Capital Gains Tax on Property Sales 2026

Overview of Capital Gains Tax on Property for 2025-26

What is Capital Gains Tax on Property?

Capital Gains Tax (CGT) is a tax on the profit (gain) made when selling or disposing of an asset that has increased in value. For UK residential property, CGT applies when selling second homes, buy-to-let properties, or any property other than your main residence.

- Main homes are generally exempt due to Private Residence Relief.

- Gains from buy-to-let or second homes are taxable if they exceed the annual CGT allowance.

Annual Allowance for 2025-26

- The annual CGT allowance for individuals in the tax year 2025-26 is £3,000.

- For couples jointly owning property, the allowance doubles to £6,000.

- This allowance is the amount of gain you can realise tax-free.

- Unused allowance cannot be carried forward to subsequent years.

CGT Rates for Property Sales

CGT rates for residential property sales depend on your taxable income:

Income Tax Band | CGT Rate on Residential Property Gains |

Basic Rate | 18% |

Higher/Additional Rate | 24% |

The CGT rate is applied on the gain after using the annual allowance and allowed deductions. Importantly, the capital gain is added on top of your other taxable income to determine the rate band applicable.

Calculating Capital Gains Tax on Property Sales

Step-by-Step Calculation

- Determine the Gain on Sale

Gain = Sale Price – Purchase Price – Allowable Costs

Allowable costs include:

- Purchase price (including solicitor fees)

- Costs of improvement (not repairs)

- Selling costs (estate agent fees, solicitor fees).

- Apply Annual Allowance

Deduct the £3,000 allowance (or £6,000 for couples). - Determine taxable gain

Any amount above the allowance is taxable. - Add Gain to Income to Determine Tax Band

Combined taxable income + gain determines if gain is taxed at 18% or 24%. - Calculate CGT Owed

Practical Calculation Example:

- Property bought for £200,000 (with £5,000 in allowable improvements).

- Sold for £350,000.

- Selling costs: £10,000.

- Other taxable income for the year: £45,000 (basic rate band).

Step 1: Gain = £350,000 – (£200,000 + £5,000 + £10,000) = £135,000

Step 2: Deduct allowance: £135,000 – £3,000 = £132,000 taxable gain

Step 3: Basic rate band limit is £50,270 for 2025/26 (assuming personal allowance has been used).

Combined income + gain = £45,000 + £132,000 = £177,000.

£50,270 – £45,000 = £5,270 taxed at 18%.

Remaining gain: £132,000 – £5,270 = £126,730 taxed at 24%.

CGT = (5,270 × 18%) + (126,730 × 24%) = £948.60 + £30,415.20 = £31,363.80 tax owed.

