Fiscal Drag Explained: Why Millions In The UK Are Paying More Tax Without Earning More

Understanding Fiscal Drag and Its Mechanics

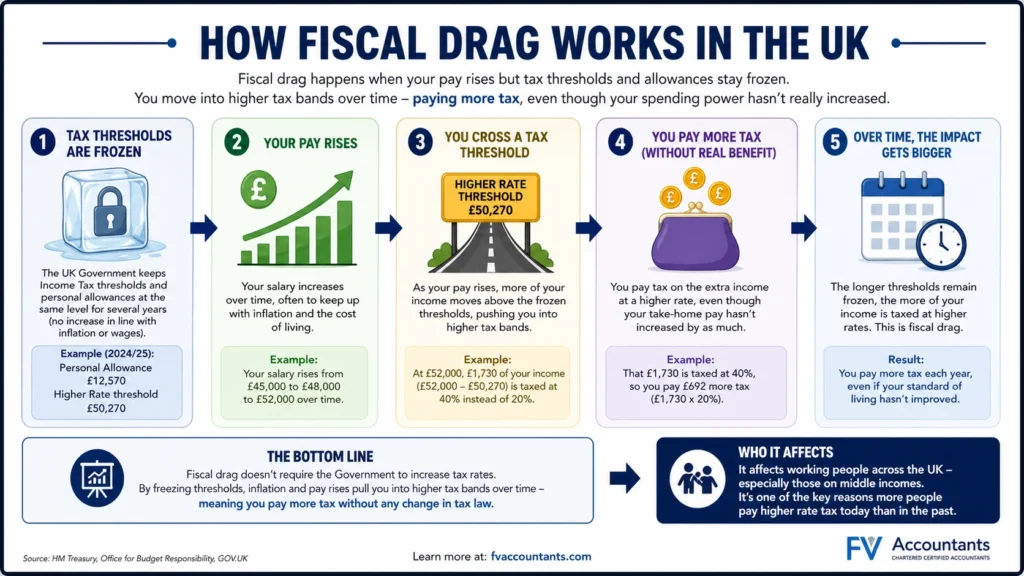

Fiscal drag results from the failure to adjust income tax thresholds in line with inflation and wage growth. When thresholds are frozen in nominal terms, rising incomes—whether from pay raises or inflation adjustments—push taxpayers into higher tax bands or diminish their entitlement to allowances, raising their effective tax rate. For example, from April 2023, the basic rate threshold remains at £50,270 while the additional rate threshold decreased to £125,140, triggering higher tax payments. This incremental tax rise happens even if real income (purchasing power) remains static or falls, which feels like a stealth tax increase.

For taxpayers earning between the personal allowance (£12,570) and £50,270, income above the personal allowance is taxed at 20%. Once income crosses £50,271, it is taxed at 40%, and above £125,140, at 45%. With thresholds frozen, someone earning £30,000 today could pay almost £2,000 more tax over five years purely due to fiscal drag. This phenomenon also pushes some workers inadvertently into paying National Insurance contributions sooner or at higher rates.

Tax Band Thresholds 2025/26 (England/Wales/Northern Ireland)

Tax Band | Income Range (£) | Tax Rate (%) |

Personal Allowance | 0 – 12,570 | 0 |

Basic Rate | 12,571 – 50,270 | 20 |

Higher Rate | 50,271 – 125,140 | 40 |

Additional Rate | 125,141+ | 45 |

Practical Implications and Nuances for Taxpayers

Fiscal drag impacts different taxpayers in complex ways. Those with multiple income sources—such as a salaried job plus self-employment or rental income—may face compounded fiscal drag due to aggregate income pushing them into higher tax liabilities. For business owners, income extracted from profits combined with personal income can lead to unexpected tax charges. Scottish and Welsh taxpayers have their own income tax bands and rates that differ from the rest of the UK, which compounds calculation complexity.

Another important nuance is the High Income Child Benefit Charge, affecting families where income exceeds £50,000. With fiscal drag pushing incomes higher, more families face clawbacks of child benefit, further increasing their tax bills without a rise in actual income. For self-employed individuals and gig economy workers, fluctuating income and irregular tax code adjustments can lead to overpayment or underpayment challenges, requiring diligent record-keeping and proactive annual tax reviews.

