Over 55s Inheritance Tax Warning

The Looming Inheritance Tax Challenge for Over-55s

Picture this: you’ve spent decades building a comfortable life, perhaps running a small business or accumulating a solid pension pot, only to discover that a hefty chunk could vanish in taxes upon your passing. As someone who’s guided countless clients through these waters, I’ve seen the shock on their faces when they realise inheritance tax (IHT) isn’t just for the ultra-wealthy anymore. With thresholds frozen and new rules kicking in, over-55s in the UK face a stark warning for the 2025/26 tax year and beyond.

Why Over-55s Are Particularly Vulnerable Now

In my practice, I’ve noticed a surge in queries from those in their mid-50s onwards, often prompted by recent Budget announcements. The nil-rate band remains stuck at £325,000 per individual, unchanged since 2009 and now frozen until at least 2030/31 according to the latest Finance Bill 2025-26. Add the residence nil-rate band of £175,000 if you’re leaving your main home to direct descendants, and you might think £500,000 is a safe buffer. But with property prices and asset values rising, more estates are tipping over this edge. Official ONS data shows average UK house prices hovered around £285,000 in 2025, but in hotspots like London, they’re double that—pushing many modest estates into the 40% IHT bracket.

The Freeze Factor and Rising Estate Values

None of us enjoys tax surprises, especially when they’re posthumous. The Office for Budget Responsibility (OBR) forecasts that by 2030/31, IHT receipts could hit £14.5 billion annually, up from £9 billion in 2025/26, largely due to this threshold freeze. For business owners, this is compounded if you’ve got multiple income streams—say, from a company, rentals, and investments. I’ve advised clients with combined assets just over £1 million who assumed they were safe, only to find taper relief erodes the residence band for estates above £2 million. Check your total estate value annually; use HMRC’s online IHT calculator to simulate scenarios, factoring in any Scottish or Welsh property variations where land transaction taxes differ, though IHT itself is uniform across the UK.

Common Misconception: “I’m Not Wealthy Enough”

Be careful here—surveys from firms like Canada Life reveal that 27% of over-55s haven’t even drafted a will, risking intestacy rules that could amplify IHT exposure. In my experience, this stems from a belief that IHT only hits the top 4-5% of estates. But with pensions soon entering the fray, that figure could rise. GOV.UK guidance confirms most estates under £325,000 pay nothing, yet OBR projections indicate fewer than 10% will owe IHT annually, but that’s still tens of thousands more due to inflation. For those with high-income child benefit charges or emergency tax codes from multiple jobs, it’s a reminder to consolidate affairs early; overlooked overpayments can be reclaimed via HMRC’s P800 forms, but don’t let them inflate your estate unnecessarily.

Scottish and Welsh Nuances in Estate Planning

Now, let’s think about your situation if you’re north of the border or in Wales. While IHT rates are UK-wide, succession laws vary—Scotland’s legal rights mean spouses and children have fixed claims, potentially forcing asset sales to cover IHT. I’ve handled cases where Welsh clients underestimated land transaction tax on property gifts, which interacts with IHT’s seven-year rule. Always consult HMRC’s manuals on regional differences; for instance, Scottish taxpayers might face different income tax bands on rental income, affecting overall wealth accumulation and thus IHT liability. Cross-check with GOV.UK’s devolved tax pages to avoid pitfalls like emergency tax on pension drawdowns mimicking higher IHT exposure.

The Risk of Underestimating Multi-Income Scenarios

I’ve seen many clients run into this problem: juggling PAYE from a job, self-assessment from a side business, and pension income. For IHT, it’s the estate’s net value that counts, but errors in income tax can lead to overpayments inflating assets. HMRC notices highlight that high earners (over £50,000) lose child benefit taper, effectively a 60% marginal rate—money that could be gifted to reduce IHT. Verify your tax code via your personal tax account; if it’s BR or emergency, it might signal untaxed income boosting your estate. Business owners, note: corporation tax reliefs don’t directly cut IHT, but efficient extraction via dividends can fund gifts.

