Agricultural Property Relief: April 2026 Changes Explained

Agricultural Property Relief: April 2026 Changes Explained in the UK

The real question most readers are asking is not simply what Agricultural Property Relief (APR) is. It is whether a farm, farmhouse, tenancy, trust, or lifetime gift will still qualify in the way they expect after 6 April 2026, and how much Inheritance Tax could now be exposed if it does not. The practical answer matters because APR now has to be read alongside the new combined APR/BPR allowance, not in isolation.

What actually changed from 6 April 2026

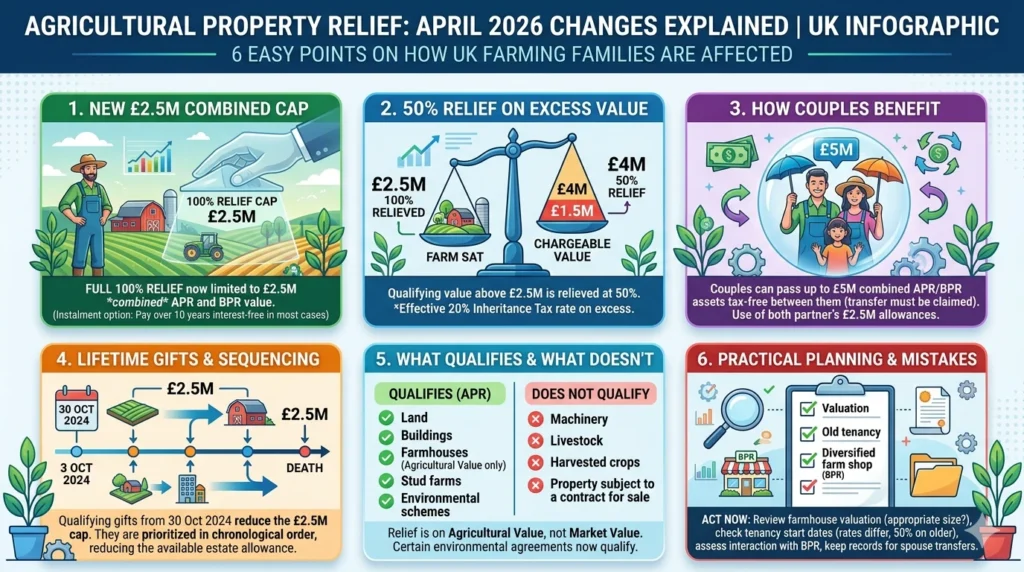

From 6 April 2026, the full 100% relief for qualifying agricultural and business property is restricted to the first £2.5 million of combined APR and Business Property Relief (BPR) value in an estate. Any qualifying value above that is relieved at 50%, which means the effective Inheritance Tax rate on that excess is up to 20% rather than 40%. The relief sits on top of the ordinary Inheritance Tax nil-rate band and any other applicable exemptions.

The government’s own examples still matter here. It says a couple can pass on up to £5 million of agricultural or business assets between them using the £2.5 million allowance each, and up to £5.65 million when the two nil-rate bands are also factored in. That is not a universal outcome, but it is a useful benchmark for family farms and trading estates that are structured sensibly.

There is also a planning point that commercial summaries often miss: from 6 April 2026, tax due on agricultural or business property can generally be paid in instalments over 10 years interest-free in most cases. That does not remove the tax, but it can materially improve cash flow for estates that are asset-rich and cash-poor.

How APR works after April 2026

APR still applies to genuine agricultural property, but it does not cover everything connected with a farm. GOV.UK says qualifying agricultural property includes land or pasture used to grow crops or rear animals, stud farms for breeding and rearing horses and grazing, short-rotation coppice, land temporarily out of production under an environmental land management agreement or crop rotation scheme, some agricultural shares and securities, and farm buildings, cottages and farmhouses. By contrast, farm machinery, derelict buildings, harvested crops, livestock and property subject to a binding contract for sale do not qualify.

