How Does HMRC Collect Tax On Savings Interest

Understanding the Core Rules: How HMRC Actually Collects Tax on Your Savings Interest in 2026/27

You know the feeling. You open your banking app, see a healthy lump of interest sitting in your easy-access saver, and for about three seconds it feels like a win. Then a small voice in the back of your head reminds you HMRC will probably want a slice — and that little voice has been getting louder every year since interest rates climbed.

The good news is that the heavy lifting has been done for you since April 2016, when banks and building societies stopped deducting tax at source. Before then, 20% was lopped off automatically, which was painful for non-taxpayers but at least meant most people didn’t have to think about it. Now interest is paid gross, which is brilliant for cashflow but does shift the responsibility onto HMRC to chase any tax owed — and onto you to make sure their numbers are right.

Here’s how the collection machinery actually works in 2026/27:

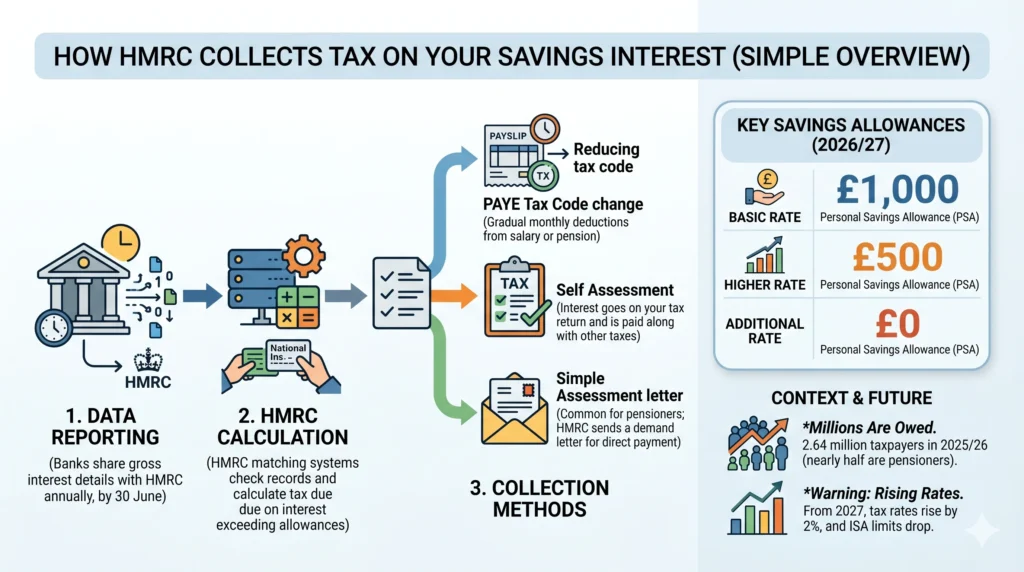

Every year, usually by 30 June after the tax year ends, every UK bank, building society, NS&I and most other financial institutions have to send HMRC a full data return showing the interest they’ve paid or credited to each customer. HMRC then runs that data through its matching system, lining it up against National Insurance numbers and address records to work out who owes what. Where your total taxable interest pushes past your allowances, HMRC works out the tax due and gets the money back from you in one of three ways.

If you’re employed or drawing a private or company pension, HMRC will almost always tweak your tax code — sometimes mid-year, more often at the start of the next tax year — so the underpayment is collected gradually from your salary or pension. In my experience, this catches the vast majority of cases.

If you’re already in Self Assessment, the interest just goes onto your tax return and gets paid alongside your usual balancing payment (or rolled into payments on account if you’re a sole trader).

If you’re outside PAYE altogether — perhaps you only receive the State Pension, or you’ve retired with no other taxable income — HMRC will instead pop a Simple Assessment letter through your door (the calculation is the PA302). That tells you exactly what you owe and when to pay it.

Recent figures from a Freedom of Information request by AJ Bell, published in autumn 2025, show that around 2.64 million UK taxpayers were expected to owe tax on their savings interest in 2025/26 — more than four times the number from just four years earlier. With thresholds frozen and rates having stayed elevated through 2024 and 2025, that number is almost certainly going to climb again for 2026/27. Pensioners alone account for nearly half of those caught.