Scottish Income Tax Bands 2025/26

Tax Band | Income Range (£) | Tax Rate (%) |

Personal Allowance | 0 – 13,430 | 0 |

Starter Rate | 13,431 – 14,751 | 19 |

Basic Rate | 14,752 – 25,688 | 20 |

Intermediate Rate | 25,689 – 43,662 | 21 |

Higher Rate | 43,663 – 150,000 | 41 |

Top Rate | 150,001+ | 46 |

Fiscal Drag Explained

Why millions in the UK are paying more tax without earning more real income.

🔍 The Stealth Tax Mechanism

Fiscal drag is the ultimate "stealth tax." It occurs when the government fails to adjust income tax thresholds in line with inflation and wage growth.

Because thresholds like the Basic Rate (£50,270) have been frozen since April 2023, standard inflation adjustments or pay raises push taxpayers into higher tax bands. Your purchasing power might remain exactly the same, but you hand a larger percentage of your paycheck to HMRC.

📊 Tax Band Complexity & Regional Differences

The complexity of the UK tax system compounds the effects of fiscal drag. Scotland operates under a significantly different regime with more tax bands and higher marginal rates, meaning Scottish taxpayers experience drag at different income milestones. The chart below illustrates the varying marginal rates across different standard income brackets for the 2025/26 tax year.

⚠️ The High Income Child Benefit Trap

Families face a severe penalty known as the High Income Child Benefit Charge (HICBC). Raised in April 2024 to begin at £60,000, the benefit is aggressively clawed back at a rate of 1% for every £200 earned above this threshold. Once the highest earner hits £80,000, the benefit is entirely wiped out. As nominal wages rise, thousands of families are dragged into this clawback zone without feeling any richer.

How to Mitigate Fiscal Drag

Verify Your Code

Use your HMRC online personal tax account to check reported income and ensure your tax code is correct, avoiding accidental overpayments.

Maximise Allowances

Shield your money. Utilise ISAs and tax reliefs. Shifting income between spouses can help balance the load and keep you out of higher bands.

Boost Pensions

If you are nearing the £60k HICBC threshold, increasing pension contributions reduces your "adjusted net income," protecting your child benefit.

Seek Professional Advice

Complex cases—especially those with multiple income streams, self-employment, rental properties, or cross-border Scottish taxation—require expert tax planning to optimize liabilities.

How to Check, Calculate and Manage Fiscal Drag

Taxpayers can take several practical steps to understand and mitigate fiscal drag:

- Verify Tax Code and Income: Use the official HMRC online personal tax account to check income reported, tax codes, and payments. It helps spot errors or incorrect tax codes that might cause overpayment [gov.uk/personal-tax-account].

- Calculate Tax Liability: Use HMRC’s tax calculators for the 2025/26 tax year to estimate liability under current frozen thresholds. This includes calculating NICs and how multiple income sources combine [gov.uk/income-tax-rates].

- Consider Tax Planning: Maximise tax-free allowances by utilising ISAs, pensions, and tax reliefs. Shifting income where possible between spouses or into tax-efficient investments helps reduce taxable income.

- Review Child Benefit Charge Impact: Families near the £50,000 income mark should model child benefit clawback scenarios and consider pension contributions to reduce adjusted net income below thresholds.

- Seek Professional Advice: Complex cases involving self-employment, rental income, gig work, or cross-border taxation within the UK’s devolved system benefit from expert tax planning to optimise liabilities and refunds.

Original Case Study: The Self-Employed Business Owner

Consider Jane, a self-employed graphic designer earning a flat £48,000 in 2025/26 with an additional £5,000 rental income. Due to frozen thresholds, although her total income rises only slightly with inflation, Jane’s taxable income edge pushes her into the higher 40% band for part of her earnings. Over five years, Jane faces an additional £2,500 cumulative tax due to fiscal drag alone, reducing funds available for business reinvestment. By maximising pension contributions and reviewing allowable expenses, Jane optimises her taxable income, mitigating some impact of fiscal drag.

Fiscal Drag, Explained

Why millions of people in the UK are paying more income tax each year — even when their pay rise barely keeps up with inflation, and even though headline tax rates haven't moved.

Headline numbers for 2026/27

Fiscal drag occurs when tax thresholds stay the same in cash terms while wages rise. People pay tax on more of their income, and some are pulled into higher bands — without any change to the headline rates themselves. The freeze is now in place until April 2031.

What is fiscal drag, in plain English?

Each year HMRC normally uprates income-tax thresholds in line with inflation. When the government instead chooses to freeze them, wages keep rising while the tax bands don't move. The result: a larger share of every pay packet falls into a taxable band, and some people get pulled across a threshold into a higher band entirely.