That distinction is important because APR applies to the agricultural value of property, not necessarily its market value. A farmhouse may qualify, but only to the extent that it is of a nature and size appropriate to the farming activity being carried on. Any value above agricultural value, such as the extra worth attached to a country residence, is outside APR. That is one of the most common causes of over-optimistic claims.

The occupation and ownership tests also still matter. For property transferred on death or another chargeable transfer, the property must have been owned and occupied for agricultural purposes immediately before the transfer for two years if occupied by the owner, a controlled company, or the owner’s spouse or civil partner, or seven years if occupied by someone else. The property must also be part of a working farm in the UK.

The rate is not automatically 100% either. GOV.UK says 100% relief applies where the owner farmed the land themselves, where it was used by someone else under a short-term grazing licence, or where it was let on a tenancy that began on or after 1 September 1995. In all other cases, the rate is 50%, which is exactly why older tenancies and historic ownership structures often need a fresh review before someone assumes they are fully protected.

Agricultural Property Relief is Changing

From 6 April 2026, APR will no longer provide an unlimited 100% shelter for qualifying assets. The rules are shifting to a combined cap system.

1. The Core Change: Visualising the Cap

Under the new framework, the first £2.5 million of qualifying assets receives 100% relief. However, any qualifying value above this threshold is relieved at 50%, resulting in an effective Inheritance Tax (IHT) rate of 20% on the excess. Tax due on these assets can generally be paid in interest-free instalments over 10 years.

Impact on a £4,000,000 Qualifying Estate

Insight: For a £4M estate, the new rules expose £1.5M to a 50% relief rate. This means £750,000 becomes chargeable, generating a potential IHT liability of £300,000 (before applying the standard Nil-Rate Band), whereas previously the entire £4M was sheltered.

2. What Qualifies (and What Doesn't)

It is a dangerous misconception that everything situated on a farm automatically qualifies for APR. HMRC makes strict distinctions between agricultural assets and other farm-related property.

- • Land used for crops or rearing animals

- • Stud farms (breeding, rearing, grazing)

- • Short-rotation coppice

- • Land under environmental agreements

- • Farmhouses & Cottages (Agricultural value ONLY)

- • Farm machinery and equipment

- • Livestock

- • Harvested crops

- • Derelict buildings

- • Property under a binding contract for sale

The "Agricultural Value" Trap

APR only applies to the agricultural value of a property. For a farmhouse, this is its value specifically as a home for a working farmer. Any "premium" market value—such as its appeal as a luxury country residence—is entirely excluded from APR and may be subject to the full 40% IHT unless covered by other reliefs.

3. Crucial Timing: Gifts & Trusts

The rules formally apply to transfers on or after 6 April 2026, but actions taken prior to this date are heavily scrutinized under the new sequential use rules.

30 October 2024

Qualifying lifetime gifts made on or after this date count against the £2.5M allowance if the donor dies within seven years. Trusts settled after this date face immediate rule application in 2026.

6 April 2026

New £2.5M cap rules officially take effect for all deaths and chargeable transfers. Allowances are applied in strict date order, starting with the earliest lifetime gift.

4. Tenancy Pitfalls

The rate of relief is not uniformly 100%. Historic tenancy agreements can severely limit relief to 50%, even before the new £2.5m cap is applied.

100% Relief: Applies if you farm the land yourself, use short-term grazing licences, or have a tenancy starting on or after 1 Sept 1995.

50% Relief: Often applies to older "protected" tenancies established before 1 Sept 1995.

5. Immediate Action Checklist

Preparation is critical. Protect your estate by executing these five steps before the April 2026 changes take effect.

Map the Estate

Rigorously separate the strict agricultural value from the open market value for all farm dwellings and farmhouses.

Review Tenancies

Check the exact start dates of all let land to confirm whether they fall under the 100% or 50% relief categories based on the 1995 threshold.