Upcoming Changes Amplifying the Warning

Fresh insights from the 2025 Budget: thresholds extended frozen to 2031, meaning fiscal drag pulls more into the net. For over-55s, the big shift is pensions inclusion in IHT from April 2027, per HMRC’s technical consultation. Previously exempt, unused pots will now count towards your estate, potentially hitting 67% effective tax if beneficiaries pay income tax too. OBR datasets underline this could affect 10,500 new estates in 2027/28. If you’re a business owner, add the April 2026 cap on agricultural/business property relief at £2.5 million per estate (up from initial £1 million proposal), with 50% relief beyond—transferable between spouses, but still a clampdown.

Long-Term Residency Rules for Global Assets

Here’s a curveball for those with international ties: from April 2025, IHT shifts to a residency-based system. If you’ve been UK tax resident for 10 of the last 20 years, your worldwide assets are liable— a ‘tail’ persists for up to 10 years after leaving. HMRC manuals clarify transitional rules for non-residents in 2025/26, but for over-55s who’ve lived abroad, this could ensnare overseas properties or investments. I’ve advised expat clients to track residency via statutory tests; miscounting years leads to nasty surprises, as seen in FTT cases on domicile disputes.

Real-Life Pitfall: The Unwritten Will

One client, a 58-year-old business owner, passed without a will—his £600,000 estate faced £110,000 IHT, plus probate delays. Intestacy distributed unevenly, triggering family disputes. Always draft a will; HMRC’s IHT400 form is key for reporting, but errors here invite penalties. Cross-reference with GOV.UK’s will guidance to include IHT-saving clauses like discretionary trusts.

The Looming Inheritance Tax Challenge

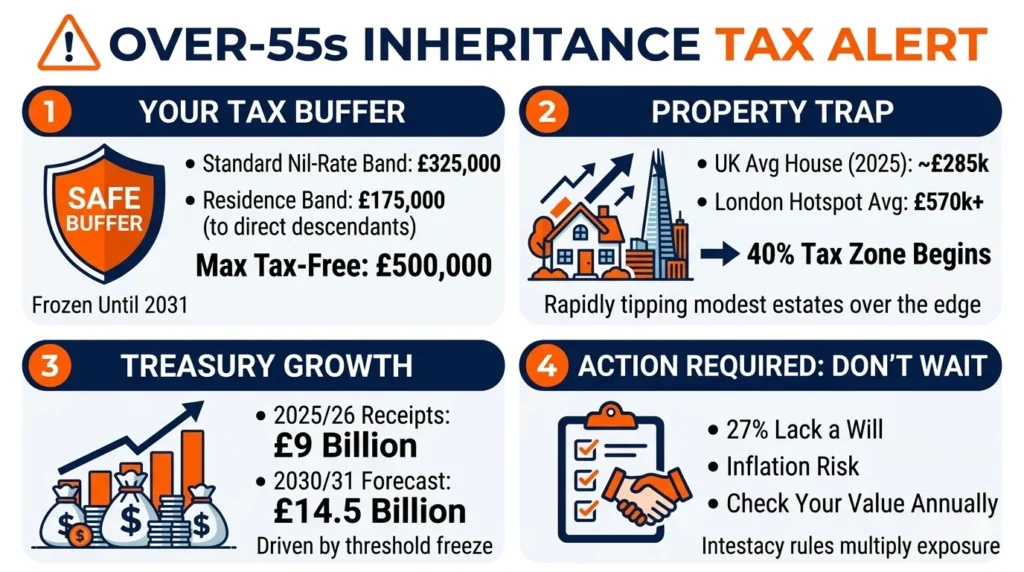

For decades, you've built a comfortable life. But frozen thresholds and rising asset values mean Inheritance Tax (IHT) is no longer just for the ultra-wealthy. Over-55s face a stark reality.