Because the policy raises revenue without lifting any headline rate, it is widely described as a "stealth tax". The Office for Budget Responsibility (OBR) estimates that the income-tax threshold freeze will be raising more than £55 billion a year by 2030/31 once fully matured.

Who is affected?

Between 2022/23 and 2030/31 the OBR projects an extra 5.2 million people dragged into paying income tax for the first time, around 4.8 million more pulled into the 40% higher-rate band, and roughly 600,000 more into the 45% additional-rate band.

How big is the bill?

AJ Bell analysis of the 2025 Budget extension suggests someone earning around £47,000 today could pay roughly £1,292 more in income tax over the three extra years of freeze (2028–2031), as wage growth pushes them into the higher-rate band.

Why it matters now

The original freeze ran to April 2026, was extended to April 2028 in the 2022 Autumn Statement, and was extended again to April 2031 at the Autumn Budget 2025. That's nine consecutive tax years without an inflationary uplift to the personal allowance or higher-rate threshold.

Income-tax rates & bands · 2026/27

The personal allowance and main thresholds for 2026/27 are unchanged from 2025/26 across the whole UK. Scotland sets its own non-savings, non-dividend rates and bands.

| Band | Taxable income | Rate |

|---|---|---|

| Personal Allowance | Up to £12,570 | 0% |

| Basic rate | £12,571 – £50,270 | 20% |

| Higher rate | £50,271 – £125,140 | 40% |

| Additional rate | Over £125,140 | 45% |

| Band | Taxable income | Rate |

|---|---|---|

| Personal Allowance | Up to £12,570 | 0% |

| Starter rate | £12,571 – £16,537 | 19% |

| Basic rate | £16,538 – £29,526 | 20% |

| Intermediate rate | £29,527 – £43,662 | 21% |

| Higher rate | £43,663 – £75,000 | 42% |

| Advanced rate | £75,001 – £125,140 | 45% |

| Top rate | Over £125,140 | 48% |

The 60% trap between £100,000 and £125,140

The personal allowance is withdrawn by £1 for every £2 of income above £100,000, fully tapering away at £125,140. Combined with the 40% rate, this creates an effective marginal rate of 60% on every additional £1 in this band — a classic fiscal-drag pressure point that catches more people every year.

Where the threshold would be without the freeze

ICAEW analysis shows that if the personal allowance had been uprated with inflation, it would already sit at around £15,480 for 2025/26 — about £2,910 higher than its current level. The OBR estimates that by 2030/31, the personal allowance would be roughly £4,920 higher and the higher-rate threshold around £20,120 higher had inflation indexation continued.

Drag calculator

Enter your salary and an estimated annual pay rise. We'll compare what you'd pay if thresholds had been uprated by 3% a year (a rough inflation proxy) against the current frozen system. The difference is your fiscal-drag bill.

How the calculation works

The illustrative comparison uprates the personal allowance and higher-rate threshold by your chosen inflation proxy (default 3%) each year, and compares the resulting annual income-tax bill against today's frozen thresholds. NIC, dividend, savings and pension contributions are not modelled. For Scotland, all six bands above the personal allowance are uprated proportionately. Figures are rounded to the nearest pound.

What's changing — the next three tax years

Beyond the threshold freeze itself, several adjacent measures from the Autumn Budget 2025 (Finance Act 2026) compound the fiscal-drag effect on dividend, savings and property income.

Dividend tax rates rise by 2 percentage points

Ordinary rate up from 8.75% to 10.75% and upper rate up from 33.75% to 35.75%. The £500 dividend allowance is unchanged. The additional rate of 39.35% is also unchanged.

Savings & property income rates rise by 2pp

Across basic, higher and additional rates: 20%/40%/45% become 22%/42%/47% for savings interest and rental income. From the same date, the personal allowance must be allocated to earnings/pensions first, before savings or dividends.

Cash ISA limit reduced for under-65s

Maximum cash ISA subscription drops to £12,000 for those under age 65, though the overall £20,000 ISA limit is unchanged. Aimed at nudging savers toward Stocks & Shares ISAs.

High Value Council Tax Charge introduced

Properties valued at £2m – £2.5m face a £2,500 annual charge, rising on a sliding scale to £7,500 for properties valued over £5m.