Audit Business Assets

Identify which assets fall under Business Property Relief (BPR) versus APR, as both reliefs must now share the same single £2.5m combined cap.

Record Lifetime Gifts

Ensure detailed, accurate records are kept of all qualifying gifts made since 30 October 2024, as these eat into the allowance.

Prepare to Claim the Allowance

Understand that the transfer of an unused allowance between spouses is not automatic. Executors must actively claim it using HMRC forms IHT400 and IHT437 within strict time limits.

What the new cap means in practice

The simplest way to see the effect is by using a worked example. If an individual dies owning £4 million of qualifying agricultural property, the first £2.5 million can still receive 100% relief. The remaining £1.5 million receives 50% relief, so £750,000 is still chargeable. If the person also has the full £325,000 nil-rate band available, the taxable amount falls to £425,000, producing an Inheritance Tax bill of £170,000 at 40%. That calculation is based on the current HMRC rules and the standard IHT rate.

For couples, the position is better but only if the estate planning is tidy. HMRC and HM Treasury both state that any unused £2.5 million allowance can be transferred to a surviving spouse or civil partner, and that if the first death was before 6 April 2026 the full allowance is assumed to be transferable. That is why the government’s own example reaches £5.65 million tax-free for a couple when the APR/BPR allowance and both nil-rate bands are combined.

Lifetime gifts now need closer attention too. For deaths on or after 6 April 2026, the £2.5 million 100% relief allowance includes qualifying agricultural or business property in the estate and qualifying gifts made on or after 30 October 2024 if the gift is brought back into account because death occurs within seven years. HMRC also says the allowance is applied in date order, starting with the earliest qualifying lifetime gift from 30 October 2024. That sequencing can affect the amount left for the estate itself.

The spouse or civil partner transfer claim is not automatic. HMRC says the claim for the unused allowance must be made on the second death, using form IHT400 and form IHT437, normally within four years from the end of the month of death or within six months of the personal representatives starting their role, whichever is later. In practice, that means executors need the right figures and records, not just the broad family story.

Trusts are now part of the same conversation. The £2.5 million allowance also applies to qualifying agricultural or business property held in trusts, but transitional rules depend on when the property was settled and when the next relevant trust charge arises. HMRC’s consultation material shows that property settled before 30 October 2024 is brought into the new regime at the next 10-year anniversary charge on or after 6 April 2026, while property settled on or after 30 October 2024 is affected under the new framework sooner.

Mistakes that keep causing problems

One frequent mistake is treating the whole farm as if it qualifies for APR at 100%. It often does not. The farmhouse may only qualify to the extent of its agricultural value, machinery is excluded, livestock is excluded, and a contract for sale can break relief altogether. In other words, the bill is often decided by what the asset really is, not by what the family has always called it.

Another common error is overlooking environmental land management agreements. HMRC now says land not currently being farmed because it is under an environmental land management agreement can still qualify for APR. That matters for farms that have diversified or entered longer-term land-use change, because the tax treatment no longer has to be assumed from old “active farming only” thinking.

Older tenancy arrangements also need a proper review. The date on which the tenancy began can determine whether the rate is 100% or only 50%, and many owners still assume all let farmland receives the same treatment. That assumption is wrong often enough to change the Inheritance Tax outcome by a very large amount.

It is also easy to miss the interaction between APR and BPR. The new £2.5 million allowance is combined, not separate, so a farm with trading activities, a farm shop, holiday accommodation, or other business assets may need APR and BPR allocated across the estate carefully. HMRC’s apportionment tool exists precisely because estates often contain both types of relievable property.

Finally, do not assume the spouse or civil partner transfer works itself out. If the allowance is not claimed, it is not being used. That is one of the quietest but most expensive admin failures in farm estates.

