMRC online/phone)

- Separate PAYE scheme & CIS contractor registration

- Ensure payroll software handles RTI + CIS25 statements

- Implement subcontractor due diligence checklist

- File monthly CIS returns (including nil returns)

- Review status annually or on contract renewal

- Keep timesheets, tool provision records, and payment trails separate

Next Steps and When to Seek Advice

For most businesses, a mixed workforce is viable and common, provided status determinations are robust and processes are disciplined. Review existing arrangements against current working practices, especially with 2026’s compliance uplift.

Practical actions:

- Run CEST for borderline workers and document decisions.

- Ensure payroll/CIS software or provider handles both regimes accurately.

- Implement supply-chain due diligence checklists.

- Engage an accountant or payroll specialist familiar with construction for complex or high-turnover operations.

- Monitor GOV.UK and HMRC CIS340 guidance for updates.

Operating mixed CIS and PAYE teams successfully requires clarity on employment status, disciplined monthly compliance, and awareness of evolving HMRC priorities around fraud and misclassification. Get the foundations right, and the model delivers genuine operational flexibility without disproportionate risk.

Key Takeaways

- Employment status is the gateway: wrong classification exposes you to PAYE liabilities plus penalties.

- Separate systems but integrated compliance: PAYE for employees, CIS for genuine subcontractors.

- 2026 brings stricter filing and anti-fraud rules—nil returns and supply-chain vigilance matter.

- Documentation and regular reviews are your best defence in any HMRC review.

- Cash flow and cost advantages exist but must be weighed against administration, risk, and worker entitlements.

FAQs

Q1: Can a worker switch between CIS subcontractor and PAYE employee status with the same business depending on the project?

A1: Yes, it’s possible, but only if the actual working relationship genuinely changes each time. In my experience with clients in the Midlands, a site manager might be employed on PAYE for a long-term development role involving daily oversight and fixed hours, then engaged as a specialist subcontractor under CIS for a one-off design phase where they invoice for labour and materials with their own insurance. The key is documenting the different terms clearly and running a fresh employment status check. HMRC will look at the reality on the ground, not the paperwork alone. Mixing the two without a real distinction risks reclassification and backdated employer National Insurance.

Q2: What should a construction business do if a long-term CIS subcontractor starts behaving more like an employee?

A2: This is one of the most common issues I see. If the subcontractor works exclusively for you, uses your tools, follows your daily instructions, and has no real financial risk, you should review the status immediately. In practice, I’ve advised clients to transition them onto PAYE before HMRC does it for you. The cost of employer NIC and entitlements is often lower than a surprise assessment plus penalties years later. Keep records of when and why the relationship shifted.

Q3: How do Scottish income tax rates affect someone operating as a CIS subcontractor versus a PAYE employee?

A3: Scottish taxpayers face different income tax bands and rates from the rest of the UK, which can make a noticeable difference depending on total income. For PAYE employees, the employer applies the correct Scottish tax code via RTI, so deductions are usually spot on. CIS subcontractors receive a flat 20% or 30% deduction regardless of where they live, then sort out the Scottish rates through Self Assessment. I’ve had clients in Glasgow who ended up with a small underpayment because they didn’t factor in the higher Scottish bands on their trading profits. Always declare CIS income accurately and consider quarterly payments on account if your profits are rising.

Q4: Does operating a mixed workforce create any issues when claiming the Employment Allowance?

A4: The Employment Allowance can still be claimed against your PAYE Class 1 secondary National Insurance liabilities, but it won’t apply to CIS payments. If your business is close to the £100,000 PAYE threshold or you have connected companies, watch for eligibility rules. One client with a mix of site staff and specialist subcontractors saved several thousand pounds by carefully allocating the allowance to their employee payroll only. Check your eligibility each year as the rules tighten.

Q5: What happens if a subcontractor with Gross Payment Status supplies both labour and materials in one invoice?