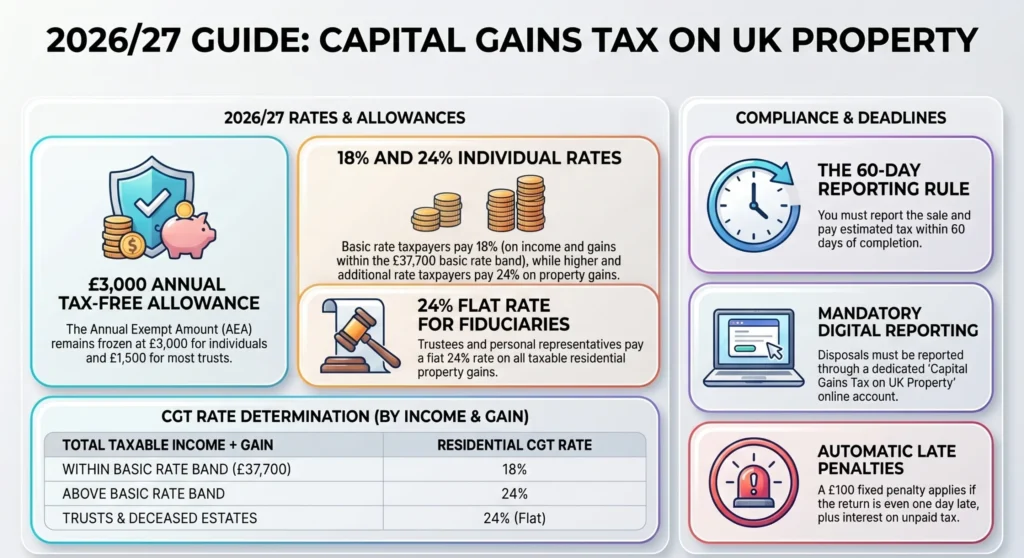

60-Day Reporting Rule

- Taxpayers must report and pay CGT for UK residential property within 60 days from the completion date of the sale.

- Failure to comply leads to penalties and interest.

- Reporting is done via the UK property Capital Gains Tax return on HMRC’s online portal.

Filing a Self-Assessment Tax Return

- Even if the 60-day return is filed, a self-assessment tax return may still be required depending on your tax circumstances.

- Reporting obligations also apply to non-residents disposing UK property.

Capital Gains Tax on Property Sales

A comprehensive guide to understanding your CGT liabilities, allowances, and reporting requirements for UK residential property sales in the 2025-27 tax years.

The Core Metrics

The government has frozen the annual allowance, meaning more of your property profit is subject to tax. Below are the critical numbers for second home or buy-to-let owners.

Annual Allowance

Individual allowance frozen for 2025-27.

Basic Rate

Applied within your basic income tax band.

Higher Rate

Applied to gains above the £50,270 threshold.

Deadline

Timeframe to report and pay HMRC post-sale.

Tax Rates by Income Band

CGT is added on top of your regular income. If your combined earnings stay below £50,270, you pay the basic rate. Anything above that is taxed at the higher rate.

The Calculation Flow

Deducting allowable costs accurately is the most effective way to minimize your final tax bill.

Example: £150k Gain

In this scenario, after a £135,000 gain and a £3,000 allowance, the majority of the profit is taxed at the higher 24% rate due to existing salary income.

Action Checklist

Docs

Gather solicitor statements and purchase records.

Improve

Log capital improvements like extensions or new kitchens.

PRR

Check main residence relief dates if you lived there.

HMRC

Set up your Gateway ID for the 60-day filing.

Private Residence Relief (PRR)

- Exempts your main home from CGT.

- Partial relief may apply if part of the property was rented out.

- Last 9 months of ownership counted as if the property was your main residence to extend relief.

Spousal Transfers

- Transfers between spouses and civil partners are exempt from CGT.

- Allows usage of both allowances by transferring property ownership share.

Other Reliefs

- Letting Relief, mainly abolished but may apply in limited cases.

- Relief in case of gifting property to charity (exempt).

- Relief if property was occupied by a dependent relative (consult an adviser).

Multiple Income Sources and Tax Bands

- CGT must be calculated considering all sources of income.

- Gains may push taxpayers into higher income tax bands, increasing CGT rate.

- Important for self-employed or gig economy workers who may have fluctuating income.

Scottish and Welsh Variations

- Scotland and Wales have different income tax rates but CGT for property follows UK-wide rules (18%/24%).

- However, Income Tax band thresholds differ, affecting the CGT rate applied.

High-Income Child Benefit Charge Interaction

- For high earners subject to the High Income Child Benefit Charge, additional tax liability may arise.

- CGT gains can push taxpayers into the charge threshold.

Before Selling Property

- Confirm property qualifies as your main residence for PRR.

- Gather all cost receipts for purchase and improvements.

- Check if you can transfer ownership to spouse before sale.

- Calculate anticipated gain considering 2025/26 allowance.

When Reporting

- Submit property disposal report within 60 days on HMRC portal.

- Retain all documentation for calculations and relief claims.

- File self-assessment return if required.

Ways to Reduce CGT

- Time sale in a lower-income year.

- Use both spouses’ CGT allowances.

- Deduct allowable costs and improvements accurately.

- Consider gifting to spouse or charity where appropriate.