Agricultural Property Relief & the new £2.5m allowance

From 6 April 2026 the unlimited 100% relief that sheltered family farms is replaced by a combined £2.5 million allowance for Agricultural and Business Property Relief, with 50% relief on the excess. Here is what changes, what stays the same, and how to model the impact.

What actually changes on 6 April 2026

APR has not been abolished. The mechanics still operate, the qualifying property tests are unchanged, and 100% relief continues to apply — up to a limit. What is new is a monetary cap and an interaction with Business Property Relief that did not exist before.

Unlimited 100% relief

- No cap on qualifying APR or BPR value at the 100% rate

- 50% rate only for older AHA tenancies (pre 1 September 1995)

- Lifetime gifts and trust transfers fully relieved on qualifying property

£2.5m combined cap

- 100% relief restricted to the first £2.5m of combined APR + BPR value

- Excess receives 50% relief — effective 20% IHT rate

- Allowance transferable between spouses and civil partners

Up to £5.65m sheltered

- £5m combined APR/BPR allowance across both deaths

- Plus 2 × £325k nil-rate band

- Even if first death was before 6 April 2026, full transfer is assumed

Three quieter changes worth noticing

BPR cut to 50%

- Shares "not listed" on a recognised stock exchange (incl. AIM)

- Drops from 100% to 50% relief, in all circumstances

- Does not consume any of the £2.5m allowance

10 years interest-free

- IHT on APR/BPR property payable over 10 equal annual instalments

- Interest-free in most cases — meaningful for asset-rich, cash-poor estates

- Extended to all property eligible for APR or BPR

CPI-linked from 2031

- £2.5m allowance frozen until April 2031

- From April 2031, increases with the Consumer Prices Index

- Indexation requires a future statutory instrument — not automatic

Worked example: £4m farm, single individual

The owner dies after 6 April 2026 holding £4m of qualifying agricultural property. The £325,000 nil-rate band is fully available against the chargeable amount.

| Step | Calculation | Amount |

|---|---|---|

| Total qualifying APR/BPR value | — | £4,000,000 |

| 100% relief on first £2.5m | −£2,500,000 | £0 chargeable |

| Excess subject to 50% relief | £1,500,000 × 50% | £750,000 |

| Less nil-rate band | −£325,000 | £425,000 chargeable |

| IHT due | £425,000 × 40% | £170,000 |

| Or paid in 10 instalments | £170,000 ÷ 10 | £17,000 per year, interest-free |

Estate Modeller

Estimate the IHT exposure on qualifying APR/BPR property under the post–6 April 2026 regime. For illustration only — ignores RNRB tapering and lifetime gift sequencing.

Result

What still qualifies — and what never did

The qualifying-property tests are unchanged by the 2026 reform. The most expensive mistakes happen here, before the new £2.5m cap is even reached.

Qualifying property

- UK agricultural land and pasture used to grow crops or rear animals

- Farm buildings of a character appropriate to the land

- Farmhouses and cottages occupied for agricultural purposes

- Stud farms for breeding and rearing horses, plus their grazing

- Short-rotation coppice

- Land in a qualifying environmental land management agreement

- Some agricultural shares and securities

Will not qualify

- Farm machinery, plant and equipment

- Derelict buildings no longer in agricultural use

- Harvested crops and livestock (separate IHT treatment)

- Property subject to a binding contract for sale

- Hope value — development uplift over agricultural value

- Land used for livery or non-agricultural diversification

100% versus 50% rate of relief

The headline rate depends on how the land is occupied or let. The £2.5m cap sits on top of these underlying rates — older tenancies that already attract 50% do not benefit from the cap at all.

| Situation | Pre-2026 rate | Effect of new cap |

|---|---|---|

| Farmed in-hand by owner (vacant possession) | 100% | Subject to £2.5m cap; excess at 50% relief |

| Farm Business Tenancy (post 1 September 1995) | 100% | Subject to £2.5m cap; excess at 50% relief |

| Right to vacant possession within 24 months | 100% | Subject to £2.5m cap; excess at 50% relief |

| AHA tenancy commenced before 1 September 1995 | 50% | Cap does not affect this rate — remains 50% |

| Other lettings without vacant possession in 24 months | 50% | Cap does not affect this rate — remains 50% |

