Inheritance Tax Planning For Married Couples In 2026

Inheritance Tax Planning for Married Couples in 2026

Marriage and civil partnership sit at the centre of the most valuable IHT exemptions available under UK law. The spousal exemption, the transferable nil-rate band, and the transferable residence nil-rate band together create a framework that allows couples to pass wealth between themselves free of IHT and to combine their allowances on the second death. Used well, this framework can shelter up to £1 million from inheritance tax entirely.

Used poorly — or simply left unreviewed as estates grow, pensions change, and family circumstances shift — the same framework produces unexpected tax bills that competent planning could have avoided.

The context in 2026 is materially different from even three years ago. Pension funds will be brought within the IHT net from April 2027. Business property relief and agricultural property relief are being reformed. Nil-rate band thresholds remain frozen until April 2031. Each of these changes affects married couples’ IHT positions, and the interaction between them rewards attention to detail.

The Spousal Exemption: What It Does and What It Doesn’t

Transfers between spouses and civil partners — whether during lifetime or on death — are exempt from IHT without limit, provided the recipient is UK domiciled or has elected to be treated as such. The exemption applies to assets of any value and any type. There is no ceiling.

This is the single most powerful IHT tool available to married couples, and it operates automatically. There is no claim to make, no form to file, and no minimum period of marriage required.

What it does not do is eliminate IHT — it defers it. Assets passing to a surviving spouse are exempt, but when the surviving spouse dies, those assets form part of their estate and may be subject to IHT at that point. The exemption creates a timing benefit, not a permanent escape. Planning that treats spousal transfers as a permanent solution — without considering what happens to the second estate — frequently results in a larger IHT bill on the second death than would have arisen had some assets been distributed differently on the first.

The Domicile Caveat

The unlimited spousal exemption applies only where the recipient spouse is UK domiciled, or where the recipient has made a valid election to be treated as domiciled in the UK for IHT purposes. Where the recipient is non-UK domiciled, the exemption is capped — currently at £325,000. This is a genuinely significant limitation for international couples and one that is often overlooked in estate planning conversations focused primarily on asset values rather than domicile status.

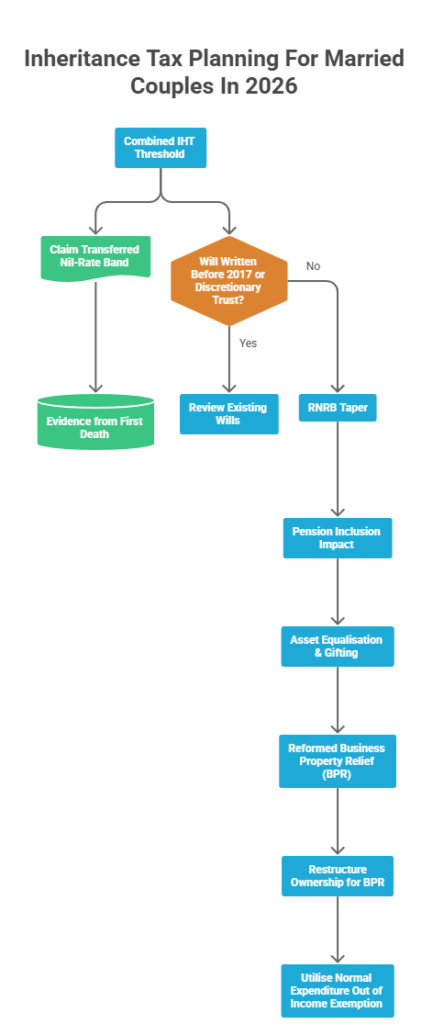

The Transferable Nil-Rate Band

The nil-rate band — currently £325,000 per person — is the threshold below which no IHT is charged. On a first death, if the deceased leaves their entire estate to their surviving spouse (exempt), none of the nil-rate band is used. That unused allowance does not disappear: it is preserved and can be claimed by the surviving spouse’s estate on the second death.

The result is that the surviving spouse’s estate can potentially claim up to double the standard nil-rate band: their own £325,000 plus up to 100% of the deceased’s unused allowance, giving a combined threshold of £650,000.