🛡️ The Frozen "Safe Buffer"

The standard nil-rate band has remained stuck at £325,000 since 2009 and is frozen until 2030/31. Even with the added £175,000 residence nil-rate band (applicable when leaving a main home to direct descendants), your total buffer maxes out at £500,000.

Breakdown of the maximum £500,000 tax-free estate threshold.

🏠 The Property Trap

Many assume £500,000 is plenty. However, rising property prices are rapidly tipping modest estates over the edge. While average UK prices hover around £285,000, hotspots like London see values double this amount, instantly breaching the threshold.

House prices compared to the standard £325,000 nil-rate band.

Skyrocketing Tax Receipts

The threshold freeze is highly lucrative for the Treasury. The Office for Budget Responsibility (OBR) forecasts a massive surge in IHT revenue. By 2030/31, receipts are expected to jump from £9 billion to £14.5 billion annually.

Common Misconceptions & Risks

"I'm not wealthy enough." This belief is leaving tens of thousands exposed. Pensions, multiple income streams, and inflation are compounding the risk.

No Will Drafted

Over a quarter of over-55s haven't drafted a will, risking intestacy rules that drastically amplify IHT exposure.

The Tax Bracket

Any portion of your estate that falls above the threshold is subject to a hefty 40% inheritance tax rate.

Taper Relief Trap

For business owners or those with combined assets over £2 million, taper relief actively erodes the residence nil-rate band.

Pensions: The New Frontier in IHT Exposure

By Alistair Thorne, FCA, a UK tax accountant with over 18 years advising taxpayers and business owners on estate planning and inheritance tax strategies.

I’ve watched pension pots grow from modest retirement savings into significant family wealth over the years. For many over-55s, the pension has been a cornerstone of IHT planning—often left untouched, passing IHT-free to heirs. But that era is ending, and the changes hit harder than most realise.

Pensions Entering the IHT Net from April 2027

From 6 April 2027, most unused pension funds and death benefits will count towards your estate for IHT purposes. HMRC’s guidance is clear: this includes defined contribution pots and certain death benefits, regardless of whether trustees have discretion. Previously exempt, these now form part of the taxable estate.

The impact? Estates previously below thresholds could tip over. HMRC estimates around 10,500 new estates will face IHT in 2027/28, with 38,500 paying more overall. For over-55s drawing down gradually, this is a wake-up call—your pot isn’t just for retirement anymore.

How the Inclusion Works in Practice

Be careful here: the value included is the lump sum or fund at death, minus any liabilities. If your estate exceeds £325,000 (or £500,000 with residence nil-rate band), the pension portion faces 40% IHT. Personal representatives (not scheme administrators) report and pay via the IHT400 form.

I’ve seen clients shocked by this—especially those with £500,000+ pots assuming full exemption. Now, even modest pots can push estates into liability if other assets are high. Cross-check with GOV.UK’s pension IHT page for the latest process maps.

Double Taxation Risk: IHT Plus Income Tax

Now, let’s think about your situation if beneficiaries are over 75 or high earners. If death occurs after age 75, beneficiaries face income tax on withdrawals—potentially 45%—on top of the 40% IHT. Effective rates can hit 67% or more.

HMRC promises mechanisms to reclaim overpaid income tax, but the cash flow hit is real. In my practice, I’ve advised clients to consider accelerating drawdowns or gifting now, while weighing income tax implications.

Business Owners: Pensions in Multi-Income Estates

For those with businesses, pensions often sit alongside company shares qualifying for business property relief. The 2026 changes cap 100% relief at £2.5 million per estate (transferable between spouses), with 50% beyond—meaning larger business estates pay 20% effective IHT on excess.

Add a pension pot, and the combined value can erode reliefs faster. One client, a 62-year-old with a £3 million business and £800,000 pension, faced a £200,000+ IHT bill post-2027. Plan holistically—use pensions for retirement, not inheritance.

