The CGT Time Bomb Inside A Settlor-Interested Trust

The CGT Time Bomb Inside a Settlor-Interested Trust in the UK

Settlor-interested trusts remain a common planning tool for UK business owners, landlords, and higher-rate taxpayers seeking to manage assets for family or succession purposes. Yet many hold a hidden capital gains tax exposure that can catch even experienced advisers off guard. In the current 2026 environment—with CGT rates at 18% and 24% for individuals and a flat 24% for most trust gains—the mechanics of these trusts can turn what looks like straightforward asset protection into an expensive tax surprise.

What Makes a Trust Settlor-Interested for CGT Purposes?

A trust is settlor-interested for capital gains tax (and income tax) where the settlor or their spouse or civil partner can benefit from the trust property or income in the relevant tax year. This includes situations where they are a potential beneficiary under the trust deed, even if they have not actually received anything yet.

For UK-resident trusts, the practical effect since 2008/09 has been that trustees remain liable for CGT on gains arising inside the trust. The settlor is not directly assessed on the gains in the same way as for income in many cases, but the “interested” status triggers important restrictions and interactions.

The definition is wide. It covers not only direct entitlements but also arrangements under which the settlor or spouse might acquire an interest. Minor children can also trigger issues in certain contexts, though the primary focus for CGT is the settlor/spouse.

Why It Creates a “Time Bomb”

The core problem is a mismatch between economic reality and tax treatment. The settlor has not fully divested themselves for tax purposes, yet the assets sit in a separate legal entity with its own tax rules. This produces several pressure points:

- Restricted Hold-Over Relief on Creation: Hold-over relief under TCGA 1992 s165 (business assets) or s260 (chargeable lifetime transfers) is generally unavailable on transfers into a settlor-interested trust. This means the settlor often crystallises a gain immediately on gifting appreciating assets—such as shares in a family company, buy-to-let property, or investment portfolios—rather than deferring it.

Many older trusts were created before this rule was fully appreciated, or before the settlor’s circumstances changed. Assets transferred with the benefit of relief in earlier years can face clawback if the trust later becomes (or is discovered to be) settlor-interested.

- Trustees Pay CGT at Flat Higher Rates: Trustees of UK-resident trusts typically pay CGT at 24% on gains (aligned with the higher rate for individuals post-2024 changes). The annual exempt amount is limited—£1,500 for 2026/27, shared across multiple trusts created by the same settlor (minimum £300 per trust).

This rate applies regardless of the settlor’s personal tax position. There is no uplift or band utilisation from the settlor’s basic rate band.

- Losses Do Not Flow Freely: Following the repeal of the old TCGA 1992 s77 rules, personal capital losses of the settlor generally cannot be offset against trust gains. Trust losses can only be carried forward against future trust gains, not surrendered to the settlor. This asymmetry traps losses inside the structure while the settlor pays tax on personal gains elsewhere.

- Exit and Appointment Charges: When assets leave the trust—whether by appointment to beneficiaries, termination of an interest in possession, or winding up—there is a disposal at market value. Trustees pay CGT on the gain. If the trust was settlor-interested, additional complications arise around whether hold-over relief is available on the way out (it can be in some cases) and the interaction with inheritance tax.

For interest in possession trusts where the settlor is the life tenant, the IHT treatment (often treated as owned by the settlor) contrasts sharply with the CGT position, creating planning tension on death or termination.