The transferred allowance is expressed as a percentage, not a fixed pound amount. This matters because if the first death occurred when the nil-rate band was lower — say £300,000 — and the entire band was unused, the estate transfers 100% of the band available at the time of the first death. That 100% is applied to whatever the nil-rate band is at the time of the second death. If the nil-rate band has since increased, the estate benefits from the higher current figure at 100% — which is more generous than the original £300,000.

In the current environment, with the nil-rate band frozen at £325,000 until April 2031, this percentage calculation is less dynamic than it once was. But the principle matters: the transferable nil-rate band is a percentage of the current band, not a fixed inherited sum.

Claiming the Transfer

The transfer of the unused nil-rate band is not automatic. The claim must be made on the IHT402 form, submitted with the deceased’s IHT400 return, within two years of the end of the month in which the surviving spouse dies. Tax Expert Where the first death occurred many years earlier, executors need to locate the grant of probate, the IHT return (or a certificate of nil IHT liability), and evidence of the first spouse’s marital status and the assets they left. For deaths occurring before 2001, these records can be genuinely difficult to trace. Families who maintain a clear record of the first spouse’s estate documents — ideally stored with the will — make the executor’s task considerably easier.

The Transferable Residence Nil-Rate Band

The residence nil-rate band adds a further £175,000 per person to the IHT-free threshold, but only where a qualifying residential property is left to direct descendants — children, grandchildren, stepchildren, or the spouses and civil partners of those individuals.

For couples who meet the conditions, the combined RNRB on the second death can reach £350,000 — in addition to the combined nil-rate band of £650,000. This produces the oft-cited £1 million combined threshold.

The RNRB applies to the value of the qualifying property, not to other assets. If the property is worth less than £175,000, the RNRB applies only to the property value. The shortfall cannot be offset against other assets. And if the property is worth more than £175,000, the RNRB is capped at £175,000 regardless of the property’s full value.

The £2 Million Taper

Both the RNRB and the transferable RNRB are subject to a taper. The RNRB is reduced by £1 for every £2 by which the estate exceeds £2 million. At £2.35 million, the RNRB is eliminated entirely. UK Parliament For couples with larger estates — particularly those where the surviving spouse accumulates the combined estate over time — the taper can significantly reduce or eliminate the RNRB benefit.

The calculation applies to the estate at the time of each death separately. This means the second death estate is assessed independently. If the combined estate has grown substantially between the first and second death — through investment growth, property appreciation, or pension inclusion from April 2027 — the surviving spouse’s estate may breach the £2 million threshold even if the joint estate appeared comfortably below it during the first spouse’s lifetime.

The Interaction With Wills: A Common Mistake

Wills written before the RNRB was introduced in April 2017 — and many written since — may contain provisions that inadvertently prevent the RNRB from being claimed. Discretionary trust arrangements, which were widely used before the transferable nil-rate band made them largely redundant, route assets through a trust rather than directly to descendants. Because the property does not pass directly to a qualifying descendant, the RNRB condition may not be met.

The fix — where the will contains such provisions — may be available posthumously through a section 144 appointment within two years of death, redirecting assets from the trust to qualifying beneficiaries. But this requires professional attention promptly after the death, not several years later. The safer approach is to review the will now and ensure it is aligned with the current framework.

Worked Example: The Combined IHT Position on the Second Death

A couple in their mid-seventies have the following estate on the death of the second spouse:

- Main residence: £550,000

- Savings and investments: £280,000

- ISA portfolio: £120,000

- Pension fund (pre-April 2027, therefore outside IHT): £300,000

- Total taxable estate: £950,000

The first spouse died six years ago, leaving everything to the surviving spouse. Their full nil-rate band and full RNRB were unused.

On the second death, the estate claims:

- Own nil-rate band: £325,000

- Transferred nil-rate band (100%): £325,000

- Own RNRB (property passes to three adult children): £175,000

- Transferred RNRB: £175,000

- Total threshold: £1,000,000

Taxable estate of £950,000 falls below the combined threshold. IHT: nil.

Now consider the same couple, but the second death occurs after April 2027, and the pension fund is now included:

- Total taxable estate: £1,250,000

Still below the £1 million combined threshold. No IHT.