A Real-Life Tribunal Insight on Relief Claims

While direct pension IHT cases are emerging, related disputes highlight pitfalls. In a 2024 First-tier Tribunal case involving business property relief (similar principles apply), HMRC successfully challenged a claim where assets weren’t genuinely trading—leading to full IHT exposure.

Hypothetically, if a pension-linked investment fails relief tests post-inclusion, the estate pays dearly. Always verify qualifying status; HMRC manuals stress genuine commercial activity.

Action Checklist for Over-55s

- Review your pot annually: Use HMRC’s calculator to model IHT with pension included.

- Consider drawdowns: Withdraw tax-efficiently to reduce estate size.

- Update nominations: Ensure death benefits align with will, but note discretion.

- Seek professional valuation: For business-linked pensions.

- Monitor 2027 guidance: HMRC will refine processes.

The Broader Picture: Frozen Thresholds and Fiscal Drag

The nil-rate band stays £325,000 (plus £175,000 residence band) until 2031. OBR forecasts show rising receipts as more estates exceed this due to inflation.

For over-55s, combining pension inclusion with frozen bands amplifies the warning—many modest estates now face bills.

Over-55s & Inheritance Tax:

The Pension Warning You Can't Ignore

🏛 What Is Changing & Why It Matters

For decades, pension pots were one of the most effective Inheritance Tax (IHT) shelters available to UK taxpayers. They sat outside your estate, passing tax-free to loved ones. That era ends on 6 April 2027.

The Autumn Budget 2024 confirmed that most unused pension funds and death benefits will be drawn into the taxable estate. The Finance Bill 2025–26 formalises this. HMRC's rationale: pensions were increasingly used as a wealth-transfer vehicle rather than for retirement — closing this loophole.

⚡ The Double Taxation Danger

If a pension holder dies after age 75, beneficiaries pay income tax on withdrawals (up to 45%). Once IHT at 40% is layered on top, the effective combined rate can exceed 67%.

📅 Key Dates & Legislative Journey

🧮 Simple IHT Estimator

Illustrative only — not financial advice. Always seek professional guidance for your personal circumstances.

🛡 Mitigation Strategies for Over-55s

Time to act before 6 April 2027. Tap any strategy to expand:

📂 Hypothetical Case Study: The Family Business Owner

A 58-year-old married business owner (Alex) with a growing estate — illustrating how the 2026–2027 reforms interact in practice.

📊 Alex's Estate — Before vs After April 2027

| Pre-2027 | Post-2027 | |

| Main residence | £1,200,000 | £1,200,000 |

| Business (qualifying BPR) | £1,500,000 | £1,500,000 |

| Unused pension pot | Exempt (£0) | +£500,000 |

| Other savings | £200,000 | £200,000 |

| Gross estate | £2,900,000 | £3,400,000 |

| NRB + RNRB (married) | £1,000,000 | £1,000,000 |

| BPR (within £2.5m cap) | £1,500,000 | £1,500,000 |

| Taxable estate | £400,000 | £900,000 |

| IHT @ 40% | £160,000 | £360,000 |

| Extra IHT from pension | — | +£200,000 |

💡 Alex's Mitigation Plan

📉 Projected Savings with Action Taken

| Annual gifts from surplus income (£30k/yr × 5 yrs) | ~£60k IHT saved |

| Pension drawdown at basic rate, re-gifted | Pot reduced by £100k+ pre-2027 |

| Whole-of-life policy in trust (£200k benefit) | Covers remaining bill |

| Spousal bypass trust on nominations | Removes 2nd-gen IHT |

| Projected total saving | £150,000 – £200,000+ |

✅ Immediate Action Checklist for Over-55s

Prioritise these steps before the April 2027 deadline:

- Value your estate holistically — include ALL pensions, property, savings, investments and business interests. Don't wait for 2027.