The Key 2026/27 Allowances That Shield Most People

Allowance | Who Gets It | Amount Tax-Free on Interest | Key Notes |

Personal Allowance | Everyone (tapers away above £100,000) | Up to £12,570 of total income (including interest) | Frozen until April 2031. Lost entirely once income hits £125,140 |

Starting Rate for Savings | Only if your other (non-savings) income is below £17,570 | Up to £5,000 at 0% | Reduces £1 for £1 once non-savings income exceeds £12,570 |

Personal Savings Allowance (PSA) | Basic-rate taxpayer (income up to £50,270) | £1,000 | Higher-rate (£50,271–£125,140): £500. Additional-rate: £0 |

Cash ISA | Anyone over 18 | Unlimited (within £20,000 annual subscription) | Completely tax-free — interest doesn’t count towards anything |

A quick reality check on how much you need stashed away before the PSA gives up the ghost:

Tax Status | PSA | Savings needed at 4.5% | Savings needed at 5.0% |

Basic-rate | £1,000 | Around £22,200 | Around £20,000 |

Higher-rate | £500 | Around £11,100 | Around £10,000 |

Additional-rate | £0 | Any interest is taxable | Any interest is taxable |

You’ll notice those numbers are a lot lower than people instinctively assume. Plenty of clients arrive in my office convinced they’re “miles off” the threshold, only to find their £15,000 emergency fund is already nudging them over it.

A Real-World Example I See Most Weeks

Take Mark from Birmingham — a client of mine who came in last spring. Mark earns £42,000 on PAYE, married with two children, and over the past few years he’d built up around £100,000 in a high-street easy-access saver paying about 4.6%. That gave him roughly £4,600 of interest in 2025/26.

His tax position works out like this:

- His salary uses up his £12,570 Personal Allowance and a chunk of the basic-rate band, but leaves him comfortably under £50,270 — so he’s a basic-rate taxpayer.

- Starting Rate for Savings: zero, because his salary is well above £17,570.

- PSA: £1,000.

- Taxable interest: £4,600 minus the £1,000 PSA = £3,600. Tax due at 20% = £720.

His three banks reported the figures to HMRC by the end of June 2025. By around October he received a P800 setting out the underpayment, and HMRC adjusted his 2026/27 tax code accordingly so the £720 came out gradually over the year — about £60 a month off his take-home. He didn’t notice for weeks; when he did, he rang me in mild panic. We logged into his Personal Tax Account, confirmed everything was right, and he chose to leave it collecting through PAYE rather than write a cheque.

The lesson, as ever: log in and look. Don’t wait to be ambushed by a payslip that’s £60 lighter than you expected.

Scottish and Welsh Taxpayers — The Bit Most People Get Wrong

This one trips up half my Scottish clients on first appointment. If you live in Scotland or Wales, you pay Scottish or Welsh rates on earned income and pensions — but savings interest is always taxed at the rest-of-UK rates and bands. Always. Doesn’t matter whether you’re paying 21% Scottish intermediate rate on your salary; for your interest, you’re back to the standard 20%/40%/45% structure for 2026/27, with the PSA tied to UK thresholds.

I had a Glasgow couple last summer convinced they owed thousands more than they actually did because they’d assumed their Scottish higher rate applied to their interest as well. Pleasant phone call, that one.

A Word on What’s Coming Down the Track

Worth flagging this before we move on, because it isn’t yet in most clients’ heads. The Autumn Budget 2025 announced two big changes that affect savers, neither of which kicks in this year but both of which will hurt next year:

- From 6 April 2027, the rates of tax on savings interest go up by 2 percentage points across the board. So basic-rate becomes 22%, higher-rate 42% and additional-rate 47%. The PSA and starting rate band are unchanged.

- From 6 April 2027, the Cash ISA subscription limit drops from £20,000 to £12,000 a year for under-65s. The over-65s keep the full £20,000. The overall £20,000 ISA wrapper still applies — the rest just has to go into Stocks & Shares, Innovative Finance or a Lifetime ISA.

So 2026/27 is, for under-65s, the last chance to use the full £20,000 cash allowance. I’d be filling that ISA before April if you’ve got the cash sitting in a taxable account.