Now consider a couple with larger assets — property worth £750,000, savings of £450,000, investments of £300,000, and a pension of £600,000 on the second death after April 2027:

- Total taxable estate: £2,100,000

The estate exceeds £2 million by £100,000. The RNRB taper reduces both the own RNRB and the transferred RNRB by £50,000 each, eliminating £100,000 of combined RNRB. The effective combined threshold is £900,000 rather than £1 million. IHT at 40% on the £1,200,000 excess: £480,000.

This is the scenario that pension inclusion creates for many couples who previously assumed they were comfortably within the £1 million threshold.

Inheritance Tax Planning for Married Couples

Navigating the 2026/2027 Legislative Shocks

Building the £1M Shelter

Marriage and civil partnership sit at the centre of the most valuable IHT exemptions. The framework allows couples to pass wealth free of IHT and combine allowances on the second death.

By combining standard Nil-Rate Bands (NRB) and Residence Nil-Rate Bands (RNRB), a surviving spouse can shelter up to £1,000,000 from the 40% tax rate. However, these allowances must be actively claimed and rely on specific conditions, such as leaving a qualifying residence to direct descendants.

- ✔ Unlimited Spousal Exemption (if UK domiciled)

- ✔ 100% Transferable NRB

- ✔ 100% Transferable RNRB

Composition of the Combined Threshold

Values represent maximum possible combined allowances on second death.

The £2M Taper Cliff-Edge

RNRB drops by £1 for every £2 the estate exceeds £2,000,000.

The £2 Million Taper Trap

The combined £1 million threshold is not guaranteed for wealthy estates. Both the RNRB and the transferable RNRB are subject to a strict taper.

If the second estate exceeds £2 million, the RNRB is reduced. For an estate reaching £2.35 million, the £350,000 combined RNRB is wiped out entirely.

The April 2027 Pension Shock

Historically outside the estate, pension funds will be added to the taxable estate from April 2027. This single change drastically alters the math for the £2M taper.

Scenario Parameters

- Property: £750,000

- Savings/Investments: £750,000

- Pension Fund: £600,000

Pre-2027, this estate sits comfortably at £1.5M, fully sheltered by the £1M threshold (as it's under the £2M taper limit). Post-2027, the inclusion of the £600k pension triggers the taper, reducing the threshold to £900k and exposing £1.2M to 40% tax.

Tax Impact Comparison (Same Assets)

Strategic Defences & Mitigation

1. Equalising Estates

Asymmetric wealth can cause the surviving spouse to breach the £2M taper. Balancing assets via IHT-free spousal transfers ensures both NRB and RNRB are utilized efficiently on the first death.

2. Lifetime Gifting & Drawdown

Leveraging exemptions to move wealth outside the estate before death. Coordinated giving doubles allowances.

-

➔

Annual Exemption £3,000 per spouse per year. £60,000 sheltered over 10 years for a couple.

-

➔

Normal Expenditure Out of Income Unlimited exemption for habitual gifts made from surplus income (pensions/rentals).

-

➔

Pension Drawdown (Post-2027 strategy) Accelerating drawdown to fund exempt gifts reduces the residual taxable pension pot.

Lifetime Gifting: How Couples Can Use the Rules Together

Each spouse has their own annual gift exemption of £3,000 per year, which can be carried forward one year if unused. Used by both spouses, the combined exemption is £6,000 per year — £12,000 if the prior year’s allowances were unused. Over ten years, regular use of both exemptions shelters £60,000 from the estate.

The normal expenditure out of income exemption is potentially far more valuable. Gifts from regular income that do not reduce the donor’s standard of living can be exempt from IHT without limit, provided they form part of a habitual pattern of giving. TaxYZ For couples where one or both have pension income, investment income, or rental income that genuinely exceeds their living costs, this exemption allows regular gifts — monthly payments to children, grandchildren, or payment of school fees — to leave the estate completely free of IHT, regardless of amount.

The conditions require genuine surplus income — not capital — and a consistent pattern rather than ad hoc transfers. Documentation is essential. A simple record maintained annually, showing income received, expenditure, and the habitual gift payments made, is the evidence an executor will need if HMRC questions the exemption after death. Couples who make regular financial contributions to family members but have never formally documented them as a normal expenditure out of income arrangement are at risk of those gifts being treated as potentially exempt transfers and falling back into the estate if death occurs within seven years.