Salary-sacrifice pension cap

Only the first £2,000 of employee pension contributions made via salary sacrifice will be exempt from National Insurance. Both employee and employer NICs become payable on amounts above the cap.

Income-tax threshold freeze ends

The personal allowance, higher-rate threshold, additional-rate threshold and aligned NIC thresholds are scheduled to be uprated again from 2031/32. By that point the OBR estimates the policy will have raised tens of billions and brought millions of additional individuals into higher tax bands.

A note on Scotland

The Scottish Parliament sets the rates and bands for non-savings, non-dividend income of Scottish taxpayers. For 2026/27 it raised the starter and basic-rate thresholds by 7.4% but left the higher, advanced and top thresholds frozen — so Scottish taxpayers above ~£43,663 are still exposed to fiscal drag through the higher, advanced and top bands.

Practical planning considerations

Fiscal drag isn't something individuals can stop, but its impact can often be softened with disciplined use of pre-tax allowances and reliefs. None of the below is personalised advice — speak to a qualified adviser before acting.

Pension contributions

Personal pension contributions reduce your "adjusted net income". This can pull income back below £100,000 (recovering the personal allowance and escaping the 60% taper), or back below £50,270 (avoiding higher-rate tax) for those on the cusp. The standard annual allowance is £60,000.

ISAs & the dividend allowance

All gains, interest and dividends inside an ISA are tax-free. With the dividend allowance at £500 and dividend rates rising 2pp from April 2026, sheltering dividend-paying assets in a Stocks & Shares ISA matters more each year. The £20,000 overall ISA limit is unchanged.

Marriage Allowance

If one spouse or civil partner has income below the personal allowance and the other is a basic-rate taxpayer, up to £1,260 of unused allowance can be transferred — worth up to £252 a year. Backdating up to four prior tax years is permitted.

Salary sacrifice — review before 2029

For higher earners, salary sacrifice into pensions has been a powerful way to reduce both income tax and NIC. From April 2029 a £2,000 cap on the NIC-free portion applies, so existing arrangements should be reviewed against the new ceiling.

Charitable giving (Gift Aid)

Higher- and additional-rate taxpayers can claim relief on the difference between their highest rate and the basic rate on Gift Aid donations. Like pension contributions, qualifying gifts reduce adjusted net income and can preserve the personal allowance.

EIS, SEIS and VCTs

Higher-risk investments such as the Enterprise Investment Scheme, Seed EIS and Venture Capital Trusts offer income-tax relief at 30% (or 50% for SEIS) on qualifying subscriptions. Suitability is highly individual — they are not appropriate for many investors.

Reporting and deadlines

Most employees pay income tax through PAYE. Self Assessment for 2025/26 must be filed online by 31 January 2027, with the balancing payment due the same date. From April 2026, Making Tax Digital for Income Tax applies to self-employed individuals and landlords with combined gross income above £50,000 — quarterly digital updates are required to HMRC.

Frequently asked questions

Common questions about how the freeze works and who it affects.

Why is fiscal drag called a "stealth tax"?

Because the government raises significant additional revenue without legislating any increase to the headline rates of income tax. Most taxpayers see no line item that says "your tax went up" — but a slowly larger share of their pay is taxed each year, and some cross thresholds into higher bands. The OBR currently estimates the threshold freeze will raise more than £55 billion a year by 2030/31 once fully matured.

Have rates of income tax actually gone up?

No. The 20% / 40% / 45% main rates have not changed for 2026/27. What has changed are some of the rates on investment income: dividend rates rise by 2pp from April 2026, and rates on savings and property income rise by 2pp from April 2027. These are separate measures that compound the effect of the threshold freeze for landlords, savers and shareholders.

How long are the thresholds frozen for?

The personal allowance was frozen from April 2022. The freeze was originally due to end in April 2026, was extended to April 2028 in the 2022 Autumn Statement, and was extended again to April 2031 at the Autumn Budget 2025 — putting nine consecutive tax years into the freeze. Provision for the latest extension is included in the Finance Act 2026.

Where would the personal allowance be without the freeze?

ICAEW estimates that, had it been uprated with inflation, the personal allowance would already have reached around £15,480 for 2025/26 — about £2,910 higher than its current £12,570. The OBR projects that by 2030/31 the personal allowance would be roughly £4,920 higher, and the higher-rate threshold around £20,120 higher, had inflation indexation continued throughout.

Does fiscal drag affect Scotland the same way?

