APR After April 2026 — How Tenant Farmers Lose 50% Relief

A lot of commentary around APR after April 2026 is misleading because it collapses two different issues into one headline. The first is the long-standing APR rule that some let agricultural property has only ever qualified for 50% relief. The second is the new rule from 6 April 2026, which caps the combined 100% APR/BPR allowance at £2.5 million and then gives 50% relief above that level. In other words, APR has not disappeared, but the way it works is materially worse for larger estates and for anyone whose land is already trapped in an older tenancy structure.

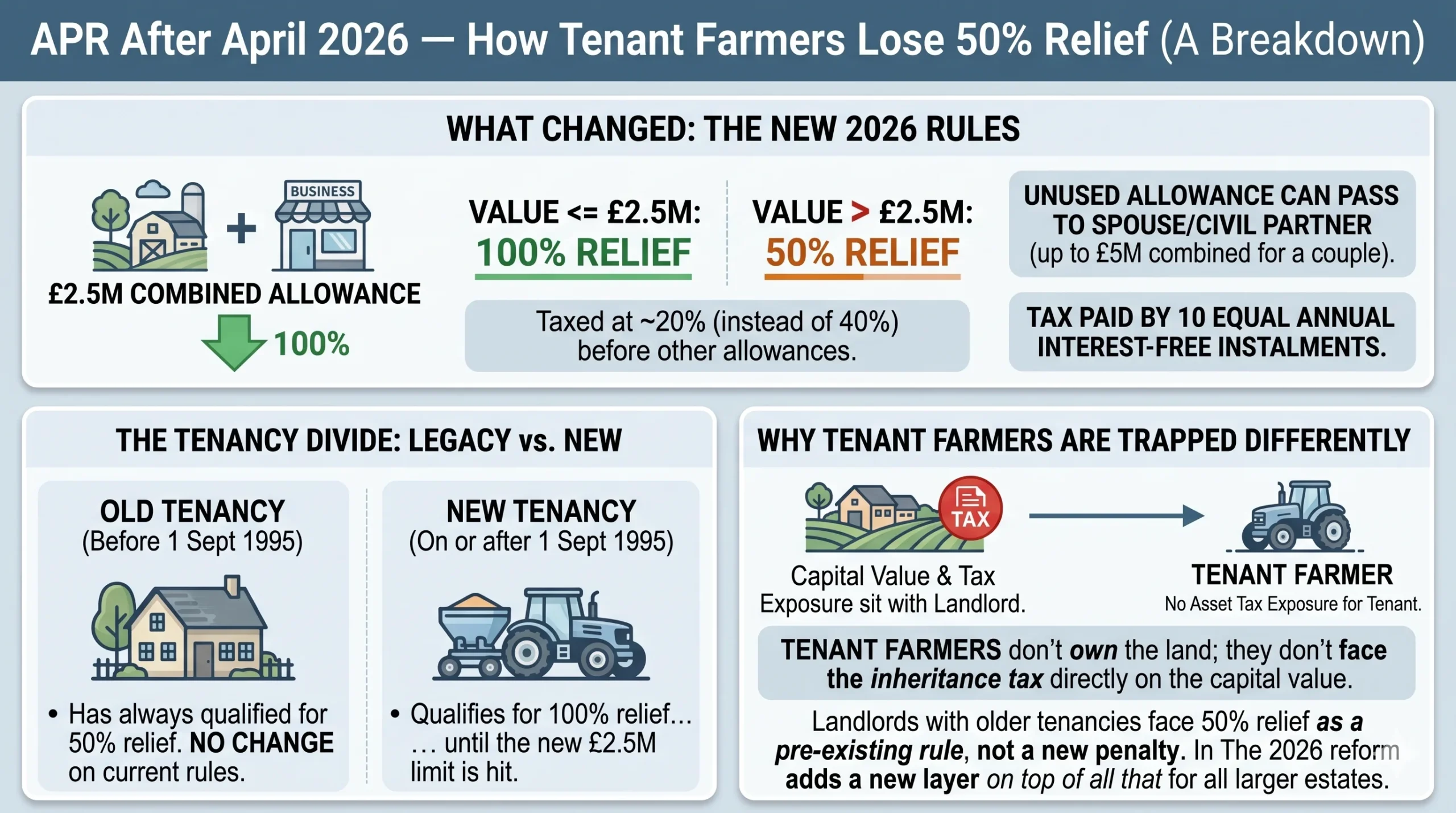

What Changed From 6 April 2026

From 6 April 2026, the full 100% rate of Agricultural Property Relief and Business Property Relief is restricted to the first £2.5 million of combined qualifying agricultural and business property. Anything above that allowance receives 50% relief, which means the exposed slice is taxed at an effective 20% rather than 40% before any other inheritance tax allowances are applied. HMRC and GOV.UK also confirm that any unused allowance can be transferred between spouses or civil partners, and that the tax on qualifying assets can be paid by 10 equal annual instalments interest free.

The practical point is that many articles still mention the old £1 million allowance, but that figure was later increased to £2.5 million in December 2025. That matters because readers are now planning around a materially larger cushion than the original Budget 2024 announcement suggested. For couples, the government’s stated position is that up to £5 million of qualifying agricultural or business assets can pass between them before the 100% relief allowance is exhausted, on top of the usual nil-rate band.

There is also an important transitional point. The new allowance is not just about what is owned on death. It can also be affected by qualifying property given away on or after 30 October 2024 if the donor dies within seven years of the gift, and by qualifying property in trusts that is treated as part of the estate. That means some families who think they made their planning move “before the change” may still fall inside the new regime.

Why Tenant Farmers Need to Look at This Differently

The phrase “tenant farmers lose 50% relief” is easy to misread. In practice, the key question is usually not whether a tenant farmer is farming land, but whether the land or rights in question are actually in their estate at all. HMRC’s guidance on farm business tenancies is clear that the tenancy gives exclusive occupation to the tenant, not the owner. That means the APR exposure often sits with the landlord’s estate, not with the tenant’s own assets. That is an inference from HMRC’s occupation guidance, but it is the right way to read the rules in practice.

