Understanding Frozen Income Tax Thresholds in the UK: HMRC Warnings on Fiscal Drag and Stealth Taxes for 2026/27

The Reality of Frozen Income Tax Thresholds

The Illusion of a Pay Rise

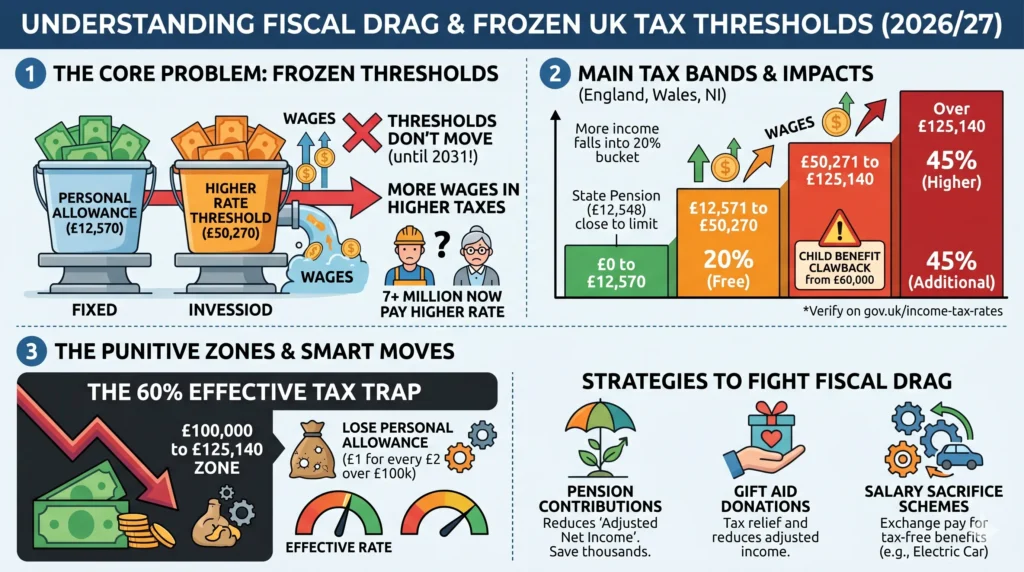

Imagine getting a decent pay rise this year, popping the kettle on to celebrate, only to realise months later that a chunk of it has vanished into higher tax – not because rates went up, but because the goalposts never moved. That’s the reality for millions right now, thanks to frozen income tax thresholds. For the 2026/27 tax year (6 April 2026 to 5 April 2027), the personal allowance stays locked at £12,570, meaning there is no tax on the first slice of your income up to that point. The basic rate limit remains £37,700, which means the higher-rate threshold (where 40% tax kicks in) is still pinned at £50,270 for England, Wales, and Northern Ireland. These figures haven’t budged since 2021/22 and, following the extension introduced at Budget 2025, are set to stay frozen until April 2031 – a stealth policy maintained across successive governments to quietly bolster Treasury revenues.

The Mechanics of Fiscal Drag

This isn’t a new headline-grabbing rate hike; it’s what’s known as fiscal drag or a “stealth tax”. As wages creep up with inflation or cost-of-living adjustments, more of your earnings spill into higher taxable bands. Recent HMRC figures highlight that over 39 million people are caught in the income tax net, with a record 7.08 million taxpayers pushed into the higher-rate bracket. Pensioners are feeling the squeeze acutely this tax year: the full new state pension has risen to £12,548 a year, leaving it sitting less than £30 away from the £12,570 personal allowance. This means any small private pension or part-time earnings will instantly drag millions of retirees into paying tax for the first time. (You can check the baseline data on liabilities at gov.uk: https://www.gov.uk/government/statistics/income-tax-liabilities-statistics-tax-year-2022-to-2023-to-tax-year-2025-to-2026).

The Hidden Impact of Threshold Stagnation

The Kitchen Cupboard Analogy

Think of your tax bands like shelves in a cupboard – if you keep adding more groceries (rising wages) but never raise the shelves (thresholds), everything starts overflowing into the pricier section. HMRC doesn’t send a dramatic warning letter about this, but the effect on your bank balance is very real. Average earners see less benefit from cost-of-living pay rises, and middle-income professionals like teachers, nurses, or mid-level managers suddenly find themselves designated as “higher-rate taxpayers” without feeling a penny wealthier.