The Seven-Year Clock on Larger Gifts

Gifts to individuals that are not covered by any exemption are potentially exempt transfers. They fall outside the estate if the donor survives seven years. Both spouses can make PETs independently, and the seven-year clock runs from the date of each gift for each donor separately. A couple who makes coordinated gifts — one from each spouse — to the same recipient in the same year is making two separate PETs, each with its own clock. If one spouse dies within seven years, their PET fails, but the other spouse’s equivalent gift remains on its own independent trajectory.

This independent treatment creates a planning advantage. Rather than funnelling gifts from one spouse’s assets, using both spouses’ capacity to make PETs doubles the amount that can potentially leave the combined estate within a given period, with each gift assessed on its own merits.

Equalising Estates: Why Asset Balance Matters

A common problem in married couples’ IHT planning is asymmetric wealth — one spouse holds the majority of the assets, while the other has relatively little. This matters because the transferable nil-rate band passes unused allowance to the second estate, but the RNRB is tied to the property and only applies where the qualifying residence passes to direct descendants. If the wealthier spouse dies first and leaves everything to the surviving spouse, the second estate may be very large while still having the benefit of the transferred allowances. But if the surviving spouse’s estate then exceeds £2 million, the RNRB taper bites.

Conversely, if the wealthier spouse dies second, their estate may exceed the combined thresholds significantly, with no further transfer mechanism available.

Equalising assets between spouses during their lifetimes — using the spousal transfer mechanism, which is free of IHT and CGT on a no-gain, no-loss basis — creates a more balanced position. If both spouses hold roughly equivalent estate values, the first death can make use of both the nil-rate band (partly used, giving assets directly to descendants rather than everything to the spouse) and the RNRB, rather than wasting both on an entirely exempt spousal transfer.

Using the Nil-Rate Band on the First Death

Many couples assume that leaving everything to the surviving spouse is always the optimal approach. It is not — and it is the most commonly underexplored area in couples’ IHT planning. If the first spouse to die leaves assets up to the value of their nil-rate band directly to children or grandchildren, those assets avoid IHT on the first death and are no longer in the surviving spouse’s estate. The surviving spouse retains the comfort of the spousal exemption on the remainder, and also retains the ability to use 100% of the deceased’s transferred nil-rate band on their own death — but applied to a smaller second estate.

The practical version: the first spouse leaves £325,000 to adult children directly and the balance to the surviving spouse. The first estate has no IHT (the direct bequest is within the nil-rate band; the spousal transfer is exempt). The surviving spouse’s estate is now £325,000 smaller than it would otherwise have been — and that is before any growth or further accumulation. On the second death, the estate has a smaller taxable value, and the transferred 100% nil-rate band supplements the surviving spouse’s own allowance. The combined threshold is the same, but the estate it needs to shelter is smaller.

Whether this approach suits a particular couple depends on whether the surviving spouse can sustain their lifestyle without access to those assets, and on the relative ages and health of both spouses. It is a planning decision that requires genuine reflection, not a mechanical formula.

Business and Agricultural Property Relief for Business-Owning Couples

From April 2026, the reformed business property relief and agricultural property relief rules apply a 100% relief rate to the first £1 million of qualifying assets, with the excess attracting only 50% relief — meaning an effective 20% IHT rate on qualifying business or agricultural assets above that threshold.

For married couples where one or both spouses own qualifying business or agricultural assets, this reform creates a new planning consideration. The £1 million 100% relief allowance applies per individual, not per couple. If one spouse holds £2 million of qualifying business assets, £1 million attracts full relief and the excess £1 million is subject to the 50% rate. If those assets could be partially restructured so that both spouses hold qualifying interests, each potentially has access to the £1 million 100% relief, sheltering £2 million at 100% rather than £1 million.

Transfers of business assets between spouses can be made on a no-gain, no-loss basis for CGT, and may also attract spousal IHT exemption for lifetime transfers. TaxYZ Whether the restructuring of business ownership achieves the intended result requires confirmation that each spouse holds genuine qualifying interests — HMRC will not accept paper ownership that does not reflect economic reality. For family farms or trading companies where both spouses are genuinely involved, the restructuring is often straightforward. For businesses where one spouse has never been involved, it requires more careful structuring.