For let agricultural land, APR has always worked differently from owner-occupied land. HMRC says property qualifies for 100% relief if it is farmed by the owner, used under a short-term grazing licence, or let on a tenancy that began on or after 1 September 1995. In all other cases, the rate is 50%. So if you are dealing with a tenancy that started before 1 September 1995, the lower rate is not a new April 2026 penalty; it is the existing rule. The 2026 reform adds another layer on top of that for estates with qualifying assets above the new £2.5 million allowance.

That distinction matters because many older tenanted farms are already in the 50% category, while newer farm business tenancies often fall into the 100% category until the new allowance is used up. A reader who simply hears “APR is now 50%” can easily come away with the wrong result. The correct answer depends on both the age of the tenancy and the value of the qualifying property in the estate.

Another common mistake is to assume APR covers the market value of the whole farm. It does not. HMRC says property is valued as if it could only be used for agricultural purposes, and any value above that agricultural value, such as the hope value of land or the market value of a country residence, does not qualify for Agricultural Relief. That is often where the real inheritance tax bill is hidden, especially on farms near development land or where a farmhouse is larger or more valuable than the farming operation would justify.

APR After April 2026

Separating Fact from Fiction for Tenant Farmers

Recent commentary regarding Agricultural Property Relief (APR) reforms is often misleading, conflating historical rules with new limits. This briefing clarifies the actual impact of the £2.5 million cap and explains why tenant farmers are positioned differently than headlines suggest.

1. The Core Change: The £2.5M Cap

From 6 April 2026, the 100% rate of APR and Business Property Relief (BPR) is restricted. The relief applies fully only to the first £2.5 million of combined qualifying property. Anything above this threshold drops to a 50% relief rate.

Because standard Inheritance Tax (IHT) is 40%, applying a 50% discount means the "exposed slice" above £2.5 million is taxed at an effective 20% rate before other allowances.

Comparing the effective tax rate applied to estate value before and after the £2.5M threshold.