The UK Tax Trap Guide 2026/27

A visual breakdown of frozen thresholds, fiscal drag, and how to protect your wealth in May 2026.

The 2026/27 Income Tax Bands

£12,570

0% Tax Rate

Frozen since 2021

Up to £50,270

20% Tax Rate

Personal Savings: £1k

£50,271+

40% Tax Rate

Savings allowance drops to £500

£125,140+

45% Tax Rate

PA completely removed

Interactive Trap Escape Calculator

Includes salary, bonuses, rental profit & dividends.

This lowers your "Adjusted Net Income".

Live Analysis

The Fiscal Drag "Cliff Edges"

£50,270: The Higher-Rate Threshold

Every pound over this line is taxed at 40%. Plus, your tax-free savings interest allowance is slashed from £1,000 to £500.

"I've seen nurses and mid-level managers hit this wall just from cost-of-living pay rises."

£60,000 - £80,000: The Child Benefit Clawback

The High Income Child Benefit Charge begins. You lose 1% of your benefit for every £200 over £60k. At £80k, it's gone entirely.

Official GOV.UK Guidance →£100,000 - £125,140: The 60% Trap

Your Personal Allowance disappears (£1 lost for every £2 earned). Combined with 40% tax, the effective hit is 60%.

TAX BLACK HOLE ZONE: Minimize Adjusted Income here!

Accountant-Approved Escape Strategies

Pension Contributions

The "Nuclear Option". Lower your income below £100k or £60k to reclaim allowances and benefits instantly.

Gift Aid Donations

Reduces your taxable income pound-for-pound while supporting a cause. Costs a higher-rate payer only £60 for every £100 donated.

Salary Sacrifice

Cycle-to-work or electric car schemes reduce gross income, bypassing tax, NI, and threshold traps simultaneously.

Dividend Timing

With rates at 10.75%/35.75%, time your withdrawals to utilize the (small) £500 allowance effectively.

The 2026/27 Tax Year Framework

Tax Bands for England, Wales, and Northern Ireland

Here’s the structure straight from the official guidelines: ● £0 to £12,570: 0% (Personal Allowance – tax-free) ● £12,571 to £50,270: 20% (Basic rate on the next £37,700) ● £50,271 to £125,140: 40% (Higher rate) ● Over £125,140: 45% (Additional rate) (Verify your specific position at: https://www.gov.uk/income-tax-rates)

The Scale of Affected Taxpayers

I’ve seen clients stare at their payslips in utter disbelief when a modest pay rise pushes them over £50,270. Suddenly, they face a 40% tax hit on that extra portion, plus clawbacks on family perks like Child Benefit eligibility. The Office for Budget Responsibility (OBR) estimates that this compounding fiscal drag is raking in tens of billions in extra revenue for the government without them ever having to announce a direct rate change.

Cross-Border Variations in Scotland

If you’re north of the border, income tax bands are devolved and determined by Holyrood. While they are adjusted differently—with multiple bands including a 19% starter, 20% basic, 21% intermediate, 42% higher, 45% advanced, and a 48% top rate—the pressure of wage growth against frozen or tightly squeezed lower thresholds means Scottish taxpayers are feeling the pinch just as intensely.

The Higher-Rate Threshold Trap

A Real-World Case of the 40% Cliff Edge

Picture Sarah, a project manager in Manchester earning £48,000. She gets a well-deserved 5% raise – lovely, an extra £2,400 on paper. But because the higher-rate threshold is frozen at £50,270, that bump tips her over the edge. Suddenly, the top slice of her income is taxed at 40% instead of 20%, and she faces the clawback of her household’s Child Benefit. “It felt like HMRC just nicked half my raise,” she told me during our annual review. Stories like Sarah’s are standard practice now, a direct result of fiscal drag pulling everyday professionals into the higher-rate net.

What Triggers the 40% Tax Hit?

Once your total income (combining salary, bonuses, taxable benefits, and rental profits) exceeds £50,270, every pound above that line is taxed at 40%. It’s important to remember it’s not your whole salary being hit, just the portion over the threshold. However, with the limit unmoved for years, standard cost-of-living adjustments are doing the damage. We now have over 7 million people paying the higher rate—meaning senior nurses, police sergeants, and mid-level engineers are routinely handing over 40% on their overtime or hard-earned promotions.