The April 2027 Pension Interaction: What Couples Need to Do Now

The inclusion of pension funds in estates from April 2027 will affect many couples who previously assumed their combined estate was within the £1 million threshold. The pension fund — which has historically been outside the estate — will now be added to property, savings, and investments when assessing both the IHT charge and the £2 million RNRB taper.

For couples where both spouses have defined contribution pensions, both pots are potentially in scope. The first spouse to die may have a pension that would have passed to the surviving spouse tax-free under the spousal exemption; the spousal pension transfer exemption is preserved under the new rules. But the pension remaining in the surviving spouse’s pot — plus any inherited pension — will form part of the second estate and may push it over both the nil-rate band thresholds and the RNRB taper threshold.

The practical response involves three considerations. First, reviewing pension nominations to ensure they reflect current wishes and the post-2027 IHT implications — directing pension funds to a spouse remains exempt, but directing them to adult children will attract IHT. Second, modelling the likely second estate value with pension inclusion and checking whether it breaches the £2 million taper threshold. Third, for couples with significant pension funds who do not need all of them for living costs, considering whether accelerating drawdown and making gifts from the proceeds — using the normal expenditure out of income exemption where applicable — reduces the residual pension pot and hence the future IHT exposure.

Inheritance Tax Planning for Married Couples

Allowances, reforms and what's coming in 2026 & 2027 — explained interactively.

The £1 million headline

A married couple or civil partners can shelter up to £1 million from IHT on the second death — combining two nil-rate bands (£650,000) and two residence nil-rate bands (£350,000), provided the family home passes to direct descendants.

The spousal exemption

Transfers between UK-domiciled spouses or civil partners — during life or on death — are exempt without limit. No claim, no form, no minimum marriage period. But this defers tax; it doesn't eliminate it.

Frozen until April 2031

The Autumn Budget 2024 confirmed all IHT thresholds are frozen until 5 April 2031. As asset values rise, more estates are pulled into the IHT net — fiscal drag in action.

Pensions in scope from 2027

From 6 April 2027, most unused pension funds will form part of the deceased's estate for IHT — a major change for couples relying on pension wealth as a transfer tool.

Nil-Rate Band (NRB)£325,000

The standard threshold below which no IHT is charged. Frozen at £325,000 since April 2009 — and now confirmed frozen until April 2031. On the first death, any unused proportion transfers to the surviving spouse's estate, expressed as a percentage (not a fixed sum).

Claimed via form IHT402, submitted with the IHT400 return within two years of the surviving spouse's death.

Residence Nil-Rate Band (RNRB)£175,000

An additional allowance available when a qualifying residence passes to direct descendants — children, grandchildren, stepchildren, adopted or foster children, and their spouses. Unused RNRB transfers to the surviving spouse, giving a combined RNRB of up to £350,000.

Taper warning: Reduced by £1 for every £2 the estate exceeds £2 million. Eliminated entirely at £2.35m (individual) or £2.7m (couple).

Spousal ExemptionUnlimited

Transfers between UK-domiciled spouses and civil partners are entirely free of IHT, with no upper limit. Where the recipient is non-UK domiciled, the exemption is capped at £325,000 — unless they elect to be UK-domiciled for IHT purposes.

Annual Gift Exemption£3,000/yr

Each spouse has £3,000 per year — combined, that's £6,000 annually, or £12,000 if the prior year's allowance was unused. Over ten years, regular use shelters £60,000 from the estate.

Normal Expenditure out of IncomeNo Limit

Gifts from regular surplus income that don't reduce the donor's standard of living are exempt without limit — provided they form a habitual pattern. Documentation is essential: keep an annual record of income, expenditure, and gifts.

BPR & APR (Reformed April 2026)£2.5m / 100%

From 6 April 2026, Business and Agricultural Property Relief is capped: 100% relief on the first £2.5 million of qualifying assets per individual; 50% relief above that (effective 20% IHT rate). The allowance is transferable between spouses — couples can shelter up to £5 million.

Originally set at £1m in October 2024, increased to £2.5m on 23 December 2025 after industry lobbying.

Estate on second death

Adjust the sliders. We assume both spouses' allowances and RNRBs are fully transferable, with the property passing to direct descendants.