The HMRC Savings Tax Trap

Understanding the core rules and realities of how HMRC collects tax on your savings interest in the 2026/27 tax year.

Taxpayers Expected to Owe Savings Tax (2025/26)

With frozen thresholds and elevated interest rates, over two and a half million taxpayers—four times the number from just four years prior—are being caught in the tax net. Pensioners account for nearly half.

Your Defences: The Personal Savings Allowance

The Personal Savings Allowance (PSA) determines how much interest you can earn tax-free. As your total income pushes you into higher tax brackets, your PSA drops sharply, disappearing completely for additional-rate taxpayers.

The Danger Zone: Savings Needed to Hit the Limit

Many assume they need massive wealth to be taxed on interest. With high-street rates hovering around 4.5% to 5.0%, a modest emergency fund of £10,000 to £22,000 is enough to breach the allowance.

How the Collection Machinery Actually Works

Interest is now paid gross. By June 30th each year, financial institutions send a full data return to HMRC. HMRC's matching system then calculates what you owe and retrieves it via one of three methods.

PAYE Tax Code Tweaks

For employed or pension-drawing individuals, HMRC tweaks the tax code. The underpayment is collected gradually from your salary or pension throughout the year.

Self Assessment

If already registered (e.g., sole traders), interest is added to your tax return and paid alongside your usual balancing payment or payments on account.

Simple Assessment

If completely outside PAYE (e.g., State Pension only), HMRC posts a PA302 letter detailing the exact calculation and when to pay the bill directly.

HMRC's Matching System Errors

You cannot blindly trust HMRC's figures. According to FOI data, HMRC's automated engine fails to properly reconcile bank account interest against taxpayer records in a staggering portion of cases. Joint accounts are the worst offenders.

Interest Earned vs. PSA Limits

Visualizing the exact point at which your savings cross into taxable territory. The chart below models interest accrued against total savings balances at the two most common market rates.

⚠ Warning: The 2027 Tax Hike

The Autumn Budget announced sweeping changes taking effect from April 6, 2027, making 2026/27 the final window for current allowances.

Tax Rates Jump by 2%

Basic-rate rises to 22%, higher-rate to 42%, and additional-rate to 47%. The underlying allowances remain completely frozen.

Cash ISA Limits Slashed

The generous £20,000 Cash ISA limit will drop to just £12,000 a year for under-65s. 2026/27 is the last chance to maximize this tax-free wrapper.

Checking What HMRC Already Knows, Catching Their Mistakes, and Running Your Own Calculations

Where most people come unstuck isn’t the sums — it’s assuming HMRC’s figures are right. They quite often aren’t. Banks send their interest returns to HMRC by 30 June each year for the previous tax year, and the matching process usually rolls out P800s between July and November. For 2023/24 the volume was so heavy that the process didn’t finish until March 2025, and 2024/25 was much the same story. So if you haven’t heard anything yet about a year that ended a while back, don’t assume you’re in the clear.

Here’s the bit that should give you pause: according to AJ Bell’s FOI data, HMRC says it cannot reconcile bank account interest against taxpayer records in roughly one in five cases. That’s not a typo. Twenty per cent. Joint accounts are the worst offenders, along with offshore interest, accounts opened years ago at addresses you’ve since moved from, and anywhere the bank’s records of your name don’t match HMRC’s exactly. Sometimes you’ll dodge a tax bill because of it; sometimes HMRC will catch up with you years later, sometimes with a penalty for failure to notify on top.

How to See What HMRC Has on You — In Five Minutes

Don’t wait for a brown envelope. This is genuinely a five-minute job and I’d strongly suggest doing it tonight.

Sign in to your Personal Tax Account at gov.uk/personal-tax-account. From the dashboard, click “Check your Income Tax for the current year”, then “View PAYE income and tax details”. Scroll down until you find a line called “Untaxed interest” or “Estimated untaxed interest” — that’s the figure HMRC is currently using to set your tax code for 2026/27. For previous tax years, click “Tax years” and choose the year you want; any P800 will sit under “Tax calculations”.

If the figure looks off — too high, too low, or includes an account you closed years ago — the Income Tax helpline on 0300 200 3300 can break it down by individual bank. The online summary just gives a single number, but the back-end records are itemised by bank and account. Have your NI number ready.