Ownership & occupation tests

Owner-occupied

- Property occupied by the owner, a controlled company, or the owner's spouse/civil partner

- For agricultural purposes throughout the two years ending with the transfer

Let to others

- Property owned for at least seven years before the transfer

- Occupied by someone else for agricultural purposes throughout

Reporting & compliance

APR must be claimed; it is not automatic. The personal representatives use:

Estate return

- The full inheritance tax account for the estate

- Includes valuation of relievable property

Schedules

- IHT414: Agricultural relief schedule

- IHT413: Business relief schedule

- IHT437: Claim for spouse's unused allowance

From announcement to commencement

The reform travelled a long road. The shape of the regime moved materially after the 2024 announcement — especially in late December 2025 when the cap was raised to £2.5m and full spousal transferability was confirmed.

Practical strategies before action is taken

Plans built for the old unlimited regime can now waste the new allowance or trigger unexpected charges. The most useful pre-death actions are usually structural.

Audit legacy clauses

- Older wills often pass all relievable property to children on first death

- Under the new rules, this can waste the £2.5m allowance of the first to die

- Review wording before either spouse predeceases

Balance asset holdings

- Where one spouse holds most of the farm, the other may have an unused allowance

- Consider re-aligning ownership in life to use both £2.5m allowances

- Watch the partnership and property law consequences alongside the tax

Review old AHA arrangements

- Pre-1995 AHA tenancies still attract only 50% relief

- Replacing them with FBTs may unlock 100% — subject to the £2.5m cap

- Holding an AHA may also depress freehold value, with mixed effects

Map gifts since 30 October 2024

- Qualifying gifts from this date count against the £2.5m allowance on death

- Allowance is applied in date order — earliest gift first

- Document, value, and check seven-year survival timing carefully

Frequently asked questions

For lifetime gifting, the 100% relief allowance refreshes every seven years — the same look-back window that already applies to potentially exempt transfers. For relevant property trusts, a separate £2.5m trust allowance refreshes every ten years, aligned with the principal trust charge cycle.

However, the seven-year refresh applies only where the donor survives. If the donor dies within seven years and on or after 6 April 2026, the allowance is recalculated with the gift in date-order alongside the death estate.

Any unused part of the £2.5m allowance on the death of the first spouse or civil partner can be transferred to the survivor. If the first death occurred before 6 April 2026, the full £2.5m allowance is assumed to be available for transfer — even though the regime did not exist at that date.

The transfer is not automatic. Personal representatives must claim it on the second death using HMRC form IHT437 alongside IHT400. The same rule applies to the £325,000 nil-rate band (form IHT402).

From 6 April 2026, shares not listed on a recognised stock exchange — including AIM-listed shares — receive Business Property Relief at 50% only, in all circumstances. The same applies to qualifying shares listed on foreign exchanges that are not recognised stock exchanges.

Importantly, the 50% relief on these shares does not consume the £2.5m allowance. They are taxed at an effective 20% rate regardless of how much agricultural or qualifying business property the estate also holds.

Trusts that held qualifying property on or before 29 October 2024 are not brought into the new regime until their next ten-year anniversary charge falling on or after 6 April 2026. Until then, distributions from such trusts remain subject to the old unlimited 100% relief rules.

For trusts settled on or after 30 October 2024, the new £2.5m allowance applies for chargeable lifetime transfers and trust charges from 6 April 2026 onwards. Anti-fragmentation rules give a single £2.5m allowance across all trusts settled by the same settlor — allocated to trusts in chronological order of settlement.