The CGT Time Bomb Inside A Settlor-Interested Trust

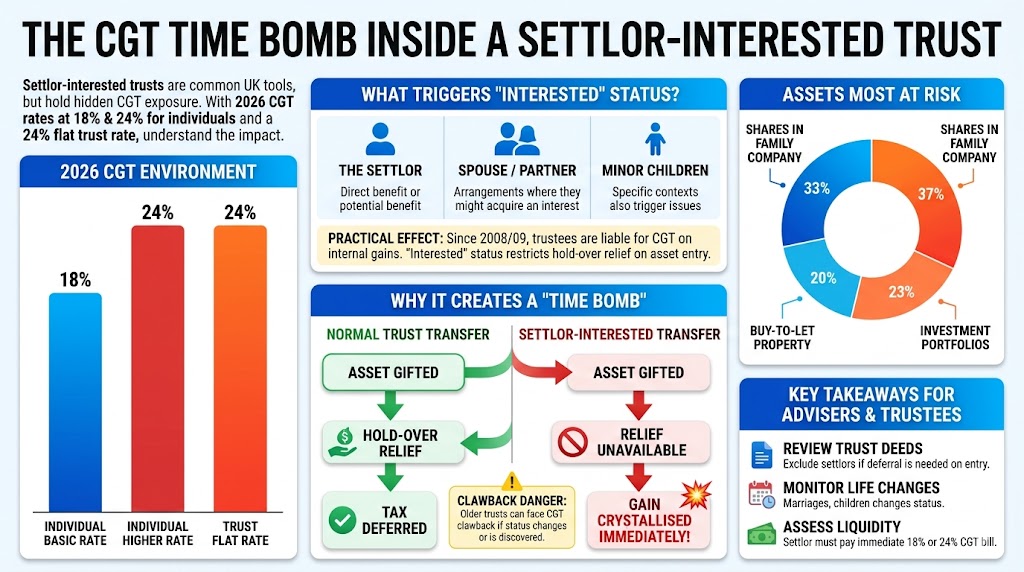

Settlor-interested trusts are a common UK planning tool for business owners and landlords. Yet, beneath the surface of asset protection lies a hidden capital gains tax exposure that can turn a straightforward transfer into an expensive tax surprise.

The 2026 CGT Environment

Understanding the risk begins with the current tax rates. In 2026, individuals face tiered Capital Gains Tax rates depending on their income band, while trusts are subject to a flat, higher rate. This discrepancy makes tax efficiency crucial when moving assets.

What Triggers the "Interested" Status?

A trust is settlor-interested for CGT if the settlor or their spouse/civil partner can benefit from the property or income in the relevant tax year. Even being a potential beneficiary triggers this status.

The Settlor

Direct entitlements or potential benefits.

Spouse / Partner

Arrangements where a spouse might acquire an interest.

Minor Children

Can also trigger issues in specific contexts.

Practical Effect: Since 2008/09, trustees remain liable for CGT on gains arising inside the trust, but the "interested" status imposes severe restrictions on how assets enter the trust.

Why It Creates a "Time Bomb"

The core problem is a mismatch between economic reality and tax treatment. The settlor hasn't fully divested themselves, yet the assets sit in a separate legal entity. This leads to the critical pressure point: Restricted Hold-Over Relief on Creation.

Asset Gifted to Trust

Hold-Over Relief Allowed

(s165 or s260 applies)

Asset Gifted to Trust

Relief Generally Unavailable

(Transfer INTO trust restricted)

⚠ The Clawback Danger

Many older trusts were created before this rule was fully appreciated. Assets transferred with the benefit of relief in earlier years can face clawback if the trust later becomes (or is discovered to be) settlor-interested due to changed circumstances.

Assets Most at Risk

The time bomb detonates when highly appreciating assets are transferred. Because hold-over relief is denied, the settlor must pay CGT on the assumed market value gain, despite receiving no cash from the transfer to pay the tax bill.

Key Takeaways for Advisers & Trustees

-

✔

Review Trust Deeds

Carefully analyze the class of beneficiaries. Exclude settlors and spouses explicitly if hold-over relief is required on entry.

-

✔

Monitor Life Changes

Marriages, civil partnerships, or changes to minor children's status can inadvertently trigger settlor-interested rules, risking clawback.

-

✔

Assess Liquidity

If a transfer must occur into a settlor-interested trust, ensure the settlor has external liquidity to pay the immediate 18% or 24% CGT bill.

Real-World Scenarios That Trigger the Bomb

Family Investment Company or Portfolio Trust

A business owner transfers shares or a portfolio into a discretionary trust for children and grandchildren but retains a power to benefit or includes their spouse as a potential beneficiary. Gains accrue inside the trust at 24%. When the settlor later needs access or the trust is restructured, the accumulated gains are taxed without access to the settlor’s full annual exemption or lower-rate band. Personal losses sitting outside cannot help.