A Client Story That Still Annoys Me

David and Susan, a retired couple from Leeds, came to me in early 2025. Between them they had £180,000 in a Santander joint easy-access saver paying 4.7%, which produced £8,460 of interest over the year. By default that should have been split 50:50 by HMRC under the spousal rules in ITA 2007 s.836 — £4,230 each.

David, who has a couple of decent private pensions on top of his state pension, is a higher-rate taxpayer, so his PSA is £500. The P800 he received in October showed the £4,230 less his £500 PSA, taxed at 40% — about £1,492. Fair enough.

Susan’s P800, however, never arrived. The reason was that Santander had reported the entire £8,460 against David’s NI number alone, because his name was first on the account. It’s a common glitch on older joint accounts opened before banks tightened up their KYC processes. Susan assumed she was fine. She wasn’t. In March 2026 HMRC suddenly amended her state pension tax code and started clawing back tax, plus late-payment interest at 8.5% (Bank rate plus 4%, since the rate was hiked in April 2025). She rang me in tears.

We sorted it with one phone call, both NI numbers in front of us, and got the late-payment interest waived — but only because we caught it within a few months. Had it run longer, that battle would have been considerably harder.

The takeaway: if you and your spouse hold any joint account, both of you should log into your Personal Tax Accounts and compare what’s there. And if your beneficial ownership genuinely isn’t 50:50, look at filing a Form 17 within 60 days of any change — that’s the only way HMRC will accept a different split for spouses or civil partners.

Your 2026/27 Savings Interest Worksheet

I’ve used a version of this with clients for years. Drop it into a spreadsheet, fill in the cells in column D, and it’ll catch most of the errors HMRC makes.

Row | Description | Your Figure £ | Notes / Formula |

1 | Total gross savings interest received in 2025/26 (every account) | Include NS&I, peer-to-peer, gilts coupons | |

2 | Less interest from Cash ISAs and other tax-free sources | Always £0 tax | |

3 | Taxable gross interest (Row 1 − Row 2) | ||

4 | Non-savings, non-dividend income (salary, pensions, rental profit) | ||

5 | Personal Allowance used by Row 4 | =MIN(12570, D4) | |

6 | Remaining Personal Allowance for savings | =12570 − D5 | |

7 | Starting Rate for Savings available (max £5,000) | =MIN(5000, MAX(0, 17570 − D4)) | |

8 | Total 0% allowance available for savings (Row 6 + Row 7) | ||

9 | Interest taxed at 0% (PA + starting rate) | =MIN(D3, D8) | |

10 | Interest remaining after 0% bands | =D3 − D9 | |

11 | Personal Savings Allowance | =IF(D4+D3<=50270,1000,IF(D4+D3<=125140,500,0)) | |

12 | Interest covered by PSA | =MIN(D10, D11) | |

13 | Fully taxable interest | =D10 − D12 | |

14 | Tax due — work out using bands below |

Quick reckoner for Row 14 in 2026/27 (England, Wales and Northern Ireland — these rates apply to Scottish and Welsh residents on savings income too):

- First £37,700 of taxable income above the Personal Allowance: 20%

- Next £74,870 (so up to £125,140 total): 40%

- Anything above £125,140: 45%

Two quick warnings for the keen-eyed: from April 2027 those 20%/40%/45% rates rise to 22%/42%/47%, so this worksheet will need updating then. And from April 2027 HMRC is also changing how it allocates the Personal Allowance between different income types — earned income will be served first — which will increase the tax on savings, dividends and rental income for some people with mixed income sources. None of that bites yet, but it’s coming.

Multiple Jobs, Company Pensions and Emergency Codes — The Quiet Disasters

This one bites every January. If you changed jobs mid-year, ran on a BR or 0T emergency code for a few months, or you’ve got a salary plus a small pension, HMRC’s coding system can badly underestimate which tax band your savings interest falls into. I had a client in Croydon last year on a BR code for five months who ended up with a £2,300 P800 because the system had assumed all his interest was basic-rate when in fact most of it was higher-rate.