Illustrative only. Real planning needs professional advice — domicile, lifetime gifts, trusts, and reliefs all affect the outcome.

BPR & APR Reform Takes Effect

100% relief now capped at £2.5m of qualifying business or agricultural property per individual. 50% relief above that (effective 20% IHT). Transferable between spouses — up to £5m combined.

All Thresholds Frozen

NRB (£325k), RNRB (£175k) and £2m taper threshold remain unchanged through 5 April 2031. Asset growth quietly pulls more estates into IHT.

Pensions Brought Into IHT

Most unused defined-contribution pension pots become part of the estate for IHT. Spousal pension transfers remain exempt; transfers to adult children attract IHT. Pension providers will pay tax directly to HMRC.

BPR/APR Indexation (Proposed)

The £2.5m allowance is currently drafted to rise with inflation from 2031 — though whether indexation actually happens, or thresholds are frozen further, remains to be seen.

Equalise estates between spouses

Asymmetric wealth wastes allowances. Use the IHT-free, no-gain-no-loss spousal transfer to balance estates, so both nil-rate bands and RNRBs can be used efficiently across both deaths.

Use the NRB on the first death

Leaving £325k directly to children on the first death (rather than everything to the spouse) reduces the second estate while still preserving 100% of the transferable NRB. Often overlooked.

Document gifts from surplus income

Normal expenditure out of income is unlimited — but only if it's habitual and demonstrable. Maintain an annual income/expenditure/gifts record. Without it, HMRC may treat gifts as PETs.

Coordinate PETs from both spouses

Each spouse's seven-year clock runs independently. Two coordinated gifts to the same recipient — one from each spouse — is two separate PETs, doubling the capacity that can leave the combined estate.

Review pension nominations before 2027

From April 2027, pension nominations to a spouse remain exempt; nominations to adult children become taxable. Model the post-2027 estate, check the £2m taper threshold, consider accelerating drawdown for surplus-income gifting.

Audit pre-2017 wills for RNRB compatibility

Discretionary trust wills can inadvertently block the RNRB (property doesn't pass directly to descendants). A section 144 appointment within two years of death may fix it — but reviewing the will now is safer.

Restructure business assets across spouses

The £2.5m BPR/APR allowance is per individual. If one spouse holds £5m in qualifying assets, restructuring so each spouse holds genuine qualifying interests can shelter the full amount at 100% rather than half at 50%.

Maintain clear estate records

For deaths before 2001, tracing the first spouse's estate documents is genuinely difficult. Store probate records, IHT returns, and evidence of marital status alongside the will. Future executors will thank you.

Key Takeaways

- The combined IHT threshold for married couples and civil partners can reach £1 million — comprising two nil-rate bands of £325,000 each and two residence nil-rate bands of £175,000 each — but only where the qualifying conditions are met and the claim is made correctly.

- The transferred nil-rate band must be claimed on the second death using form IHT402. It is not automatic. Tax Expert Executors need evidence from the first death, which may be decades old.

- Wills written before 2017, or containing discretionary trust arrangements, may inadvertently block the RNRB. Review existing wills to confirm they are aligned with the current framework.

- The RNRB taper reduces the allowance by £1 for every £2 of estate value above £2 million. UK Parliament Pension inclusion from April 2027 will push more couples over this threshold than currently anticipated.

- Equalising assets between spouses, using the first death to pass some assets directly to descendants, and making coordinated use of both spouses’ PET and gifting capacity all reduce the combined estate’s IHT exposure over time.

- The reformed business property relief from April 2026 applies the £1 million 100% relief threshold per individual. Couples with qualifying business or agricultural assets should review whether restructuring ownership between spouses makes the combined relief more efficient.

- The normal expenditure out of income exemption is among the most underused tools available to couples with surplus income — properly documented, it allows unlimited regular gifts to leave the estate free of IHT and the seven-year clock entirely.

FAQs

Q1: Can a couple lose the transferred nil-rate band if the surviving spouse remarries after the first spouse dies?