2. Allowances & Spousal Pooling

Many early reports focused on a £1 million allowance, but this was updated. More importantly, HMRC confirms that unused allowances can be transferred between spouses or civil partners.

This means a married couple can pass up to £5 million of qualifying agricultural/business assets completely free of the new restriction, sitting on top of usual nil-rate bands. To assist with liquidity, tax on qualifying assets can be paid over 10 equal, interest-free annual instalments.

Visualizing the actual planning cushions available versus initial budget fears.

3. The Transition Trap

Some families rushed to gift assets to avoid the new rules. However, a strict transitional rule applies. If you made gifts thinking you moved "before the change," you may still fall inside the new regime.

4. The Tenant Farmer Misconception

The headline "Tenant Farmers Lose 50% Relief" is fundamentally misread. The core issue is not who is farming, but whose estate holds the capital value. Tenant farmers hold exclusive occupation rights, not the freehold. Therefore, the APR exposure almost exclusively sits with the landlord.

Landlord (Freeholder)

- ✓ Owns the capital asset.

- ✓ Value sits in their taxable estate.

- ⚠ Bears the IHT risk and the £2.5M cap limits.

Tenant Farmer

- ✓ Holds exclusive occupation rights.

- ✓ Land value does NOT sit in tenant's estate.

- ✓ No direct asset tax exposure from these rules.

While tenants don't face the tax directly, landlords may feel pressure to renegotiate rent or reclaim land to restructure their tax position.

5. The 1995 Boundary: Legacy Rules vs New Rules

For let agricultural land, APR has always worked differently. Properties let on a tenancy beginning before 1 September 1995 (like AHA tenancies) have only ever qualified for 50% relief. This is not a new penalty; it is a three-decade-old rule. The 2026 reform simply adds the £2.5M cap layer on top of modern (post-1995) tenancies and owner-occupied land.

Comparing landlord maximum available relief based on tenancy structures before and after the April 2026 changes.

The Two Questions That Decide the Outcome

The first question is who actually owns the asset. A tenant farmer may operate the business, but that does not mean the farmed land is in their estate. If they do own a farmhouse, cottages, equipment, partnership interests or business assets, those assets may still qualify for APR or BPR depending on the facts. But the tenanted land itself normally sits with the landlord, so the tax impact from the 2026 change often lands there first.

The second question is whether the arrangement gives the occupier the right to vacant possession or falls within the old pre-1995 letting rules. HMRC notes that if no tenancy existed and vacant possession could be obtained, 100% relief rather than 50% would apply, though the availability of 100% relief may now be restricted from 6 April 2026. HMRC also says it is still important to check whether an agricultural tenancy existed, because the tenancy history can change the rate materially.

This is why old paperwork matters. Partnership agreements, historic rent deductions, previous owner files, and rental income records can all be relevant evidence when deciding whether the land was under a tenancy and, if so, when that tenancy began. Inheritance tax cases on farms are often won or lost on documentation rather than on agricultural principle.

A Realistic Example

Take a landlord’s estate that includes tenanted agricultural property and other qualifying business assets worth £3.4 million in total. Under the post-April 2026 rules, the first £2.5 million can qualify for 100% relief. The remaining £900,000 qualifies only for 50% relief, so £450,000 remains chargeable to inheritance tax. At the standard 40% rate, that creates an inheritance tax charge of £180,000 on the excess slice alone. That is what the government means when it says the effective rate on the excess is up to 20%.

Now compare that with an older tenancy that began before 1 September 1995. If the land or interest is in the 50% category, half of the agricultural value is still exposed to inheritance tax even before the new allowance is considered. On a £1.8 million agricultural value, for example, 50% APR would shelter £900,000 and leave £900,000 chargeable before any nil-rate band or spouse exemption is applied. That is not the same as “50% tax”; it is 50% relief, which usually translates into 20% inheritance tax on the part that loses relief.