The fix is unglamorous but works. Phone HMRC before 5 April with a sensible estimate of your final income for the year. They’ll adjust your code in-year, and any underpayment gets spread smoothly rather than dumped on you in one go.

How HMRC collects tax on your savings interest.

Banks pay your interest gross. HMRC chases the tax. With frozen thresholds, elevated rates and an Autumn Budget 2025 hike on its way, the number of UK savers caught by tax has more than quadrupled in four years. Here's exactly how the machinery works — and how to stay ahead of it.

The four allowances that shield your interest.

Personal Allowance

Tax-free across all income. Frozen until April 2031. Tapers to zero between £100k and £125,140 of income.

Starting Rate (Savings)

Available only if your non-savings income is under £17,570. Reduces £1-for-£1 once non-savings income passes £12,570.

Personal Savings Allowance

Basic-rate. Higher-rate gets £500. Additional-rate (£125k+) gets nothing — every penny of interest is taxed.

Cash ISA

Completely invisible to HMRC. Doesn't touch your PSA. Drops to £12,000 for under-65s from April 2027 — use it now.

Run your numbers in real time.

2026/27 rates · England, Wales, NI & Scotland (savings always taxed at UK bands)

The three collection routes HMRC uses.

PAYE Tax Code Adjustment

HMRC tweaks your tax code — sometimes mid-year, often at the start of the next tax year — so the underpayment trickles out of your salary or pension over 12 months. Catches the vast majority of cases.

Self Assessment

Interest goes onto your SA100 tax return. Tax due alongside your usual 31 January balancing payment. Banks still report figures to HMRC, so reconciliation mismatches trigger compliance checks.

Simple Assessment (PA302)

HMRC sends you a calculation letter (form PA302) showing exactly what you owe and when to pay. Late payment interest accrues at base rate + 4% — currently 8.5% — so don't ignore the brown envelope.

What's coming next — timeline of changes.

Savings rates 20% / 40% / 45%. Cash ISA limit £20,000 for everyone. PSA £1,000 (basic) / £500 (higher) / £0 (additional). Personal Allowance £12,570 frozen.

Basic-rate dividends now 10.75% (was 8.75%); higher-rate 35.75% (was 33.75%). Additional rate unchanged at 39.35%. Doesn't affect savings interest yet — but signals the direction.

Basic rate becomes 22%, higher rate 42%, additional rate 47%. The PSA, Starting Rate (£5,000) and Personal Allowance are not changing — so you're paying more tax on the same interest above the allowances.

Over-65s keep the full £20,000. Under-65s lose £8,000 of cash ISA headroom — that £8k must go into Stocks & Shares, Innovative Finance or Lifetime ISA instead. The total £20,000 ISA wrapper is intact.

HMRC must apply your Personal Allowance to earned income (salary, pension, self-employment) first. Only any remainder can shelter savings, dividends or rental income. Bad news for retirees with mixed income.

Personal Allowance and tax-band thresholds frozen until April 2031 (extended again at Autumn Budget 2025). Until then, fiscal drag pulls more savers into higher bands every year wages rise.

Common pitfalls that catch real people.

Joint accounts misallocated

Banks sometimes report all interest against the first-named account holder's NI number, leaving the spouse exposed years later when HMRC catches up — often with late-payment interest at 8.5%.

Fixed-rate bond maturity shock

A 3-year bond paying out three years' interest in one tax year can push you from basic to higher rate. HMRC's algorithm doesn't always spot it. Ladder your bonds or warn HMRC in advance.

Scottish & Welsh confusion

Even if you pay Scottish or Welsh rates on your salary, savings interest is always taxed at rest-of-UK rates and bands. Always 20% / 40% / 45% — never the Scottish intermediate rate.

HICBC stealth multiplier

Savings interest counts towards adjusted net income. A £4,500 interest pot can drag you from £58k to £62.5k — losing some Child Benefit through the High Income Child Benefit Charge as well as the tax on the interest itself.

Director's "personal" business saver

If your business savings account is in your personal name (even with the company address), HMRC reports interest against you, not the company. Tax at 40% personal vs 19–26.5% corporation tax — costly mistake.