Buy-to-Let Property in Trust

Landlords sometimes place property in trust for succession planning. Principal private residence relief may be restricted or unavailable for periods the property was held in trust. On sale or appointment out, the gain is calculated from the original base cost (or rebased value), and hold-over was likely unavailable on entry. Multiple properties compound the issue.

Director/Shareholder Succession

Shares in a trading company are settled to facilitate Business Property Relief for IHT while the settlor retains influence. If the trust is settlor-interested, Business Asset Disposal Relief (BADR) on a future exit may be limited or unavailable in the trust context, and the initial transfer triggered tax.

Unwinding or Varying the Trust

Many settlors assume they can simply “take the assets back” with minimal tax cost. In practice, this can trigger CGT on the trustees’ disposal, potential loss of reliefs, and IHT implications if the settlor’s interest ends (treated as a PET or CLT depending on the structure).

Key Distinctions Often Missed

- UK Resident vs Offshore: For UK-resident trusts, trustees pay the tax. For offshore settlor-interested trusts, post-2025 changes have tightened the regime, with gains and income often charged on the settlor directly unless protected or qualifying under new rules. The “time bomb” shifts but does not disappear.

- Income Tax Overlap: Income arising in a settlor-interested trust is typically taxed on the settlor at their marginal rates. This can push them into higher CGT bands on personal disposals in the same year.

- IHT Interaction: A trust that is settlor-interested for CGT/income tax is often a Gift with Reservation (GWR) for IHT. The assets remain in the settlor’s estate. This double categorisation is useful for IHT but creates the CGT friction on exit.

Practical Steps and Risk Management

Review the trust deed carefully. Many older deeds contain wide powers that inadvertently make the trust settlor-interested long after the settlor assumed they had stepped away.

Consider whether the settlor can irrevocably exclude themselves and their spouse. This would typically take the trust out of settlor-interested status going forward, though historic gains and relief restrictions remain.

Timing matters. With CGT rates now aligned at the higher end and annual exemptions low, deferring or restructuring carries real cost. Professional valuation and detailed modelling of exit scenarios are essential before action.

Loss harvesting inside the trust, careful use of any available reliefs (such as on business assets where hold-over might still apply on exit in limited cases), and coordination with the settlor’s personal tax position can mitigate damage.

For trusts holding residential property, the 60-day reporting and payment window on disposals still applies to trustees.

UK taxpayer explainer for 2026/27

The CGT Time Bomb Inside A Settlor-Interested Trust

A settlor-interested trust can feel like family succession planning with a clean legal wrapper. For CGT, the wrapper can behave more like a pressure vessel: entry relief may be blocked, trustees face a flat 24% rate, losses can become trapped, and exits can crystallise gains at awkward moments.

Benefit can be enough

The trust is settlor-interested where the settlor, spouse, or civil partner can benefit from trust income or property in the tax year. Actual payment is not the only test; being a potential beneficiary can matter.

Trustees usually pay

For UK-resident trusts, trustees are generally the CGT taxpayer. Since the old section 77 regime was repealed, settlor personal losses usually do not rescue trustee gains.

Attribution can move the charge

For non-resident settlor-interested trusts, TCGA section 86 can attribute gains to a UK-resident settlor. From 6 April 2025, the end of domicile-based protection makes offshore structures a much hotter review area.

Hold-over relief may be blocked

Transfers into trust are normally treated as market-value disposals. Where the trust is settlor-interested, common hold-over routes can be unavailable, so the gain may crystallise immediately.

Gains compound inside a small allowance

Trustees pay a flat 24% CGT rate for 2026/27 and have only a limited annual exempt amount. No basic-rate band from the settlor is available to dilute the charge.

Appointments are disposals

When assets leave the trust, trustees can be treated as disposing of them at market value. Relief on exit is possible only in specific cases and needs careful deed, asset, and IHT analysis.