For married couples and civil partners, the position can be softer, but only if the unused allowance is available and properly claimed. GOV.UK says any unused £2.5 million allowance from a late spouse or civil partner can be transferred, subject to a claim being made within the relevant time limits. Where the first death was before 6 April 2026, HMRC assumes the full £2.5 million allowance is available for transfer to the survivor. That makes estate planning for farm-owning couples more forgiving than for single owners, but it does not eliminate the need to map the structure carefully.

Agricultural Property Relief

After April 2026 — The Full Picture

A comprehensive guide for UK taxpayers on how APR & BPR changed from 6 April 2026, what it means for tenant farmers, and where the real risks lie.

📊 Key Numbers at a Glance

🔍 What Actually Changed

Much of the commentary around APR after April 2026 is misleading because it collapses two separate issues into one headline. Understanding which rule applies to your situation is essential before making any planning decisions.

Agricultural land let on tenancies that started before 1 September 1995 has only ever attracted 50% APR. This is not a new 2026 penalty — it is the long-standing HMRC rule that predates the recent reforms entirely.

From 6 April 2026, the combined 100% APR/BPR relief is capped at £2.5 million per estate. Assets above that allowance receive 50% relief only — creating an effective 20% IHT charge on the excess.

🏡 APR Rates: Which Rate Applies?

| Scenario | APR Rate Available | Key Condition | 2026 Cap Applies? |

|---|---|---|---|

| Owner-occupied farmland | 100% | Owner personally farms the land | Yes — above £2.5m |

| Farm Business Tenancy (post-1 Sep 1995) | 100% | New-style FBT — tenancy started on or after 1 Sep 1995 | Yes — above £2.5m |

| Short-term grazing licence | 100% | Licence (not tenancy) granted for grazing | Yes — above £2.5m |

| Old-style tenancy (pre-1 Sep 1995) | 50% | Tenancy started before 1 September 1995 | Yes — compounded further |

| Any asset above £2.5m combined cap | 50% | Excess above the new allowance, regardless of tenancy type | Directly affected |

| Farmhouse (larger / luxury) | Partial / None | Only agricultural value qualifies — residential uplift excluded | Partially |

📅 Chronological Timeline of Changes

🌾 What "Tenant Farmers Lose 50% Relief" Really Means

HMRC's guidance is clear that a Farm Business Tenancy (FBT) gives exclusive occupation to the tenant, not ownership. The APR liability typically belongs to whoever owns the land — usually the landlord.

⚖️ Two Questions That Decide the Outcome

🗂️ Why Old Paperwork Matters

🔀 APR & BPR Interaction

🧮 IHT Liability Estimator

Enter the details of the estate below to estimate the inheritance tax exposure under the post-April 2026 rules. This is a simplified illustrative tool — always take professional advice for formal planning.

📖 Worked Examples

Scenario: A landlord's estate includes a post-1995 Farm Business Tenancy and other qualifying business assets worth £3.4 million in total.

• First £2.5m → 100% relief → £0 chargeable

• Remaining £900,000 → 50% relief → £450,000 chargeable

• IHT at 40% on £450,000 → £180,000 (before nil-rate band)

• Effective rate on the whole estate: approximately 5.3%

• This can be paid at £18,000 per year for 10 years, interest-free.

Scenario: A landlord's estate includes land let under an old tenancy started before 1 September 1995, with agricultural value of £1.8 million.

• 50% APR applies (pre-1995 tenancy rule, not the new cap)

• 50% of £1.8m = £900,000 sheltered by APR

• £900,000 remains chargeable to IHT before any nil-rate band

• IHT at 40% = £360,000

• This is not "50% tax" — it is 50% relief, which translates into approximately 20% effective IHT on the total agricultural value.

Scenario: A married couple owns qualifying agricultural assets of £5 million. The first spouse dies, and the full £2.5m allowance is transferred to the survivor.

• Survivor has £5m of qualifying assets and £5m total allowance (£2.5m own + £2.5m transferred)

• All £5m → 100% relief → £0 APR/BPR-related IHT (before normal nil-rate band)

• Additionally, the couple's standard nil-rate bands (£650,000 combined) and any residence nil-rate band (up to £350,000 combined) may reduce other estate IHT further.