Side hustle interest forgotten

Vinted, eBay, Etsy and food-delivery apps already share earnings with HMRC under the Digital Platforms Reporting Rules. The interest those earnings generate sitting in your saver is still taxable — and HMRC can cross-reference it.

Your 10-minute action checklist.

Self-Employed, Directors and Business Owners: The Bits Most Articles Skip Over

If you’re self-employed, run a limited company, or have a side hustle alongside the day job, savings interest plays by slightly different rules — and it’s easily the most overlooked area in the practice. I’ve spent more hours than I care to count unpicking five-figure surprise bills that started with someone forgetting that their business current account was paying 3% on the float.

Why Sole Traders and Directors Tend to Get Caught

If you’re a sole trader or in a partnership, all your personal savings interest goes onto your Self Assessment return (boxes on the SA100, or SA104 if you’re in a partnership). HMRC doesn’t tinker with a tax code — they wait until 31 January following the end of the tax year for you to declare it. So for 2025/26 interest, your deadline was 31 January 2026. For 2026/27, it’ll be 31 January 2028. Banks still report the lot automatically though, so if your return doesn’t reconcile with their figures, expect a compliance check and possibly a penalty.

Limited company directors are a slightly different beast. Interest on personal accounts is treated exactly the same as anyone on PAYE — HMRC can collect it through your tax code if you draw a salary. But interest on the company’s business savings account is corporation tax territory entirely, not personal tax. Confusing the two is one of the more expensive mistakes I see.

A Director Story From My Files

Rajesh runs an IT consultancy in Bristol through a limited company, and during 2025/26 he had around £250,000 of company reserves sitting in what he believed was a business savings account paying 4.9%. That generated about £12,250 of interest. So far so good — that should sit inside the company and pay corporation tax at the small profits or marginal rates (19% to 26.5% effective, depending on profit levels and any associated companies).

Except when I pulled out the bank paperwork, the account had been opened in his personal name with the company’s address as correspondence — quite a common quirk where high-street banks have made it easy for sole traders to open “business-style” savings, and the line gets blurred. The bank had reported the full £12,250 against Rajesh’s NI number, not the company’s UTR. He’s a higher-rate taxpayer personally, so his PSA was £500. Tax due at 40% on £11,750 came to £4,700 — versus the roughly £2,300 to £3,250 it would have cost the company at corporation tax rates.

HMRC sent a Simple Assessment in autumn 2025, late-payment interest started ticking from 31 January 2026 onwards at base rate plus 4%, and Rajesh assumed his accountant would just pick it up at corporation tax level. We had to formally close the personal account, transfer the funds into a properly company-named account (so HSBC’s records would show the company’s UTR going forward), and submit evidence to get the personal assessment cancelled. It cost him three months of stress and around £800 in professional fees.

The lesson: check whose name is actually on the account paperwork, not just what the cheque book says. If in doubt, ring the bank and ask whose tax reference they report the interest against.

A Quick Checklist: Is That Business Savings Interest Actually Personal?

Question | Yes → Personal tax | No → Company tax |

Is the account in your personal name only? | ✓ | |

Is it in a “trading-as” name with no company registration? | ✓ (sole trader scenario) | |

Is the account titled “[Ltd Company Name]” with the company number on the paperwork? | ✓ | |

Does the bank ask for personal photo ID rather than company documents to set up withdrawals? | ✓ | |

Is the interest reported against your NI number on HMRC’s records? | ✓ |

If two or more of these tick the personal column, the interest is taxable on you, regardless of whose money it really is. Sort the ownership out, properly, before the next tax year ends.

Side Hustles and the “I Forgot About the Interest” Trap

The gig economy has changed the picture noticeably over the last couple of years. Platforms like Vinted, Etsy, Airbnb, eBay and the food-delivery apps now share data with HMRC under the Reporting Rules for Digital Platforms — they have done since January 2024. So HMRC already knows what you’ve earned through those channels, and they can cross-reference that with the bank account it landed in.

A client of mine in north London earned around £8,000 from Deliveroo last year and stuck most of it in a Marcus account. He thought he was under the £1,000 trading allowance (he wasn’t — that’s for trading income only), and even when we sorted the trading position out, he’d forgotten about the £320 of interest. HMRC hadn’t.