The personal allowance is reserved to Westminster, so it is frozen for Scottish taxpayers as well. Scotland sets its own rates and bands above the personal allowance: for 2026/27 the Scottish Government raised the starter and basic-rate thresholds by 7.4%, but the higher (£43,663), advanced (£75,001) and top (£125,140) thresholds were left frozen — so middle and high earners in Scotland are still subject to drag through those bands.

Can I avoid being dragged into the higher-rate band?

You cannot opt out of the system, but you can reduce your taxable income. Pension contributions and Gift Aid donations reduce adjusted net income for tax purposes; salary sacrifice (within the new £2,000 NIC-free limit from April 2029) is one mechanism. Where appropriate, sheltering dividends, interest and capital gains inside ISAs avoids them adding to taxable income at all.

What is the "60% trap"?

For income between £100,000 and £125,140, the personal allowance is withdrawn at a rate of £1 for every £2 of additional income. Combined with the 40% higher rate, this creates an effective marginal rate of 60% on every additional £1 in this band. The £100,000 threshold itself is frozen, so wage growth pulls more people into this trap each year.

What does Making Tax Digital mean for me?

Making Tax Digital for Income Tax (MTD ITSA) is being phased in. From April 2026 it applies to self-employed individuals and landlords with combined gross income above £50,000; the threshold reduces to £30,000 from April 2027 and to £20,000 from April 2028. Affected taxpayers must keep digital records and submit quarterly updates to HMRC using compatible software.

Summary of Key Points for Taxpayers and Business Owners

- Fiscal drag increases income tax burden as frozen thresholds push incomes into higher bands.

- Current personal allowance (£12,570) and key tax bands frozen until 2028, intensifying fiscal drag impact.

- Additional rate threshold lowered to £125,140 in April 2023 affects high earners more.

- Multiple income sources compound fiscal drag effects.

- Scottish/Welsh taxpayers face a distinct, often more complex, band structure.

- High Income Child Benefit Charge affects more families due to frozen thresholds.

- HMRC online tools aid checking correct tax codes and calculating tax liabilities.

- Using tax planning methods like pension contributions and ISAs mitigates fiscal drag impact.

- Self-employed and business owners need advanced planning to handle mixed income sources and allowances.

- Professional tax advice is recommended for complicated situations to ensure compliance and optimize refund possibilities.

By understanding fiscal drag’s mechanics and impacts precisely, UK taxpayers and business owners can take actionable steps to monitor their tax position and plan effectively. Regular review of tax bands, tax code accuracy, and employing tax planning strategies enable managing invisible tax increases in this frozen-threshold environment

FAQs

Q1: What exactly does fiscal drag mean for someone on a fixed salary but experiencing rising living costs?

A1: Well, it’s worth noting that fiscal drag means your tax thresholds aren’t rising with inflation. So even if your salary feels squeezed by living costs, slowly more of your income ends up in higher tax bands. It’s like running on a treadmill that’s speeding up: you’re paying more tax without getting a real pay boost. This erodes your take-home pay unless you adjust your tax planning accordingly.

Q2: Can someone with more than one job be affected differently by fiscal drag?

A2: Absolutely. In my experience with clients who juggle multiple jobs, each job will have its own tax code and personal allowance slice, which can cause unexpected tax charges or underpayments. Combined income pushes you into higher tax bands, but checking and adjusting tax codes via HMRC can prevent errors. It’s key to declare all incomes properly to avoid surprises at tax year-end.

Q3: How does fiscal drag impact self-employed individuals differently from employees?

A3: Self-employed folks feel the pinch even more because their profits often fluctuate and they must manage payments on account. The frozen tax bands mean incremental profit growth could push them unexpectedly into higher tax brackets or reduce benefits. Regular cash flow planning and making pension contributions to reduce taxable profits can help smooth out the impact.

Q4: What should a Scottish taxpayer bear in mind regarding fiscal drag?

A4: Scottish income tax has its own bands and rates, making things a bit more complex. For example, the starter rate at 19% applies to low incomes, and the top rate hits 46% over £150,000. Fiscal drag here means that with frozen thresholds, more Scottish taxpayers face higher rates earlier than elsewhere in the UK. Always check your specific Scottish tax code and rates each year.

Q5: Could fiscal drag lead to overpaying tax, and how can someone spot this?

A5: Yes. It’s a common mix-up, but here’s the fix: overpayments often stem from outdated or incorrect tax codes or unreported income changes. Checking your PAYE details in your personal tax account online is the quickest way to catch discrepancies and apply for refunds. Keeping good records helps, especially if you have multiple income streams.