• Important: This only works if the allowance transfer is properly claimed within the relevant time limits.

⚠️ Common Mistakes That Lead to the Wrong Answer

✅ Your Pre-Planning Action Checklist

Before making any farm succession or estate planning decision, work through each of these steps. The correct APR/BPR answer depends entirely on the specific facts of each estate.

Step 1 — Establish Ownership & Asset Scope

- ✓ Identify who owns each asset. Does the tenanted farmland sit in the operator's estate or the landlord's? Which assets are truly in the estate for IHT purposes?

- ✓ Check whether each asset is agricultural property at all. Land with planning permission, development potential, or recreational use may fall outside APR entirely.

- ✓ Separate agricultural value from market value. The APR calculation is on agricultural value only. Any residential, development or hope value above that is exposed to full IHT.

Step 2 — Check Occupation & Tenancy History

- ✓ Confirm whether land is owner-occupied or let. Owner-occupied land or land under a post-1 Sep 1995 FBT → 100% APR rate. Pre-1995 tenancy → 50% only.

- ✓ Locate all tenancy agreements and their start dates. Retrieve old partnership agreements, rent records and previous owner files. The tenancy start date is often the most critical single fact.

- ✓ Check vacant possession position. If no tenancy exists and vacant possession is available, 100% APR applies (subject to the new cap). This can significantly change the valuation and the relief available.

- ✓ Review the farmhouse position. Is the farmhouse value justified by the scale of the farming operation? If HMRC judges it as a country residence rather than a working farmhouse, APR on that element may be challenged.

Step 3 — Map the £2.5m Allowance

- ✓ Total the combined APR/BPR qualifying value. Add all qualifying agricultural and business assets. Does the total exceed £2.5 million?

- ✓ Include lifetime gifts made on or after 30 October 2024. These count towards the £2.5m cap (applied in date order, earliest first) if death occurs within seven years and on or after 6 April 2026.

- ✓ Account for trust assets. Qualifying property held in trusts may also be treated as part of the estate and affect the allowance calculation.

- ✓ Assess spousal transferability. If married or in a civil partnership, has any unused allowance from a deceased partner been identified? A formal claim within time limits may be required.

Step 4 — Assess the Practical Burden

- ✓ Calculate the IHT above the cap. The excess above £2.5m is not lost to full IHT — it still receives 50% relief. The effective rate is 20%. Use the calculator tab to estimate the liability.

- ✓ Consider the instalment option. IHT on qualifying APR/BPR assets can be paid in 10 equal annual interest-free instalments. This can make a large bill commercially manageable without a forced land sale.

- ✓ Review wills in light of the new rules. Wills drafted before December 2025 may not reflect the new £2.5m allowance or the transferability changes. Update estate planning documents accordingly.

- ✓ Obtain specialist professional advice. The interaction of APR, BPR, the nil-rate band, the residence nil-rate band, and trust structures makes individualised advice essential. Do not rely on generic summaries alone.

Quick Decision Flow

Common Mistakes That Lead to the Wrong Answer

The most frequent error is to treat APR as though it applies to the whole farm at market value. It does not. A farmhouse may be partly or wholly excluded if its value reflects residential appeal rather than agricultural use, and land with development potential may also have value outside APR. Another common error is to assume every tenant farmer is in the same position. They are not: the age of the tenancy, the contractual rights in the lease, and the ownership chain all change the result.

A second mistake is to rely on summaries that still use the original £1 million allowance. Those summaries are now out of date because the allowance was increased to £2.5 million in December 2025. A third is to overlook lifetime gifts made after 30 October 2024, which can still be caught if the donor dies within seven years after 6 April 2026. In farm succession work, timing is often as important as valuation.

A final mistake is to assume that because the asset is agricultural, business relief is irrelevant. HMRC’s manuals repeatedly note that APR and BPR can overlap, but APR takes priority on the agricultural value and BPR may only be relevant to any excess value in some cases. That interaction matters where farms are diversified, where land is owned through a partnership, or where the business includes assets beyond pure farmland.