The High Income Child Benefit Charge Impact

If the highest earner in your household exceeds £60,000 in adjusted net income, the High Income Child Benefit Charge (HICBC) kicks in. The benefit is clawed back at a rate of 1% for every £200 of income over this £60,000 limit, meaning it is wiped out entirely once you hit £80,000. To simplify administration, HMRC’s digital service allows employed parents to pay this charge directly through their PAYE tax code rather than filing a full Self Assessment return (see details at: https://www.gov.uk/child-benefit-tax-charge). Even with these administrative tweaks, because the threshold has remained flat since its recent adjustment, thousands of families who previously felt comfortable are finding themselves ensnared.

Squeezing Savings and Dividend Income Streams

Your Personal Savings Allowance gives you £1,000 of tax-free interest if you’re a basic-rate taxpayer, but this drops sharply to £500 the moment you cross into the higher-rate bracket. Crossing that £50,270 line means you lose half your savings allowance overnight. Dividends bring an even sharper sting this year. While the tax-free dividend allowance remains at a tiny £500, the actual dividend tax rates have increased by 2% across the board for the 2026/27 tax year. Basic-rate taxpayers now pay 10.75% and higher-rate taxpayers pay 35.75% on dividend income above the allowance. This double-whammy of a frozen threshold and a higher tax rate makes profit extraction for business owners a delicate balancing act.

Assessing Your Personal Exposure

Take a moment to map out your own numbers using this quick “Am I Near the Edge?” checklist I give clients: ● Is your total expected income (salary, bonuses, dividends, and rental profits) creeping close to £50,000 or £100,000? ● Is Child Benefit being claimed by anyone in your household? ● Is your cash savings interest likely to breach the £500 or £1,000 tax-free limits? ● Are you a Scottish resident? (The bands are completely separate – check gov.uk/scottish-income-tax)

The Cost of Ignoring Threshold Boundaries

If you have ticked two or more of these boxes, you are likely already exposed to fiscal drag. One client of mine, a father of three earning £62,000, came to my office deeply worried after receiving an HMRC calculation for an unpaid HICBC bill. He had completely overlooked the fact that his recent promotion crossed the £60,000 threshold. We brought his affairs up to date, but the takeaway is clear: these frozen numbers have a tangible impact on real family budgets. However, the most punishing trap isn’t at £50,000—it’s the infamous six-figure zone where the tax system becomes genuinely severe.

The frozen thresholds quietly moving you up the tax ladder.

For 6 April 2026 – 5 April 2027, income tax rates didn't go up — but the bands didn't move either. The 2025 Autumn Budget extended the freeze through to April 2031, pulling millions more earners into higher bands as wages drift upward. Use the tools below to see exactly where you sit, where the traps are, and how to step clear of them.

Where does your income land?

Drag the slider (or type) to see your income broken down across the official 2026/27 tax bands. Toggle between England / Wales / Northern Ireland and Scotland — the bands are different north of the border.

Bars are proportional to your income falling in each band. Rates shown apply only to the slice in that band — not your entire salary.

The £100,000 trap — a hidden 60% band that isn't on the rate card

marginal hit 60%

How the trap works

Between £100,000 and £125,140 of adjusted net income, HMRC withdraws your £12,570 Personal Allowance at £1 for every £2 earned. That phantom income gets taxed at 40% on top of the actual 40% you're already paying — producing an effective 60% rate on the slice above £100k.

On a £15,000 bonus that takes you from £100k to £115k, you'd expect to keep around £8,500. In practice the trap can leave you with closer to £6,000. That's before the 2% employee National Insurance contribution on top.

When the trap stings the most

- A one-off bonus that pushes total income through £100,000

- A large dividend taken from a personal company

- A property sale or chargeable event that bumps adjusted net income

- A salary rise crossing the line for the first time

Child Benefit clawback — the £60k–£80k taper

If the highest earner in your household has adjusted net income above £60,000, the High Income Child Benefit Charge (HICBC) starts pulling back the benefit at 1% for every £200 over the threshold. It's gone entirely at £80,000.

HMRC's digital service now lets employed parents pay the charge through their PAYE tax code rather than filing Self Assessment. Reducing adjusted net income via pension or Gift Aid — even by £1,000 — can claw back a meaningful slice of benefit.

Dividend tax just went up 2 percentage points

The Autumn 2025 Budget raised the ordinary and upper dividend rates from 6 April 2026. Confirmed at gov.uk — the additional rate is unchanged. The £500 dividend allowance has not moved.