Tables for Clarity

Table 1: 2025-26 CGT Allowance and Rates

Detail | Amount |

Annual CGT Allowance | £3,000 per person |

Combined Allowance | £6,000 for couples |

Basic Rate CGT on Property | 18% |

Higher/Additional Rate CGT on Property | 24% |

Reporting Deadline | 60 days from sale |

Table 2: Income Tax Bands vs CGT Implications (2025-26)

Income Category | Threshold | CGT Rate on Property Gain |

Personal Allowance | £12,570 | 0% (Income Tax only) |

Basic Rate Income Band | £12,571 to £50,270 | 18% |

Higher Rate Income Band | £50,271 to £125,140 | 24% |

Additional Rate (over £125,140) | Above £125,140 | 24% |

Capital Gains Tax on Property Sales

An interactive guide to UK CGT on residential property — current rates, an instant calculator, the rules that apply now, and the changes coming in April 2026 and April 2027.

Headline numbers for 2026/27

CGT rates on residential property

When does CGT apply?

| Type of property | CGT typically due? |

|---|---|

| Your only or main home (continuously) | No — Private Residence Relief |

| Buy-to-let / rental property | Yes |

| Second home or holiday home | Yes |

| Inherited property (when you sell) | Yes — gain measured from probate value |

| Property gifted to spouse / civil partner | No (no gain / no loss) |

| Property gifted to anyone else | Yes — at market value |

Estimate your CGT on a property sale

Enter your figures below. Calculations use 2026/27 rates & thresholds (basic-rate band £12,571–£50,270, allowance £3,000). Results update instantly as you type.

How the gain is calculated

What you can deduct

Key reliefs

Reporting & payment

The CGT & landlord tax timeline

Property CGT rates themselves are unchanged for 2026/27, but the wider tax burden on property owners is rising. Here's what's confirmed in the Autumn Budget 2025 and Finance Act 2026.

Legitimate ways to reduce your CGT bill

Summary of Key Points

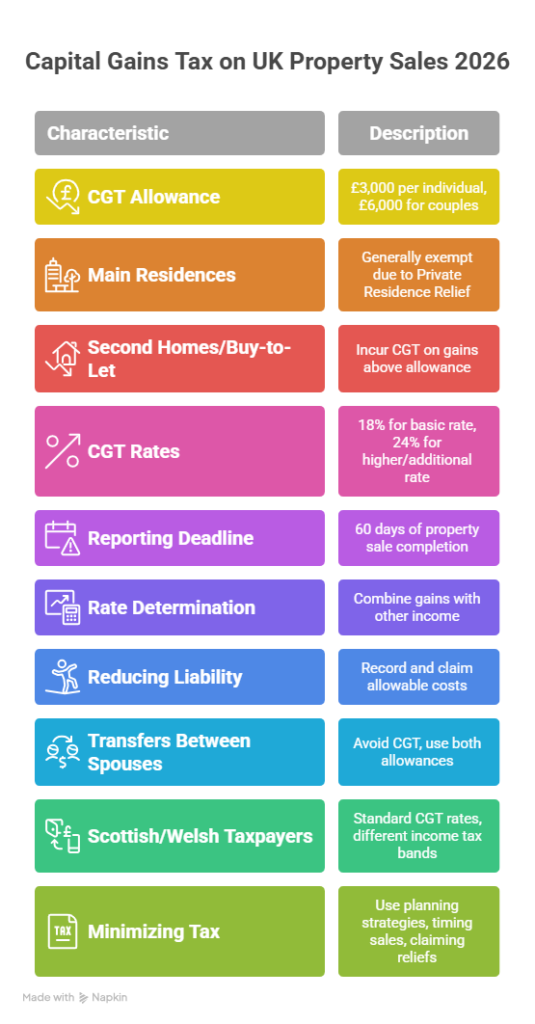

- The CGT allowance for 2025/26 is £3,000 per individual, £6,000 for couples.

- Main residences are generally exempt from CGT due to Private Residence Relief.

- Second homes and buy-to-let properties incur CGT on gains above allowance.