What to Check Before Making a Succession Decision

The sensible starting point is to separate ownership, occupation and valuation. Work out which assets are actually in the estate, whether each one is agricultural property at all, whether the occupation test is met, and whether the tenancy began before or after 1 September 1995. Then look at the total combined APR/BPR value and see whether it exceeds the new £2.5 million allowance, taking spouse or civil partner transferability into account.

After that, the issue becomes timing. If the estate includes qualifying property over the allowance, the excess is not lost to full inheritance tax immediately; it still gets 50% relief and the tax can be paid by instalments over 10 years interest free. That can make a large bill manageable, but it does not remove the commercial pressure on land-rich families who may need liquidity to keep the farm intact.

For tenant-farming structures, the most useful question is often not “How do I claim APR?” but “Whose estate is actually exposed, and on what slice of value?” In many cases the answer is the landlord’s estate, not the tenant’s. In others, particularly where the tenant owns separate business assets, the exposure may sit partly inside APR and partly inside BPR. That is why a one-line answer is rarely reliable enough for succession planning.

Summary of Key Insights

APR was not abolished in April 2026. The real change is that 100% relief is now capped at £2.5 million of combined APR/BPR, with 50% relief above that level, and the government later increased the allowance from the original £1 million to £2.5 million.

For tenant farmers, the crucial issue is ownership and tenancy history. A farm business tenancy usually means the tenant is in occupation, not the owner, so the APR risk often sits with the landlord’s estate. Older tenancies can still sit in the 50% category, while newer tenancies may qualify for 100% relief until the new allowance is used up.

The biggest practical errors are assuming APR applies to market value, relying on outdated £1 million summaries, and missing lifetime gifts or tenancy documents that change the outcome. For anyone with land, a farmhouse, or a mixed farm business, the right response is to check the ownership structure and the tenancy dates before relying on a headline figure.

FAQs

Q1: Can someone still qualify for 100% Agricultural Property Relief if they farm rented land rather than owning it?

A1: Well, it’s worth noting that APR mainly applies to ownership of qualifying agricultural property, not simply to farming activity itself. A tenant farmer working rented land may still qualify for relief on assets they actually own — such as livestock, machinery, partnership interests or a farmhouse they purchased separately — but the rented land itself normally belongs to the landlord’s estate for inheritance tax purposes.

I’ve seen confusion where farming families assume decades of occupation automatically create inheritance tax protection over the land. HMRC looks at legal ownership first. Long occupation alone does not transfer APR entitlement to the tenant.

Q2: Can a farming partnership lose relief if the paperwork is outdated or informal?

A2: Yes, and this catches more farming families than people realise. In practice, HMRC often scrutinises old partnership agreements after a death, especially where parents, adult children and spouses are all involved informally.

A common issue is where the tax returns show a partnership exists, but the written agreement has not been updated for twenty years. If ownership of machinery, livestock or farming profits is unclear, disputes can arise over whether Business Property Relief or APR applies correctly.

In my experience with farming clients, tidy legal paperwork frequently matters just as much as the farming activity itself.

Q3: Can a farmhouse fail to qualify for APR even if it sits on a working farm?

A3: Absolutely. This is one of the most misunderstood areas of inheritance tax planning. A farmhouse must be genuinely character-appropriate to the farming operation and occupied for agricultural purposes.

If a retired owner still lives in a large farmhouse while the actual farming is handled entirely by contractors or a separate farming company, HMRC may argue the property has become mainly residential rather than agricultural.

I once reviewed a case where the farmhouse value exceeded the productive value of the surrounding land. That imbalance alone raised serious APR concerns.

Q4: Can a tenant farmer claim relief on diversification income such as holiday lets or farm cafés?

A4: Potentially, but usually under Business Property Relief rather than APR. Once farming businesses diversify heavily, the tax analysis becomes much more nuanced.

For example, a Yorkshire farming business earning modest crop income but substantial profits from glamping pods and weddings could face arguments that parts of the estate are investment-related rather than trading activities.