Roughly £20 more tax per £1,000 of dividends above the £500 allowance.

Director-shareholders feel this most. £40k of dividends in this band = ~£790 extra tax.

Held flat. The 2-point lift is loaded onto basic and higher rate dividend income only.

Source: HMRC tax information & impact note, Income Tax: Changes to Tax rates for Property, Savings and Dividend Income, gov.uk (Nov 2025).

What's still coming down the pipe

Confirmed timeline

Basic 10.75% · Higher 35.75% · Additional 39.35% (held).

Savings: 20% → 22% · 40% → 42% · 45% → 47%.

Property: separate rates of 22% / 42% / 47% applied to rental income.

HMRC will apply the £12,570 to earned income first. Landlords, investors and people with multiple income streams will see more savings, dividends and rent become taxable.

The Autumn 2025 Budget extended the freeze on the Personal Allowance and higher-rate threshold by a further three years. Both are scheduled to remain at £12,570 and £50,270 until this point.

The cumulative bite of fiscal drag

The freeze is doing the heavy lifting silently. According to House of Commons Library briefings, the 2026/27 income tax bands are unchanged from 2021/22 levels — meaning roughly five years of wage growth has now been quietly absorbed into higher tax bands.

- Higher-rate taxpayers now exceed 7 million in the UK.

- The full new State Pension (~£12,548) sits less than £30 below the Personal Allowance, drawing pensioners into tax for the first time on tiny additional income.

- The dividend allowance is just £500 — down from £5,000 a decade ago.

Stepping over the traps — legitimate reliefs to know

Each of these reduces your adjusted net income — the figure HMRC uses to assess the Personal Allowance taper, HICBC and marriage allowance eligibility.

The Trap Escape calculator

Estimate how much tax a pension or Gift Aid contribution could save you in the £100k–£125,140 zone (the 60% trap) or above the £60k HICBC threshold.

Indicative figures only — based on 2026/27 rates and bands. Speak to a qualified adviser before acting; results depend on contribution method (relief-at-source vs net pay vs salary sacrifice) and full personal circumstances.

Common multi-income questions

I have two PAYE jobs — will I be undertaxed if my combined income crosses £50,270?

Can I split my Personal Allowance across two jobs instead of using BR on the second?

Does rental income count towards the £50,270 higher-rate threshold?

I'm a Scottish resident with a remote job for an English employer — which bands apply?

I'm a director paying myself low salary and high dividends. How do the 2026/27 rates affect me?

Does a company car push me into the 60% zone?

I'm self-employed with a £1,000 trading allowance — does it still help if my total income is over £50k?

What happens if a one-off settlement payment pushes me over a threshold for one year?

The Infamous 60% Effective Tax Zone

Inside the Six-Figure Tax Black Hole

Ah, the £100,000 to £125,140 bracket—I have had many clients over the years refer to this as “the tax black hole.” If your adjusted net income lands in this zone, your Personal Allowance begins to taper away. For every £2 you earn over £100,000, you lose £1 of your £12,570 tax-free allowance. By the time you reach £125,140, your Personal Allowance is entirely gone. When you couple the 40% income tax rate with the clawback of your allowance, it creates an effective marginal tax rate of 60% on this specific slice of earnings (and that is before you factor in the 2% employee National Insurance contribution). It isn’t an official tax bracket listed on paper, but the mathematics are real, and they are brutal.

The Mathematical Mechanics of the Phased Withdrawal

Let’s look at the basic math: Start at £100,000 with a full £12,570 allowance. Earn £110,000 and you lose £5,000 of your allowance. That extra £5,000 is now exposed to 40% tax, creating an additional £2,000 liability on top of the standard 40% on the pay rise itself. Total effective hit: 60% (£6,000 tax) on that £10,000 slice. HMRC applies this taper strictly across the board, regardless of your age or birth date (the complete legislative guidance can be reviewed at: https://www.gov.uk/income-tax-rates/personal-allowance-if-income-over-100000).

Sacrificing Weekends to Feed the Treasury

Mark, a senior director based in Leeds, was awarded a £15,000 performance bonus that pushed his total income to £118,000. He naturally expected to take home around £8,500 of it. The reality came as a shock: he kept barely £6,000 after the 60% trap ran its course. “I gave up my weekends for months to hit those targets,” he told me. “It felt like I was working purely to donate to the Treasury.”