- Model IHT scenarios now — use the Estimator tab above as a starting point, then engage a professional for detailed analysis.

- Review & update pension nominations — ensure death benefit nominations align with your will and estate planning objectives. Consider spousal bypass trusts.

- Assess your drawdown strategy — could you draw pension funds tax-efficiently (up to personal allowance = £12,570/yr) to reduce the pot and estate size?

- Review gifting opportunities — are you making gifts from surplus income? Have you used your £3,000 annual exemption? Consider the 7-year PET strategy for larger gifts.

- Check Business/Agricultural Relief status — if you hold business assets, confirm qualifying trading status before the April 2026 cap. Restructure if needed.

- Consider life insurance in trust — a whole-of-life policy outside the estate can cover the IHT bill without eroding assets for beneficiaries.

- Update your will — review in light of new pension rules, BPR/APR changes and transferable nil-rate band planning.

- Speak with a qualified professional — an FCA-regulated financial planner and/or specialist tax accountant is essential for personalised advice.

- Monitor HMRC guidance — updated IHT400 guidance, process maps and calculators will be published before April 2027. Check gov.uk regularly.

• gov.uk/inheritance-tax — HMRC IHT hub

• Pension IHT reform — GOV.UK

• MoneyHelper — Inheritance Tax guide

Summary of Key Insights

- Frozen nil-rate bands until 2031 mean fiscal drag pulls more estates into IHT—review yours now.

- Pensions inclusion from April 2027 adds unused pots to estates—accelerate drawdowns wisely.

- The £2.5 million APR/BPR cap from 2026 limits full relief—restructure qualifying assets early.

- Gifting out of surplus income offers immediate exemption—ideal for steady estate reduction.

- Seven-year PETs remain powerful—survive the period, and gifts escape IHT.

- Spouse transferable allowances double thresholds—equalise estates for maximum benefit.

- Business owners: maximise genuine trading for BPR—HMRC challenges weak claims.

- Long-term UK residents face worldwide IHT—track residency years carefully.

- Professional advice avoids pitfalls—tribunal cases show errors prove costly.

- Start planning today—small actions compound into significant family savings.

FAQS

Q1: What happens if an over-55 individual has no direct descendants for the residence nil-rate band?

A1: Well, it’s a bit of a sting, but if you don’t have children or grandchildren—including adopted or step ones—the extra £175,000 residence nil-rate band doesn’t apply, leaving you with just the standard £325,000 threshold. In my experience with clients like a retired teacher in Manchester who had no kids, we focused on charitable bequests to drop the rate to 36%, or gifting assets early to shrink the estate. It’s worth reviewing your will to maximise exemptions, as many overlook how this can bump up the tax bill unexpectedly.

Q2: How does divorce impact the transferable nil-rate band for inheritance tax?

A2: Divorce can complicate things, as the transferable nil-rate band only passes to a surviving spouse or civil partner, not ex-partners. I’ve advised divorced business owners where the first spouse’s unused band was lost, forcing the second estate to pay more at 40%. If you’re over 55 and remarried, consider equalising assets between you and your new partner to preserve bands—perhaps through deeds of variation, but always check with a solicitor to avoid pitfalls like unintended tax triggers.

Q3: Can life insurance policies be used to cover inheritance tax liabilities without adding to the estate?

A3: Absolutely, and it’s a clever move I’ve recommended to many clients. By placing a whole-of-life policy in trust, the payout bypasses your estate, providing liquidity for heirs to pay the 40% tax without selling assets. Picture a 62-year-old shop owner in Birmingham whose family home would have been forced on the market; the trust-held policy covered the bill seamlessly. Just ensure the trust is set up correctly, or it could backfire and inflate your taxable estate.

Q4: What are the inheritance tax implications for foreign property owned by over-55s?