The key is looking at the overall business profile. Mixed-use farms need careful review because diversification can help profitability commercially while complicating inheritance tax relief technically.

Q5: Can older Agricultural Holdings Act tenancies create bigger inheritance tax problems?

A5: They often do. Older tenancy arrangements may only qualify for 50% APR rather than 100%, particularly where vacant possession rights are restricted.

The difficulty is that many farming families inherited these arrangements decades ago and never revisited them because the structures worked commercially. After the April 2026 changes, that historic tenancy wording suddenly becomes far more financially significant.

It’s a common mix-up, but families sometimes think the new rules alone caused the problem when the tenancy had already limited relief for years.

Q6: Can someone reduce inheritance tax exposure by giving farmland away before death?

A6: Sometimes, yes — but timing is now critical. Gifts made after late 2024 can still fall into the new regime if the donor dies within seven years.

What people often overlook is that gifting farmland while continuing to benefit from it can create a “gift with reservation” issue. If the parent still receives rental income, controls the land or effectively treats it as their own, HMRC may still include it in the estate.

I’ve seen situations where families thought they had completed succession planning, only to discover the structure was ineffective because practical control never really changed.

Q7: Can APR and Business Property Relief apply together on the same farm?

A7: Yes, and this is where many online explanations oversimplify things. APR normally applies first to the agricultural value of qualifying property, while Business Property Relief may sometimes apply to additional business value.

Consider a modern dairy operation with processing facilities and a branded farm shop. Part of the value may relate to pure agricultural use, while another element reflects the wider trading business.

That overlap can be extremely valuable, but it also means valuations need to be professionally prepared rather than estimated casually.

Q8: Can a landlord lose APR if land is no longer actively farmed?

A8: Potentially, yes. Agricultural property must generally still be used for agricultural purposes. Land left unused for extended periods, or moved entirely into non-farming activity, can weaken relief claims.

A practical example would be land bought for future development but no longer genuinely farmed in the meantime. Owners sometimes assume occasional grazing is enough automatically. HMRC tends to look at the real commercial picture rather than cosmetic arrangements.

That distinction becomes increasingly important where development value is substantial.

Q9: Can tenant farmers be affected even if they do not personally pay inheritance tax?

A9: Yes, because inheritance tax pressure on landlords can indirectly affect tenants. Some landlords facing future inheritance tax liabilities may restructure holdings, sell land, renegotiate tenancy arrangements or reduce long-term commitments.

In farming communities, these changes often ripple outward. A tenant may suddenly face uncertainty over renewal terms or succession opportunities because the landowner’s tax planning priorities changed after the APR reforms.

Q10: Can machinery and livestock still qualify for relief after the new rules?

A10: In many cases, yes, through Business Property Relief rather than APR. However, the combined relief cap means larger farming operations may now reach the threshold faster than expected.

People often focus purely on land values, but expensive machinery can materially increase the qualifying estate value. Modern combines, robotic milking systems and grain storage facilities are not minor assets anymore.

I’ve worked with farms where machinery alone exceeded several hundred thousand pounds.

Disclaimer

The information provided in this article is for general guidance only and is not intended to constitute professional advice, tax advice, financial advice, legal advice, or any other form of regulated guidance. Although every effort has been made to ensure accuracy at the time of publication, Fair View Accounting Services, including its director, employees, contractors, writers, and content-creation team, accepts no responsibility for any loss, damage, penalty, or consequence arising from reliance on the information contained herein.

UK tax legislation changes frequently, and HMRC interpretations, thresholds, and rules may vary depending on the individual circumstances of each taxpayer. Nothing in this article should be considered a substitute for obtaining formal, personalised advice from a qualified accountant or tax professional. Readers should not take action—or refrain from taking action—based solely on the content published on this website.

Fair View Accounting Services does not guarantee the completeness, accuracy, or ongoing validity of the information provided and assumes no liability for omissions or errors, whether typographical, factual, or technical. By using this content, the reader acknowledges that all responsibility for decisions remains solely with the user.