Strategic Wealth Protection Options

Lowering Your Adjusted Net Income Safely

The core strategy here is straightforward: you need to actively manage and lower your “adjusted net income” (your gross taxable income minus allowable deductions like pension contributions and charitable donations) back below the key thresholds.

Maximising Retirement and Pension Allocations

Pension contributions remain the ultimate planning tool. Putting £10,000 into your pension reduces your adjusted net income by exactly £10,000, which can restore up to £5,000 of your lost Personal Allowance. Higher earners receive tax relief at 40% or 45%, and utilising a workplace salary sacrifice scheme adds to the savings by cutting your employee National Insurance contributions too.

Utilising Charitable Donations and Corporate Sacrifices

Every £100 you donate to charity via Gift Aid only costs a higher-rate taxpayer £60 out of pocket, while simultaneously dragging your adjusted net income down. Similarly, entering into an employer-backed electric car scheme or a cycle-to-work initiative allows you to exchange gross salary for tax-free benefits, keeping your taxable total down. Investing via Venture Capital Trusts (VCTs) or Enterprise Investment Schemes (EIS) offers an upfront 30% income tax relief, though these carry a higher risk profile and should be assessed carefully.

Your Step-by-Step Numerical Breakdown

Take a moment to map out your own numbers using this unique “Trap Escape” Calculator worksheet (not found in standard articles): ● Current projected income: £______

● Minus planned pension contributions or Gift Aid: £______

● Your new projected adjusted net income: £______

● Strategic Outcome 1: If you bring this figure under £100,000, you protect your full Personal Allowance (saving up to £5,036 in tax).

● Strategic Outcome 2: If you bring this between £60,000 and £80,000, you can mitigate or eliminate the High Income Child Benefit Charge, clawing back significant household cash.

The Compounding Value of Early Advice

I frequently see proactive clients shift £20,000 or more into their retirement funds, dropping their effective marginal rate from 60% back to 40% and preserving thousands of pounds. I recently advised a couple where both partners were earning £105,000. By each contributing £6,000 into their workplace pensions via salary sacrifice, they dropped below the £100,000 line, fully restored their Personal Allowances, and protected their family’s Child Benefit entitlement—an immediate combined household benefit of several thousand pounds. These are legitimate, statutory tax reliefs actively encouraged by the system. However, timing is everything: you must implement these steps before 5 April 2027 for them to count for the current tax year.

Summary of Key Points

Summary of Critical Tax Traps

● The UK Personal Allowance is held at £12,570, and the higher-rate threshold begins at £50,270, meaning fiscal drag continues to pull middle earners into higher brackets.

● More than 7 million people are now higher-rate taxpayers, while the High Income Child Benefit Charge impacts individuals once income crosses £60,000.

● Earners between £100,000 and £125,140 face an effective 60% marginal tax rate due to the phased withdrawal of the Personal Allowance.

● You can effectively bypass these traps by lowering your adjusted net income through smart pension planning, Gift Aid, or corporate salary sacrifice arrangements.

● Review your details via your official Personal Tax Account at gov.uk; with thresholds extended through a long-term freeze until 2031, planning early is your best defense.

Comprehensive Frequently Asked Questions

Q1: What happens if someone has two PAYE jobs and one pushes their total income just over the £50,270 higher-rate threshold?

Ah, this one’s a classic trap I’ve sorted for dozens of clients over the years. HMRC usually allocates your standard 1257L tax code to your main (higher-paying) job to apply the personal allowance, while the second job is placed on a BR (Basic Rate) code – meaning 20% tax is deducted from the very first pound. If your combined income creeps over £50,270, the excess needs to be taxed at 40%. Because the full allowance is already utilized on your main job, a gap can form where you underpaid throughout the year. One teacher I advised in Leeds ran a small weekend tutoring gig; we proactively phoned HMRC mid-year to adjust his coding numbers so his monthly take-home remained accurate and avoided an unexpected bill after April.

Q2: Can an employee ask HMRC to split their personal allowance across multiple jobs instead of using BR on the second one?

Yes, absolutely, and it’s a route I highly recommend when both income streams are relatively predictable. Rather than allowing the second payroll to be hit with a flat basic rate from the outset, you can log into your Personal Tax Account or contact HMRC to request a split—allocating, for instance, 70% of the allowance to your primary role and 30% to the second. This flattens out your monthly deductions and avoids the frustration of a smaller paycheck being heavily taxed. Just ensure you review the arrangement every April or if your hours shift, as an imbalance can leave you owing a small balance at year-end.