Family portfolio or FIC shares

Spouse included as a discretionary beneficiary? Gains may build at trustee rates while the settlor's personal losses and lower-rate capacity sit outside the structure.

Buy-to-let in trust

Entry can trigger a gain, private residence relief may be limited, and a future sale or appointment must be modelled with the 60-day property reporting deadline in mind.

Trading-company shares

Business Property Relief for IHT and CGT reliefs are different machines. BADR, hold-over, control, and beneficiary status need testing before a share transfer or company sale.

Main CGT rates rose to 18% and 24%, and the trustees' rate rose to 24% for disposals from 30 October 2024.

The UK moved away from domicile as the core test for many foreign income and gains rules. Offshore settlor-interested structures lost important protections.

The trust annual exempt amount remains low at £1,500, or less where multiple trusts by the same settlor share the allowance.

Future pressure points include further anti-avoidance focus, more HMRC scrutiny of offshore and mixed-residence structures, and continuing interaction between CGT, IHT, BADR, and trust reporting.

Quick CGT pressure test

Illustrative only. It uses a 24% trustee rate and a default 2026/27 trust AEA of £1,500.

Effective tax on the gross gain. Add valuation, legal, IHT, and reporting costs separately.

Risk checklist

What to review before the fuse reaches the end

1. Read the deed before modelling the tax

Check beneficiary classes, powers to add beneficiaries, revocation powers, loan arrangements, and whether the settlor or spouse is excluded irrevocably or merely by current intention.

2. Model entry, inside, and exit separately

Entry may create an immediate market-value gain. Inside the trust, gains face trustee rules. Exit or appointment out can create another disposal, with hold-over relief depending on precise facts.

3. Coordinate CGT with income tax and IHT

Settlor-interested income can be taxed on the settlor, while IHT may treat the asset as reserved. The same structure can be inefficient for CGT even where it has a family or IHT rationale.

4. Get valuations and reporting dates in writing

For property and unquoted shares, robust valuations reduce dispute risk. For UK residential property, trustees should be ready for the 60-day reporting and payment timetable.

Summary of Key Insights

A settlor-interested trust does not provide the clean break many expect for CGT purposes. The combination of immediate or trapped gains on entry, higher flat-rate taxation inside the trust, restricted reliefs, and non-transferable losses creates a structural inefficiency that worsens as assets appreciate and tax rates remain elevated.

For business owners, landlords, and those with significant unrealised gains, the structure can still serve legitimate non-tax goals—particularly IHT planning where GWR is accepted or managed. However, it demands proactive management rather than set-and-forget. Regular reviews, especially around life events, trust variations, or proposed disposals, are the best defence against an expensive surprise when the bomb eventually detonates.

Taxpayers in this position should obtain specific advice tailored to the trust deed, asset mix, and family circumstances. The rules are technical, and small factual differences—such as the exact powers retained or the timing of appointments—can materially alter the outcome. HMRC guidance in the Capital Gains Manual and Trusts, Settlements and Estates Manual provides the authoritative baseline, but real cases often turn on detailed deed interpretation and anti-avoidance analysis.”

FAQs

Q1: Can a trust stop being settlor-interested part way through its life, and what does that mean for future CGT?

Well, it’s worth noting that yes, it can—usually by the settlor and their spouse or civil partner irrevocably excluding themselves from any possible benefit. In my experience with clients, this often happens during family restructuring or when the settlor’s circumstances change. For CGT going forward, the trust may escape some of the settlor-linked restrictions, but historic gains and any previous denial of hold-over relief on entry stay locked in. Always review the deed wording carefully; a poorly drafted exclusion can leave lingering risks.

Q2: What happens to CGT if residential property held in a settlor-interested trust is sold?

Residential property in these trusts often creates extra layers of complexity. Trustees face the 24% rate with a very limited annual exemption, and the 60-day reporting and payment window still applies. I’ve seen landlords in Manchester assume full Principal Private Residence relief would carry through seamlessly—only to find periods of trust ownership restrict it. If the property was let, you may lose relief for those years, pushing up the taxable gain significantly.