- CGT rates are 18% for basic rate taxpayers and 24% for higher/additional rate taxpayers.

- Gains must be reported and tax paid within 60 days of property sale completion.

- Combining gains with other income is necessary to establish CGT rate.

- Recording and claiming allowable costs reduces your CGT liability.

- Transfers between spouses avoid CGT and allow use of both allowances.

- Scottish and Welsh taxpayers face standard CGT rates but different income tax bands affect the rate applied.

- Use planning strategies such as timing sales and claiming reliefs to minimize tax due.

This comprehensive insight provides UK taxpayers and property owners with practical knowledge, actionable checklists, and detailed calculations to manage CGT liabilities effectively for the 2025-26 tax year.

FAQs

Q1: Can someone change their tax code if it’s incorrect when calculating Capital Gains Tax on property sales?

A1: Well, it’s worth noting that CGT on property sales isn’t handled through your tax code like PAYE income tax is. Instead, you report gains and pay CGT separately via the HMRC portal or your self-assessment return. So, an incorrect tax code won’t affect your CGT liability directly, but if you notice discrepancies in your PAYE code that impact your overall income tax band, correcting it could affect the CGT rate you pay on the gain.

Q2: How does having multiple jobs affect the CGT rate on property sales?

A2: In my experience with clients juggling multiple jobs, the key is remembering that your total taxable income (from all jobs) plus your capital gain determines your CGT rate. More income means you’re more likely to pay the higher 24% CGT rate instead of 18%. So double-check all your earnings before calculating CGT to avoid surprises.

Q3: Could a self-employed person in the gig economy face any particular pitfalls with CGT on property sales?

A3: Absolutely. For freelancers or gig economy workers, fluctuating incomes make predicting your CGT rate tricky. Let’s say a contractor in Leeds sells a buy-to-let; a good tip is to estimate your total income including the gain for that tax year to know if you cross the higher rate threshold. Also, keep solid records of all allowable costs to reduce your taxable gain.

Q4: Are there any specific CGT differences for Scottish or Welsh taxpayers on property sales?

A4: It’s a common mix-up, but CGT rates on residential property are UK-wide — 18% for basic rate taxpayers, 24% for higher. However, because income tax bands differ in Scotland and Wales, this affects where your income plus the gain falls in the tax brackets, indirectly influencing your CGT rate. So, always verify your regional income tax bands alongside CGT.

Q5: What happens if a landlord didn’t report a property sale within the 60-day deadline?

A5: Missing the 60-day deadline to report UK residential property sales can lead to penalties and interest. In practice, I advise landlords to file promptly since the penalties start small but grow over time. If you’re late, file as soon as possible and be prepared to explain any genuine reasons for delay to HMRC.

Q6: How can a homeowner with shared ownership reduce CGT on property sales?

A6: For shared ownership, each owner gets their £3,000 annual allowance, doubling it effectively if the property is jointly owned. However, it’s essential to split the gain correctly according to ownership percentages. Also, transferring ownership between spouses before selling can help utilise both allowances fully.

Q7: Is it ever beneficial to gift a property to a spouse before selling to save on CGT?

A7: It can be. Transfers between spouses are CGT-free, which lets you shift the property to utilise both CGT allowances and potentially lower rates. For example, a business owner might gift half the buy-to-let to their spouse, then both sell shares to reduce overall CGT outlay, a strategy I’ve used successfully with married clients.

Q8: Can mixing personal use and rental periods affect CGT liabilities?

A8: Yes, this often trips up many property owners. If your main home was rented out for a period, you might only get partial Private Residence Relief, reducing exempt gain. This means CGT is payable on the gain related to the rental period, so accurate records of dates and usage are crucial.

Q9: How do improvements vs. repairs impact CGT calculation for property sales?

A9: It’s a subtle but vital distinction. Only capital improvements (like extensions or new kitchens) add to your property’s base cost for CGT purposes. Routine repairs or maintenance costs don’t reduce your gain. So, keep invoices sorted and label work carefully.