Q3: If someone starts a second job part-way through the tax year, will they automatically go on an emergency tax code?

Quite often, yes. If your new employer hasn’t processed a P45 from a previous role or if the starter checklist is filled out incorrectly, HMRC will likely issue a temporary code like 1257L W1/M1 (Week 1/Month 1 basis). This treats each pay period in isolation and can cause you to be over-taxed for a month or two until the systems sync up. My standard advice is to double-check that your National Insurance number is perfectly recorded and ensure you select the correct employment statement on your starter forms. A client of mine who began driving for a delivery app alongside his main job saw nearly £400 over-withheld in his first few weeks; we reclaimed it smoothly, but it’s cash flow you’d prefer to keep in your pocket.

Q4: How does having multiple jobs affect National Insurance contributions now that employee rates are lower?

National Insurance is calculated per job rather than on your combined income. If you hold two separate employments, you benefit from a completely fresh Primary Threshold (the point where you start paying 0% NI) on each payroll, provided the employers aren’t connected. While it means you continue paying the main 8% employee Class 1 rate on both jobs rather than dropping to the 2% rate on your combined earnings over £50,270, the dual tax-free thresholds can sometimes work out in your favour depending on the split of your earnings.

Q5: What should someone do if their tax code on a second job suddenly changes to D0 because total income is estimated too high?

This occurs frequently when HMRC’s automated system projects that your combined earnings will place you deep into higher-rate territory. A D0 code instructs the payroll system to apply a flat 40% tax to every pound earned on that specific job. Your first step should be to log into your Personal Tax Account to identify what triggered the estimate—it’s often based on outdated historical data or an unremoved benefit-in-kind, like an old company car. Having your latest payslips to hand and providing HMRC with an accurate income forecast will resolve it. I assisted a London commuter whose old overtime figures had distorted his profile; we had the code reset to BR within a week and secured a £1,200 repayment.

Q6: If a Scottish resident has two jobs, one in England and one remote for a Scottish employer, which income tax bands apply?

Your income tax treatment is determined entirely by your residential status, not where your employer’s payroll office is situated. If you live in Scotland, you are a Scottish taxpayer. Consequently, HMRC will apply an ‘S’ prefix to your tax codes across all employments. Your total earnings will be subject to the devolved Scottish tax bands—meaning you will transition through the starter, intermediate, higher, advanced, and top Scottish rates as your income increases. I’ve seen cross-border workers face unexpected adjustments because an English payroll department initially applied standard rest-of-UK brackets; a swift correction to the tax code ensures accuracy and prevents a reconciliation bill down the line.

Q7: Does rental income count towards the £50,270 higher-rate threshold for someone with a single PAYE job?

Yes, it does. HMRC calculates your total taxable income by adding your net rental profits (after allowable expenses and property tax credits) to your employment earnings. While your primary PAYE job will typically retain its standard 1257L code, the extra tax due on the rental profits pushing you past £50,270 will be collected either via a tax code adjustment or through your Self Assessment calculation. A landlord client in Bristol earning a £45,000 salary alongside £8,000 in net rent was caught off guard by a £1,600 liability; by exploring a legitimate transfer of a share of the property ownership to his lower-earning spouse, we were able to utilise her basic-rate band instead.

Disclaimer

The information provided in this article is for general guidance only and is not intended to constitute professional advice, tax advice, financial advice, legal advice, or any other form of regulated guidance. Although every effort has been made to ensure accuracy at the time of publication, Fair View Accounting Services, including its director, employees, contractors, writers, and content-creation team, accepts no responsibility for any loss, damage, penalty, or consequence arising from reliance on the information contained herein.

UK tax legislation changes frequently, and HMRC interpretations, thresholds, and rules may vary depending on the individual circumstances of each taxpayer. Nothing in this article should be considered a substitute for obtaining formal, personalised advice from a qualified accountant or tax professional. Readers should not take action—or refrain from taking action—based solely on the content published on this website.

Fair View Accounting Services does not guarantee the completeness, accuracy, or ongoing validity of the information provided and assumes no liability for omissions or errors, whether typographical, factual, or technical. By using this content, the reader acknowledges that all responsibility for decisions remains solely with the user.