A4: Foreign assets can be a headache, as they’re included in your UK estate if you’re domiciled here, potentially facing double taxation unless a treaty applies—like with France or Spain. One client, a semi-retired expat with a Spanish villa, used local reliefs but still owed UK IHT on the excess over £325,000. For 2025/26, with the residency-based rules, track your UK ties closely; gifting the property might help, but beware capital gains tax overlaps.

Q5: How do AIM shares qualify for business relief in inheritance tax after recent caps?

A5: AIM investments can still offer 100% relief if held for two years and qualifying as trading, but the £2.5 million cap from April 2026 limits full relief—50% beyond that. In practice, for over-55 investors I’ve counselled, diversifying into AIM helped slash bills, like a high-earner whose £400,000 portfolio escaped tax entirely. The key is ensuring they’re not investment-focused; HMRC scrutinises this, so regular reviews are essential to avoid disqualifications.

Q6: What if an over-55 couple owns assets jointly—how does that affect inheritance tax?

A6: Joint ownership as tenants in common allows you to bequeath your share via will, potentially using both nil-rate bands fully. But as joint tenants, it passes automatically to the survivor, deferring tax. I’ve seen couples in their late 50s switch to tenants in common to protect against care fees eroding the estate, saving thousands in IHT. It’s a simple severing of tenancy, but get it wrong and you might miss transferable allowances.

Q7: Are cohabiting partners treated differently for inheritance tax compared to married couples?

A7: Unfortunately, yes—cohabitees don’t get the spousal exemption, so the full 40% could hit on assets over £325,000. A long-term client couple in London learned this the hard way; we mitigated by using trusts for the home and life policies. For over-55s, consider marriage or civil partnership purely for tax perks, or gift assets strategically— but remember, no transferable bands without that legal tie.

Q8: Can skipping a generation by gifting to grandchildren reduce inheritance tax exposure?

A8: It can, through generation-skipping trusts or direct potentially exempt transfers, avoiding a double IHT hit. One family I advised gifted £100,000 to grandkids for education, surviving seven years to make it tax-free. But for over-55s with estates near £1 million, watch taper relief if you don’t make it; it’s not foolproof, and HMRC might challenge if it looks like deprivation of assets for care funding.

Q9: How do Scottish succession laws interact with UK-wide inheritance tax rules?

A9: While IHT is uniform, Scotland’s ‘legal rights’ mean spouses and kids can claim up to half the movable estate regardless of the will, potentially forcing sales to pay tax. A Scottish business owner client had to restructure into trusts to ring-fence assets. For over-55s north of the border, blend UK gifting with Scottish priors—it’s trickier, but early planning avoids family rifts and extra 40% bites.

Q10: What inheritance tax considerations apply to defined benefit pensions for those over 55?

A10: Defined benefit schemes often pass lump sums tax-free if under the lifetime allowance, but from 2027, unused elements count in your estate. I’ve guided public sector retirees to take benefits earlier, like one who commuted part to cash for gifting. Unlike defined contribution, they’re less flexible, so model scenarios—high earners might face 40% plus beneficiary income tax, pushing effective rates sky-high.

Disclaimer

The information provided in this article is for general guidance only and is not intended to constitute professional advice, tax advice, financial advice, legal advice, or any other form of regulated guidance. Although every effort has been made to ensure accuracy at the time of publication, Fair View Accounting Services, including its director, employees, contractors, writers, and content-creation team, accepts no responsibility for any loss, damage, penalty, or consequence arising from reliance on the information contained herein.

UK tax legislation changes frequently, and HMRC interpretations, thresholds, and rules may vary depending on the individual circumstances of each taxpayer. Nothing in this article should be considered a substitute for obtaining formal, personalised advice from a qualified accountant or tax professional. Readers should not take action—or refrain from taking action—based solely on the content published on this website.

Fair View Accounting Services does not guarantee the completeness, accuracy, or ongoing validity of the information provided and assumes no liability for omissions or errors, whether typographical, factual, or technical. By using this content, the reader acknowledges that all responsibility for decisions remains solely with the user.