A1: Well, it is worth noting that remarriage does not cancel the transferred nil-rate band already inherited from the first spouse. The surviving spouse retains the right to claim the first spouse’s unused nil-rate band on their eventual death, regardless of whether they subsequently marry again. However, the calculation becomes more complex where the surviving spouse also predeceases their second spouse and that second spouse then makes a claim. Each individual can only benefit from a maximum of one additional transferred nil-rate band — meaning the surviving spouse’s estate on their death can claim at most 100% of the current nil-rate band as a transfer from the first deceased spouse, in addition to their own. The second marriage itself does not generate a further transfer entitlement unless the second spouse also predeceases them and left unused allowance. Executors handling the estate of someone who was widowed and then remarried need to trace the allowances from both marriages and confirm the maximum transferable percentage. It is the combined percentage of unused allowance from all prior spouses that matters, subject to the 100% ceiling. Remarriage after bereavement is more common than people appreciate among older clients, and getting the transferred nil-rate band arithmetic right in that scenario requires careful work.

Q2: Does the spousal IHT exemption apply to gifts made to a spouse who is in the process of divorcing the donor at the time of death?

A2: In my experience, this is an area where the timing of legal events matters enormously and where assumptions can lead to significant errors. The spousal IHT exemption applies to transfers between legal spouses and civil partners. A couple remains legally married until decree absolute — now called a final order in England and Wales following the Divorce, Dissolution and Separation Act 2020 changes. If one spouse dies before the final order is made, they are legally still married at the point of death, and the unlimited spousal exemption applies to any assets passing to the surviving spouse under the will or intestacy rules. Assets passing under the will to a spouse who is separated but not legally divorced are exempt from IHT. The complication arises on intestacy — if there is no will, the intestacy rules direct assets to the legal spouse, which may not reflect the deceased’s actual wishes at all. This makes having an up-to-date will absolutely critical during any period of separation. Assets directed by will to a spouse before divorce is finalised attract the spousal exemption, but this is often the last outcome the deceased would have chosen. Conversely, once the final order is granted, the exemption no longer applies and any assets passing between former spouses are treated as gifts to unconnected individuals.

Q3: If a married couple own property as tenants in common rather than joint tenants, how does that affect their IHT planning options?

A3: This distinction is genuinely one of the most practically important property law points in couples’ IHT planning, and it is one that many couples do not know they need to make. When property is owned as joint tenants, the right of survivorship applies automatically — on the death of one owner, their share passes directly to the surviving owner regardless of what the will says. This means the deceased’s share of the property cannot be directed to children or other beneficiaries on the first death, because it has already transferred to the surviving spouse by operation of law. For a couple trying to use the first death to pass assets directly to descendants and reduce the second estate, joint tenancy prevents that strategy for the property element. Tenants in common, by contrast, each own a defined share — typically 50% each — and that share can be directed by will to whoever the deceased chooses. This allows the first spouse to leave their share of the property directly to children, potentially using the nil-rate band and residence nil-rate band on the first death rather than deferring everything to the second. Severing a joint tenancy — converting it to tenants in common — is a relatively straightforward legal process requiring notice to the other owner. Many solicitors recommend doing this when reviewing wills, precisely because it restores flexibility in directing the first spouse’s share of the property. The decision should be made alongside will planning rather than in isolation.

Q4: What happens to the residence nil-rate band if a couple’s only property is worth less than the available combined RNRB?

A4: Well, the short answer is that the RNRB is capped at the value of the qualifying property, and any unused balance does not carry over to shelter other assets in the estate. So if a couple’s combined RNRB entitlement on the second death is £350,000 but the qualifying property is only worth £200,000, the RNRB produces £200,000 of relief — not £350,000. The shortfall of £150,000 cannot be applied to savings, investments, or any other estate assets. This is one of the most frequently misunderstood features of the RNRB. The relief is property-specific. For couples who have downsized or live in a modest property, this means the widely advertised £1 million combined threshold may overstate their actual effective threshold. The downsizing addition can help where the couple has previously lived in a more valuable property — if they sold a qualifying home on or after 8 July 2015 and moved to a smaller one, the estate can potentially claim RNRB based on the former property’s value rather than the current one, subject to conditions. This makes the downsizing rules particularly relevant for couples who moved to retirement accommodation or smaller properties after their children left home.

Q5: Can a same-sex couple who have been in a civil partnership since before the Civil Partnership Act 2004 claim the same IHT treatment as a married couple?