The £2.5m is a combined cap. Where an estate contains both APR and BPR property, HMRC apportions the allowance across the qualifying assets in proportion to their values. HMRC's online apportionment tool covers estates with up to eight APR and eight BPR assets; more complex estates need professional modelling.

This matters in practice for working farms with diversified income — a farm shop, holiday lets, contracting business or agricultural processing — where the same group of assets crosses both reliefs. The order in which the allowance is applied can shift the final IHT figure materially.

Since 6 April 2025, land taken out of agricultural production under a qualifying environmental land management agreement can still attract APR. This change is carried forward into the post-2026 regime — the £2.5m cap and 50% rate above apply in the usual way to such land.

Not every environmental scheme qualifies. Each agreement should be checked against HMRC's list of recognised schemes before assuming the relief continues to apply.

Yes, and the option has been broadened from 6 April 2026. IHT attributable to property eligible for APR or BPR can be paid in ten equal annual instalments, interest-free in most cases. This applies to the chargeable element above the £2.5m allowance — the part that has actually generated a tax charge.

This does not reduce the tax, but for asset-rich, cash-poor farming estates it can prevent forced land sales by spreading the bill across a decade rather than requiring a lump sum within the usual six-month window.

What to do now

The practical job is to map the estate properly before any death, transfer or trust charge happens. That means separating agricultural value from market value, checking tenancy start dates, identifying whether any land is under an environmental agreement, and reviewing whether any assets are actually BPR rather than APR. It also means checking lifetime gifts from 30 October 2024 onwards, because those gifts can now affect how much of the £2.5 million allowance is left.

Where the estate is complex, the figures should be modelled under the current HMRC apportionment approach rather than guessed. HMRC says its tool can be used where the estate has up to eight agricultural and eight business property assets; larger or more complex estates may need professional advice. That is a sensible dividing line, because once there are multiple farms, trusts, mixed assets or historical gifts, the ordering rules start to matter as much as the headline allowance.

Summary of key insights

APR has not disappeared, but it is no longer an unlimited 100% shelter for every qualifying farm asset. From 6 April 2026, the first £2.5 million of combined APR and BPR value gets 100% relief, and qualifying value above that generally gets 50% relief. Couples can still do well, especially where spouse exemptions and transferable allowances are used correctly. The main risks now are valuation mistakes, old tenancy assumptions, trust timing, and poor record-keeping around lifetime gifts and transfers.

FAQs

Q1: Can someone still claim full Agricultural Property Relief if their farm exceeds £2.5 million in value?

A1: Well, it’s worth noting that exceeding £2.5 million doesn’t remove relief altogether—it changes how much of it you get. In practice, the first £2.5 million of qualifying APR/BPR assets can still attract 100% relief, but anything above that only gets 50%. I’ve seen estates where families assumed “the farm is exempt”, only to discover a six-figure tax bill on the excess. The key is to split the valuation carefully between agricultural and non-agricultural elements before assuming the exposure.

Q2: How does APR apply where farmland is owned personally but farmed by a limited company?

A2: In my experience with family farming structures, this is one of the trickiest areas. APR can still apply if the land is occupied for agricultural purposes by a company controlled by the owner. However, the detail matters—control, shareholding, and actual farming activity must align. Where things go wrong is when the company becomes more of a trading or diversified business and the link to agriculture weakens. That’s when HMRC starts questioning whether APR is still appropriate.

Q3: Can someone claim APR on land used for solar panels or renewable energy projects?

A3: This is becoming more common, and the answer is often disappointing. Land used primarily for solar panels typically does not qualify for APR because it is no longer being used for agriculture. I’ve seen cases where only a portion of the land still qualifies, while the rest falls outside APR entirely. If diversification is planned, it’s worth modelling the tax impact before committing, not after.

Q4: Does APR apply differently if the farm includes holiday lets or glamping sites?