High Income Child Benefit Charge — The Quiet Multiplier

Here’s the one almost nobody mentions in the context of savings. If you or your partner claim Child Benefit, and either of you has an “adjusted net income” over £60,000, the High Income Child Benefit Charge starts clawing the benefit back at 1% for every £200 over £60,000. Once you hit £80,000, the whole thing has been clawed back. (These thresholds were lifted from £50,000/£60,000 to £60,000/£80,000 from April 2024 — the £50k figure you may remember is well out of date now.)

Crucially, savings interest counts towards adjusted net income in full. So a £4,500 chunk of interest can drag you from £58,000 of salary up to £62,500, costing you not only the tax on the interest itself but also a slice of your Child Benefit through HICBC. I’ve seen plenty of couples who could have avoided this by formally moving the savings into the lower-earning partner’s sole name, or — for spouses — declaring an unequal beneficial split via Form 17 within 60 days. One couple I helped saved around £1,800 a year just by formalising a 90:10 split that already reflected reality.

A practical change worth knowing: from October 2025, HMRC let you pay the HICBC through your PAYE tax code without having to file a Self Assessment return at all, provided HICBC is your only reason for filing. That’s a quiet but genuinely useful simplification.

Pensioners — Don’t Leave the Easy Wins on the Table

If you or your spouse were born before 6 April 1935 (rare these days but a few are still with us), you may still qualify for Married Couple’s Allowance, which can reduce your tax bill by up to around £1,108 a year. Most retired couples benefit instead from the Marriage Allowance, where a non-taxpaying spouse transfers 10% of their Personal Allowance (£1,260, worth £252 a year in tax saving) to the higher-earning partner. It’s not free money strictly speaking, but it’s straightforward and underclaimed.

Pensioners with a state pension plus a private pension plus savings often find their PSA evaporates the moment a fixed-rate bond matures and the interest hits all at once. If a three-year bond pays out £6,000 in one go in year three, that’s enough to push someone from basic to higher rate for the year — and HMRC’s algorithm doesn’t always spot that the income is lumpy. Always tell HMRC if you’ve had a bond mature, and consider laddering your fixed savings to spread the tax.

A Few Things I’d Tell Any Client Tonight

Use your Cash ISA before April. £20,000 is invisible to HMRC for tax purposes, full stop. From 6 April 2027 that drops to £12,000 a year for under-65s, so the 2026/27 tax year is genuinely the last shot at the full £20,000 cash allowance for most working-age people.

Premium Bonds aren’t bad as a second-tier shelter. Prizes are tax-free, don’t count towards your PSA, and the prize fund rate has hovered around 3.6% to 4.4% lately. Not guaranteed, obviously, but neither painful nor visible to HMRC.

If HMRC rings (or more likely writes) asking for a coding estimate, err on the high side rather than the low. A small refund is much, much nicer than a P800 in March asking for a four-figure underpayment with interest accruing.

Set a calendar reminder for 30 September every year. Log into your Personal Tax Account, check the “Estimated untaxed interest” line for the current year, and adjust if it’s wrong. Ten minutes a year.

FAQs

Q1: What happens if someone has multiple jobs and savings interest pushes them into a higher tax band mid-year?

A1: In my experience advising clients with two or three part-time roles, this is a real headache that catches people out more often than you’d think. HMRC bases your initial tax code on last year’s interest and assumes a steady income, but if a pay rise or bonus from one job combines with rising savings rates, you can suddenly owe 40% on part of your interest instead of 20%. I’ve had a nurse in Manchester who ended up with a £1,200 underpayment because her second job’s overtime tipped her over £50,270 total income. The fix? Ring HMRC before April with a realistic estimate of your full-year income including projected interest – they can issue an in-year code adjustment and spread the extra tax gently rather than hit you with a big P800 the following autumn.

Q2: Can a person force HMRC to collect savings tax through a lump-sum payment instead of adjusting their tax code?

A2: Yes, absolutely – and it’s something I recommend to clients who hate seeing their monthly payslip shrink unexpectedly. If you’re PAYE and get a P800 showing an underpayment on interest, simply phone HMRC and ask to settle it as a one-off rather than via code. They usually agree, especially if the amount is under £3,000. One of my London clients last year preferred paying £780 straight away from a bonus rather than losing £65 a month for a year – it gave him peace of mind and avoided any risk of late-payment interest if his employer messed up the coding.