A5: You only deduct CIS tax on the labour element, provided the materials are properly evidenced. This is where many businesses trip up. I remember a roofing contractor client who paid gross on the whole invoice for several months until an HMRC review. The materials invoices were in the subcontractor’s name, but the amounts weren’t clearly separated. Keep detailed breakdowns and supporting invoices to avoid having to repay deductions plus interest.

Q6: Can directors of a limited company that is CIS-registered also be on PAYE for their own company?

A6: Absolutely. Many construction company directors take a modest salary through PAYE for tax and National Insurance purposes while the company operates as a CIS contractor for its subcontractors. This is perfectly normal. The important point is keeping the director’s employment separate from any subcontractor work they might do personally. I’ve seen confusion arise when directors also trade as sole traders on the side – make sure the two capacities don’t blur.

Q7: How does the apprenticeship levy interact with a mixed CIS and PAYE workforce?

A7: The levy is calculated only on your PAYE payroll bill above the £3 million threshold (or the relevant lower threshold for connected companies). CIS payments to genuine subcontractors don’t count towards the levy. This can make a mixed model attractive for larger firms looking to manage levy exposure. One building firm I work with keeps core permanent staff under PAYE and uses CIS for variable trades to keep their levy bill under control while still claiming levy-funded training where possible.

Q8: What are the risks of using the same person as both a CIS subcontractor and an agency worker through different routes?

A8: This arrangement often raises red flags. If the substance of the relationship is employment, HMRC or an employment tribunal could look through the structures. I’ve advised clients to avoid dual arrangements with the same individual unless the roles are genuinely distinct and separately contracted. The cash-flow benefit can be tempting, but the compliance risk and potential employment rights claims make it something to approach very carefully.

Q9: Does remote or office-based work in a construction support role change whether CIS or PAYE applies?

A9: CIS only covers construction operations, so purely administrative, design, or consulting work outside site activities usually falls under normal PAYE or Self Assessment rules rather than CIS. A quantity surveyor working remotely for multiple contractors might not trigger CIS at all. Clients sometimes assume everything in the sector is CIS – that’s a common and expensive misunderstanding.

Q10: What should a subcontractor do if they suspect their contractor has applied the wrong CIS deduction rate?

A10: First, check your verification status with HMRC and ask the contractor for their records. If a 30% deduction was applied when you’re registered for net payment, you can usually recover the difference through your Self Assessment or by contacting HMRC. In my practice, prompt action has saved clients hundreds or even thousands. Keep your own records of every payment and deduction statement.

Q11: How do pension contributions work differently for PAYE employees versus CIS subcontractors in a mixed team?

A11: PAYE employees can benefit from auto-enrolment and employer contributions that reduce the employer’s NIC bill. CIS subcontractors arrange their own pensions, usually as self-employed relief on contributions. This is an area where businesses can differentiate their offering to attract good permanent staff while using subcontractors for flexibility. Consider salary sacrifice arrangements for employees that aren’t available to subcontractors.

Disclaimer

The information provided in this article is for general guidance only and is not intended to constitute professional advice, tax advice, financial advice, legal advice, or any other form of regulated guidance. Although every effort has been made to ensure accuracy at the time of publication, Fair View Accounting Services, including its director, employees, contractors, writers, and content-creation team, accepts no responsibility for any loss, damage, penalty, or consequence arising from reliance on the information contained herein.

UK tax legislation changes frequently, and HMRC interpretations, thresholds, and rules may vary depending on the individual circumstances of each taxpayer. Nothing in this article should be considered a substitute for obtaining formal, personalised advice from a qualified accountant or tax professional. Readers should not take action—or refrain from taking action—based solely on the content published on this website.

Fair View Accounting Services does not guarantee the completeness, accuracy, or ongoing validity of the information provided and assumes no liability for omissions or errors, whether typographical, factual, or technical. By using this content, the reader acknowledges that all responsibility for decisions remains solely with the user.