A4: Yes, and this is where people get caught out. Agricultural land may still qualify, but holiday lets and glamping operations are not agricultural. They may fall under Business Property Relief instead—but only if they meet trading criteria rather than being mainly investment-based. I’ve seen mixed-use farms where poor structuring meant neither APR nor BPR fully applied to parts of the business.

Q5: What happens if a farmer stops farming shortly before death—does APR still apply?

A5: It depends on timing and intention. APR requires the land to be occupied for agricultural purposes for a qualifying period (typically two or seven years). If farming ceases too early, relief can be lost. However, if the land is temporarily out of production under environmental schemes, it may still qualify. The nuance here is whether HMRC sees the land as still part of a working agricultural setup.

Q6: Can APR be lost if the farmhouse is considered too large or “lifestyle” focused?

A6: Yes, and this is a classic dispute area. The farmhouse must be appropriate to the farming activity. If it looks more like a country estate than a working farmhouse, HMRC may restrict relief to only the agricultural value—or deny it entirely. I’ve seen valuations challenged heavily where the house significantly outweighs the farming operation in scale or value.

Q7: How does APR interact with the nil-rate band and residence nil-rate band?

A7: APR is applied before standard Inheritance Tax allowances. So, you reduce the value of qualifying agricultural property first, then apply the nil-rate band and residence nil-rate band to what remains. In practice, this sequencing can significantly reduce the overall tax bill—but only if everything is correctly categorised at the start.

Q8: Can someone claim APR on land held in a partnership rather than individually?

A8: Yes, but the partnership agreement matters more than many realise. The underlying land must still qualify as agricultural property, and ownership versus partnership use must be clearly documented. I’ve dealt with cases where informal arrangements led to disputes because ownership and use didn’t align properly on paper.

Q9: Does APR apply to land held under a contract for sale at the date of death?

A9: No—and this often comes as a surprise. Once a binding contract for sale exists, APR is generally lost because the property is no longer considered agricultural property in the relevant sense. Timing is everything here. I’ve seen estates accelerate or delay transactions specifically to avoid this issue.

Q10: Can APR be claimed on woodland or forestry land?

A10: Only if it qualifies as agricultural use, which most commercial forestry does not. Woodland relief may apply instead, but that’s a different regime entirely. This is one of those areas where terminology causes confusion—“land” alone is not enough; it must be agricultural in nature.

Q11: How does APR work for lifetime gifts made shortly before death?

A11: This is where the April 2026 changes really bite. Qualifying lifetime gifts made after late 2024 can now use up part of the £2.5 million allowance if the donor dies within seven years. I’ve seen planning strategies backfire because gifts were made without considering how they would reduce relief available to the estate later.

Q12: Can someone rely on APR if they inherit land and then die shortly afterwards?

A12: Potentially, yes—replacement property rules can apply. If the original owner qualified for APR, the successor may still benefit even if they haven’t met the full ownership period themselves. But the conditions are technical, and I’ve seen claims fail where records of prior ownership and use weren’t properly maintained.

Disclaimer

The information provided in this article is for general guidance only and is not intended to constitute professional advice, tax advice, financial advice, legal advice, or any other form of regulated guidance. Although every effort has been made to ensure accuracy at the time of publication, Fair View Accounting Services, including its director, employees, contractors, writers, and content-creation team, accepts no responsibility for any loss, damage, penalty, or consequence arising from reliance on the information contained herein.

UK tax legislation changes frequently, and HMRC interpretations, thresholds, and rules may vary depending on the individual circumstances of each taxpayer. Nothing in this article should be considered a substitute for obtaining formal, personalised advice from a qualified accountant or tax professional. Readers should not take action—or refrain from taking action—based solely on the content published on this website.

Fair View Accounting Services does not guarantee the completeness, accuracy, or ongoing validity of the information provided and assumes no liability for omissions or errors, whether typographical, factual, or technical. By using this content, the reader acknowledges that all responsibility for decisions remains solely with the user.