Q3: What should someone do if their tax code has been reduced because of savings interest but rates have now fallen dramatically?

A3: Don’t sit on it – I’ve seen people lose hundreds by assuming the lower code is permanent. Log into your Personal Tax Account straight away, check the “estimated untaxed interest” figure HMRC is using (it’s often based on last year’s high rates), then ring the Income Tax helpline with evidence from your current statements showing much lower monthly credits. They can raise your code mid-year and you’ll get the overpaid tax back through bigger payslips almost immediately. A retiree I helped in Oxford reclaimed £1,100 this way after fixed-rate bonds matured and his interest plummeted.

Q4: How does savings interest affect the High Income Child Benefit Charge for families?

A4: This one quietly stings a surprising number of professional couples I advise. Any taxable savings interest counts fully towards your “adjusted net income” for the HICBC, so even £2,000 of extra interest can push you over £60,000–£80,000 and trigger a 1% clawback per £200 excess. Consider a teacher married to an NHS manager – they were fine on salaries alone, but £70,000 in joint savings earning 4.8% added £3,360 interest and suddenly wiped out their entire Child Benefit. The smart move is often shifting the higher-earning partner’s savings into the lower-earner’s sole name (or a formal unequal declaration using Form 17) to keep one person comfortably under the threshold.

Q5: Is there any difference in how savings interest is taxed for Scottish taxpayers compared to the rest of the UK?

A5: Well, it’s worth noting that while your salary might suffer higher Scottish rates (up to 48% top rate now), savings interest itself is always taxed using the UK-wide bands and PSA rules – so you still get the full £1,000 or £500 allowance based on total income under £50,270 or £125,140. I’ve had several Edinburgh clients breathe a huge sigh of relief when I pointed this out; they assumed their 42% intermediate rate applied to interest too. The only practical difference is your tax code starts with an “S” and any collection via PAYE goes partly to Holyrood, but the interest calculation itself is identical.

Q6: What happens if a joint savings account pays interest but one partner earns far less – can the interest be taxed differently?

A6: By default HMRC splits joint interest 50/50, but if you genuinely own the money unequally (say 90/10 because one partner funded it entirely), you can submit Form 17 plus a declaration of beneficial ownership to have it taxed in that proportion. I’ve done this for dozens of couples where the lower-earning spouse holds most savings to preserve their full £1,000 PSA and starting rate band. One couple in Bristol saved £1,400 a year in tax just by formalising a 100/0 split – but you must own the capital unequally in reality, not just shift it for tax reasons, or HMRC will challenge it.

Q7: Does interest from a business current account count as personal savings interest for directors?

A7: Only if the account is actually in your personal name – a surprisingly common slip-up. If it’s titled properly in the limited company name with the company registration number, the interest belongs to the company and suffers corporation tax (19–25%), not your personal 40–45%. I’ve rescued directors who had £200,000+ in a “trading as” sole-trader style account thinking it was business money, only for HMRC to tax it personally. Move it into a proper limited-company account immediately and backdate if possible – the tax saving can be enormous.

Disclaimer

The information provided in this article is for general guidance only and is not intended to constitute professional advice, tax advice, financial advice, legal advice, or any other form of regulated guidance. Although every effort has been made to ensure accuracy at the time of publication, Fair View Accounting Services, including its director, employees, contractors, writers, and content-creation team, accepts no responsibility for any loss, damage, penalty, or consequence arising from reliance on the information contained herein.

UK tax legislation changes frequently, and HMRC interpretations, thresholds, and rules may vary depending on the individual circumstances of each taxpayer. Nothing in this article should be considered a substitute for obtaining formal, personalised advice from a qualified accountant or tax professional. Readers should not take action—or refrain from taking action—based solely on the content published on this website.

Fair View Accounting Services does not guarantee the completeness, accuracy, or ongoing validity of the information provided and assumes no liability for omissions or errors, whether typographical, factual, or technical. By using this content, the reader acknowledges that all responsibility for decisions remains solely with the user.