Q3: Is hold-over relief ever available on an exit from a settlor-interested trust?

In many cases it is, particularly under section 260 for chargeable transfers. This differs from entry, where it’s usually blocked. Consider a business owner in Birmingham whose family company shares sit in the trust: on appointment to adult children, hold-over can defer the gain into the beneficiaries’ hands. The key pitfall is ensuring the exit qualifies and that both trustees and the recipient sign the election properly. Miss this and the trust pays 24% immediately.

Q4: How do capital losses inside a settlor-interested trust interact with the settlor’s personal losses?

They generally don’t. Trust losses stay trapped and can only offset future trust gains. This asymmetry catches many self-employed clients who have personal losses from side ventures. In practice, I’ve advised coordinating sales across personal and trust portfolios in the same year where possible, but you can’t simply offset one against the other. Planning the order of disposals becomes crucial.

Q5: Does making the settlor a trustee create additional CGT problems?

Not automatically for CGT classification, but it can heighten scrutiny around whether the settlor truly has an interest. More practically, it complicates decision-making and record-keeping. One client, a freelancer with a property portfolio, found HMRC questioning the arm’s-length nature of decisions because the settlor-trustee also benefited indirectly. Clear minutes and separation of roles help.

Q6: What are the CGT implications when a settlor-interested trust becomes non-resident?

This is a major red flag. The move can trigger a deemed disposal at market value in many scenarios, crystallising gains at trust rates. Post-2025 rules have tightened reporting for offshore structures involving UK settlors. For high-earners with international ties, this “time bomb” can detonate expensively without specialist advice on the transitional rules.

Q7: Can Business Asset Disposal Relief (BADR) apply to gains realised inside the trust?

It’s limited. The trust itself doesn’t qualify in the same way an individual does, though on exit to a qualifying beneficiary, BADR may be available in the beneficiary’s hands if conditions are met. I’ve seen directors assume the trust would inherit the relief—only for it to be unavailable because the ownership tests look through differently. Early modelling of succession is essential for business owners.

Q8: How does the annual exempt amount work when the settlor has created multiple trusts?

It gets shared. With multiple settlements by the same settlor, the £1,500 (2026/27) exemption is divided, down to a £300 minimum per trust. This erodes the benefit quickly for families with several structures. A common mistake is overlooking older family trusts created years ago that still count in the group.

Q9: What should a self-employed contractor do if they want to transfer business assets into a trust without triggering immediate CGT?

In most settlor-interested cases, you can’t fully avoid it because hold-over is blocked on entry. Alternatives include using a non-settlor-interested structure (if the settlor steps away completely) or accepting the gain and using available reliefs or losses elsewhere. One Leeds-based IT contractor I advised restructured by first gifting to children directly before trust involvement, but this depends heavily on family dynamics and IHT goals.

Q10: Are there special rules for Scottish or Welsh residents with settlor-interested trusts?

The core CGT rules are UK-wide, but income tax interactions (since settlor-interested income is taxed on the settlor) can differ due to devolved rates. Scottish higher-rate taxpayers may find the combined tax burden heavier. Always cross-check your marginal rate when modelling distributions or gains that flow back.

Disclaimer

The information provided in this article is for general guidance only and is not intended to constitute professional advice, tax advice, financial advice, legal advice, or any other form of regulated guidance. Although every effort has been made to ensure accuracy at the time of publication, Fair View Accounting Services, including its director, employees, contractors, writers, and content-creation team, accepts no responsibility for any loss, damage, penalty, or consequence arising from reliance on the information contained herein.

UK tax legislation changes frequently, and HMRC interpretations, thresholds, and rules may vary depending on the individual circumstances of each taxpayer. Nothing in this article should be considered a substitute for obtaining formal, personalised advice from a qualified accountant or tax professional. Readers should not take action—or refrain from taking action—based solely on the content published on this website.

Fair View Accounting Services does not guarantee the completeness, accuracy, or ongoing validity of the information provided and assumes no liability for omissions or errors, whether typographical, factual, or technical. By using this content, the reader acknowledges that all responsibility for decisions remains solely with the user.