A5: The Civil Partnership Act 2004 came into force on 5 December 2005, which is the earliest date civil partnerships could be formally registered in the UK. Same-sex couples who were together before that date but were unable to register a civil partnership at the time did not have legal recognition of their relationship for IHT purposes during that period. However, once they registered, the spousal IHT exemption and all the associated reliefs — transferable nil-rate band, transferable RNRB, and so on — applied in full from the date of registration. The nil-rate band transferred on the first death would be based on any unused allowance from that death onwards, not from any earlier cohabitation period. For couples who registered a civil partnership in the mid-to-late 2000s and experienced a first death since then, the transferred nil-rate band calculation uses the band available at the time of the first death and the proportion left unused — exactly as it would for any other couple. Same-sex married couples, following the Marriage (Same Sex Couples) Act 2013, have identical IHT treatment to opposite-sex married couples in all respects. The IHT framework does not distinguish between marriage and civil partnership.

Q6: If the first spouse to die had previously been married and had used some of their nil-rate band in a prior marriage, how much can be transferred to the surviving spouse?

A6: In my experience, this scenario comes up more often than people expect — particularly for those in second marriages where one partner was previously widowed rather than divorced. The transferable nil-rate band is calculated based on the percentage of the nil-rate band that was unused on the first death in the current marriage. If the first spouse used some of their nil-rate band in a prior marriage — for example, they left assets to children from their first marriage rather than to their first spouse — the unused portion from that earlier arrangement may have already been transferred to the first spouse who predeceased them in that previous marriage. HMRC allows each surviving spouse to inherit at most 100% of the current nil-rate band as a transfer — meaning a surviving spouse who has outlived two previous spouses could in theory claim up to 200% of the nil-rate band, capped at 100% of the current figure. However, if the most recent deceased spouse had themselves previously transferred allowance to a prior spouse and that prior spouse is still living, the position requires careful tracing. The key figure for the current surviving spouse is the percentage of the most recently deceased spouse’s nil-rate band that was unused at their death — which is then applied to the current band at the time of the surviving spouse’s own death.

Q7: Does making a deed of variation after a spouse’s death to redirect assets to children affect the transferred nil-rate band calculation?

A7: Well, this is a planning tool that is more useful than many families realise, and the IHT treatment of it is genuinely favourable. A deed of variation executed within two years of death can redirect inherited assets to different beneficiaries, and for IHT purposes the variation is treated as if the deceased had made that arrangement in their will. So if a surviving spouse inherits everything from their deceased partner but subsequently signs a deed of variation redirecting, say, £325,000 worth of assets to their adult children, HMRC treats the deceased as having left those assets directly to the children. The effect is twofold: first, those assets are now potentially within the deceased’s nil-rate band on the first death, reducing the first estate’s IHT exposure if applicable. Second, those assets no longer form part of the surviving spouse’s estate for IHT purposes — they have been removed from the estate they would otherwise inherit and have passed directly to the next generation. The assets removed by the deed of variation do not reduce the transferred nil-rate band entitlement, because the deed is treated as the deceased’s own direction — meaning the nil-rate band can still be transferred to the surviving spouse on their later death. This combination — removing assets from the surviving spouse’s estate while preserving the transferred nil-rate band — makes a well-timed deed of variation one of the more powerful posthumous planning tools available to couples.

Disclaimer

The information provided in this article is for general guidance only and is not intended to constitute professional advice, tax advice, financial advice, legal advice, or any other form of regulated guidance. Although every effort has been made to ensure accuracy at the time of publication, Fair View Accounting Services, including its director, employees, contractors, writers, and content-creation team, accepts no responsibility for any loss, damage, penalty, or consequence arising from reliance on the information contained herein.

UK tax legislation changes frequently, and HMRC interpretations, thresholds, and rules may vary depending on the individual circumstances of each taxpayer. Nothing in this article should be considered a substitute for obtaining formal, personalised advice from a qualified accountant or tax professional. Readers should not take action—or refrain from taking action—based solely on the content published on this website.

Fair View Accounting Services does not guarantee the completeness, accuracy, or ongoing validity of the information provided and assumes no liability for omissions or errors, whether typographical, factual, or technical. By using this content, the reader acknowledges that all responsibility for decisions remains solely with the user.