Q10: What are the chances of HMRC challenging the valuation if a property is sold to a connected party?

A10: Quite high. HMRC expects sales between connected parties to be at market value. If HMRC suspects undervaluation, they may request independent valuation reports or reassess your gain, which can lead to disputes and penalties. Being prepared with professional valuations is a smart safeguard.

Q11: Do pension contributions or withdrawals affect CGT on property sales?

A11: While pension contributions don’t impact CGT directly, higher pension withdrawals can increase your taxable income, potentially pushing you into the higher CGT bracket at 24%. So, if you’re planning a large withdrawal alongside a property sale, it’s wise to plan timing carefully.

Q12: Can an individual with multiple properties sell some without paying CGT?

A12: It depends. Your main residence is generally exempt due to Private Residence Relief. Any extra properties like buy-to-lets or holiday homes will be subject to CGT on gains above the allowance. Strategic timing and using reliefs or exemptions on one property might help.

Q13: How does non-resident CGT reporting differ with multiple UK property sales?

A13: Non-residents must report every UK property disposal within 60 days of completion, even if no CGT is due. This strict reporting ensures HMRC tracks gains accurately. If selling multiple properties in one year, report each separately and keep impeccable records.

Q14: Are there any risks of CGT overpayment if income changes unexpectedly after property sale?

A14: Yes, this happens often with fluctuating incomes — you may calculate CGT assuming a higher tax band than your final income justifies. You can ask HMRC to adjust this via self-assessment amendments or claim a repayment. It’s worth double-checking your final income before submitting.

Q15: If someone receives a family inheritance of property, when does CGT kick in?

A15: Good question. No CGT is due at inheritance. The base cost for CGT is the property value at the date of death. CGT is payable when you later sell the property, with gain measured from the inherited value to the sale price. Careful valuation at inheritance is important.

Q16: What should a PAYE employee check to ensure correct CGT calculations alongside salary?

A16: Employees should check their tax code is correct to ensure income tax bands are properly applied. Since CGT rate depends on combined income, you’ll want your PAYE income accurately reflected so your CGT computation corresponds to your real income level.

Q17: How does the High-Income Child Benefit Charge influence CGT tax planning?

A17: Gains can push your income over £50,000, triggering the high-income child benefit charge, reducing or removing child benefit payments. For business owners with children, this is a subtle trap — planning sales timing or spreading gains over different tax years may help.

Q18: What’s the impact of part-exchanging property on CGT?

A18: Part-exchange means swapping part cash and part another property. For CGT, you calculate gain based on the total value you receive (cash + value of the property received). It complicates calculations, so getting valuations and advice is crucial.

Q19: Can business owners offset CGT from property sales against trading losses?

A19: Unfortunately, no. Trading losses offset income tax, but CGT computations are separate. However, planning to use trading losses in a year with a big capital gain could free up more cash for CGT payments.

Q20: Is it advisable to seek professional valuations for all properties sold?

A20: In my 15+ years advising clients, I always recommend professional valuations, especially for connected-party sales or where the market value is unclear. This protects you from HMRC challenges and supports accurate CGT reporting.

Disclaimer

The information provided in this article is for general guidance only and is not intended to constitute professional advice, tax advice, financial advice, legal advice, or any other form of regulated guidance. Although every effort has been made to ensure accuracy at the time of publication, Fair View Accounting Services, including its director, employees, contractors, writers, and content-creation team, accepts no responsibility for any loss, damage, penalty, or consequence arising from reliance on the information contained herein.

UK tax legislation changes frequently, and HMRC interpretations, thresholds, and rules may vary depending on the individual circumstances of each taxpayer. Nothing in this article should be considered a substitute for obtaining formal, personalised advice from a qualified accountant or tax professional. Readers should not take action—or refrain from taking action—based solely on the content published on this website.

Fair View Accounting Services does not guarantee the completeness, accuracy, or ongoing validity of the information provided and assumes no liability for omissions or errors, whether typographical, factual, or technical. By using this content, the reader acknowledges that all responsibility for decisions remains solely with the user.