Q6: For families affected by the High Income Child Benefit Charge, how does fiscal drag worsen their tax bills?

A6: Families earning just above £50,000 start losing child benefit through this charge. Frozen thresholds mean inflation or small pay rises push more households into the charge zone. One client I advised used pension contributions to reduce income below the threshold, safeguarding benefits. It requires proactive income management to minimise clawback.

Q7: What’s the best first step to verify one’s income tax liability considering fiscal drag?

A7: Start by logging into your HMRC personal tax account and reviewing your tax code, income details, and payments. Using HMRC’s updated tax calculators for the 2025/26 year lets you estimate if you’re paying the right amount. It’s a hands-on way to catch errors quickly before the tax year closes.

Q8: How can business owners effectively manage fiscal drag when extracting income?

A8: Business owners should monitor drawings, dividends, and salary mix carefully, as frozen thresholds can push them into higher bands faster. Tax planning strategies—such as spreading income over tax years or increasing pension contributions—help smooth liabilities. Consulting a professional accountant ensures extraction is tax-efficient and compliant.

Q9: Is there any relief for taxpayers facing fiscal drag, or is it unavoidable?

A9: While fiscal drag itself is a form of stealth tax rise, taxpayers can reduce its effect through tax-efficient investments like ISAs or by utilising pension allowances. Also, keeping income just below key thresholds where possible and claiming all eligible reliefs can soften the blow. It’s about smart financial planning, not avoidance.

Q10: How can the gig economy workers check their tax payments considering fiscal drag?

A10: Gig workers often face irregular income, so combining PAYE and self-assessment tax can be tricky. The key is keeping detailed records and submitting accurate self-assessment returns on time. Using HMRC’s tools, they can monitor their tax codes and payments, avoiding surprises from fiscal drag pushing them into higher payment brackets mid-year.

Q11: What happens if someone underpays tax due to having multiple jobs under fiscal drag?

A11: Underpayment is common if tax codes don’t reflect total income properly across jobs. HMRC might collect this later through a tax bill or adjusted codes the next year. In my experience, voluntarily reviewing your tax codes and informing HMRC early prevents larger bills and penalties.

Q12: How are pension incomes affected by fiscal drag?

A12: Pensioners are not immune; rising state pensions and private pension withdrawals face frozen personal allowances and tax bands. This means more pension income can get taxed at higher rates over time. For retirees, managing withdrawals to keep income within allowances can reduce unnecessary tax.

Q13: Can you explain the VAT registration threshold’s impact related to fiscal drag for small businesses?

A13: The VAT threshold is another frozen threshold until recently, meaning more small businesses had to register and charge VAT without real turnover growth. This pressure squeezes margins on many micro-businesses and retailers. Keeping up with threshold changes and planning pricing accordingly can help manage this burden.

Q14: How should taxpayers handle tax refunds owed due to overpayment caused by fiscal drag?

A14: Once identified, most overpayments must be reclaimed via HMRC’s online portal or by contacting their helpline. It’s crucial to keep proof of income and tax paid, especially with multiple jobs or self-employment. Requests should be made promptly to avoid missing refund windows.

Q15: Is it possible to request a change in tax code if it doesn’t account for fiscal drag?

A15: Yes, taxpayers can apply for a code review anytime. If you spot your tax code is too high or too low due to unaccounted income changes or threshold freezes, request an update through HMRC’s service. This prevents over or underpayment across the year.

Disclaimer

The information provided in this article is for general guidance only and is not intended to constitute professional advice, tax advice, financial advice, legal advice, or any other form of regulated guidance. Although every effort has been made to ensure accuracy at the time of publication, Fair View Accounting Services, including its director, employees, contractors, writers, and content-creation team, accepts no responsibility for any loss, damage, penalty, or consequence arising from reliance on the information contained herein.

UK tax legislation changes frequently, and HMRC interpretations, thresholds, and rules may vary depending on the individual circumstances of each taxpayer. Nothing in this article should be considered a substitute for obtaining formal, personalised advice from a qualified accountant or tax professional. Readers should not take action—or refrain from taking action—based solely on the content published on this website.

Fair View Accounting Services does not guarantee the completeness, accuracy, or ongoing validity of the information provided and assumes no liability for omissions or errors, whether typographical, factual, or technical. By using this content, the reader acknowledges that all responsibility for decisions remains solely with the user.