P11d For Beneficial Loans — The 2.25% Official Rate Trap

P11D for Beneficial Loans: The Official Rate Trap Directors Need to Understand

The official rate of interest for beneficial loans sat at 2.25% for several years — low enough that many directors and payroll teams stopped paying close attention to it. That changed sharply in April 2025, when the official rate of interest increased from 2.25% to 3.75%, its most significant jump in over thirty years. For anyone who borrowed from their company on the assumption that the tax cost of a beneficial loan was negligible, the arithmetic changed significantly.

Understanding the current rules, how the benefit is calculated, and what the combined personal and corporate tax cost actually looks like is now more important than it was when the rate was sitting at historic lows.

What the Official Rate Is and Why It Exists

The official rate of interest — also called the ORI — is set by Treasury Order and used by HMRC to calculate the taxable value of beneficial loan arrangements. When an employer or director’s own company provides a loan at below the official rate, or at zero interest, the interest that was not charged is treated as a benefit in kind. The employee or director is taxed on that notional interest as if it were employment income.

The ORI is used to calculate the taxable value of employment-related loans and some employer-provided living accommodation. The rate is normally fixed for a whole tax year but can be varied mid-year when there is a significant change in interest rates. From 6 April 2025, the previous public commitment that the ORI will not increase in-year no longer applies. The rate is now reviewed on a quarterly basis, and changes can occur following a quarterly review where appropriate.

This policy change is significant. For most of the period since the early 2000s, employers could rely on the ORI being fixed for a full tax year in advance — payroll calculations were straightforward and predictable. From April 2025 onwards, the rate may increase, decrease, or be maintained throughout the year, meaning mid-year adjustments are now possible. Employers with significant loan balances outstanding need to monitor quarterly announcements and update their benefit calculations accordingly.

The ORI for 2025/26 was 3.75%. The rate for 2026/27 is subject to the quarterly review process — any director or employer currently carrying a loan balance should verify the current rate through GOV.UK rather than relying on the prior year figure.

The £10,000 Threshold: Where the Rules Begin

Not every low-interest loan triggers a P11D filing or a benefit-in-kind charge. Any loan over £10,000 that charges less than the official rate can create a taxable benefit. Loans over £10,000 at any point in the tax year are treated as a benefit in kind and must be recorded at the end of the tax year on a P11D.

The threshold is cumulative across loans from the same employer to the same employee or director. Separate loan facilities that each stay just below £10,000 but collectively exceed that amount are aggregated for this purpose. HMRC’s guidance is explicit that the exemption applies to the aggregate of all outstanding qualifying loans, not to each loan individually.

Where the aggregate outstanding loan balance exceeds £10,000 at any point during the tax year — even briefly — the benefit calculation applies for the full tax year on the balance outstanding throughout. This is a common source of P11D errors: a director who repays a loan to bring it below £10,000 in March, but who had a balance above that threshold throughout the year, still generates a P11D benefit for the full year.

The Exemption for Qualifying Loans

Where the employer lends an employee more than £10,000, the taxable benefit is the difference between the official rate and the amount actually charged on the outstanding loan.

A loan at exactly the official rate, where the interest is charged and paid within the tax year, creates no taxable benefit. This is the primary mechanism for avoiding the benefit-in-kind charge: charge interest at no less than the ORI and ensure it is paid before the tax year ends. The interest paid by the director to the company is income of the company — included in corporation tax profits — but it eliminates the personal benefit-in-kind charge entirely.

Calculating the Taxable Benefit: Two Methods

HMRC permits employers to calculate the taxable value of a beneficial loan using either of two methods: the averaging method or the precise method.

The Averaging Method

The simpler of the two, this takes the average of the opening and closing loan balance for the tax year, applies the official rate to that average, and then deducts any interest actually charged and paid during the year.

Example:

- Loan balance at 6 April 2025: £80,000

- Loan balance at 5 April 2026: £60,000

- Average balance: £70,000

- ORI for 2025/26: 3.75%

- Notional interest at ORI: £70,000 × 3.75% = £2,625

- Actual interest charged and paid: £0

- Taxable benefit: £2,625

The averaging method is administratively simple and the default approach for most P11D submissions.

The Precise Method

This calculates the benefit on the actual daily balance throughout the year — more accurate where the balance changed significantly or where a partial interest payment was made at some point. Employees can elect to use this method if it produces a lower figure, which is useful where the loan was substantially higher at the start of the year than the end, or where repayments occurred in the early part of the year.

Employees may elect to use a more complex but accurate method of calculating the benefit from interest-free or low-interest loans. Where an election is made, the calculation must be done on a loan-by-loan basis rather than as an aggregate. GOV.UK

The Combined Tax Cost for Directors

For a director of an owner-managed company with a beneficial loan, the tax consequences fall in two places: personal income tax on the benefit in kind, and employer Class 1A NIC on the P11D value.

Employers providing beneficial loans are likely to see an increase in their Class 1A National Insurance Contributions for 2025/26 given the ORI increase. The Class 1A NIC rate which applies to taxable benefits also went up — from 13.8% in 2024/25 to 15% from April 2025. A higher NIC rate applies to a higher benefit-in-kind value.

For 2026/27, the Class 1A National Insurance rate on expenses and benefits is 15%. GOV.UK

The combined cost calculation for a director with a higher-rate income tax liability:

Beneficial loan of £80,000 at zero interest for full year (2025/26):

Item | Calculation | Amount |

Average balance | £80,000 | — |

Notional interest at 3.75% | £80,000 × 3.75% | £3,000 |

Director’s income tax at 40% | £3,000 × 40% | £1,200 |

Class 1A NIC (company pays) | £3,000 × 15% | £450 |

Total combined cost |

| £1,650 |

At the 2024/25 ORI of 2.25% and the 13.8% Class 1A rate, the equivalent total cost on the same loan would have been:

£80,000 × 2.25% = £1,800 benefit value. Director’s income tax: £720. Class 1A NIC: £248. Total: £968.

The combined cost has increased by approximately 70% due to the ORI increase and Class 1A rate rise — not because the loan arrangement changed, but because the rate environment did.

Directors and the Section 455 Charge: A Separate but Related Cost

For director-shareholders of close companies, a large outstanding loan balance carries a second tax consequence that operates alongside the P11D benefit charge. Proper accounting is essential — failing to record directors’ loans properly can result in HMRC reclassifying withdrawals as taxable income.

Section 455 of the Corporation Tax Act 2010 imposes a tax charge on the company equal to 33.75% of any loan to a participator (broadly, a shareholder with significant control) that is outstanding nine months after the end of the accounting period. This is a temporary charge: it is repaid to the company when the loan is repaid or written off. But it represents a significant cash-flow cost in the interim.

A director with a loan of £100,000 outstanding nine months after the year end faces:

- Personal P11D benefit charge on the notional interest each year

- Section 455 charge of £33,750 on the company — effectively an interest-free loan from HMRC at zero return for the company until repayment

The section 455 charge and the P11D benefit are separate calculations and both must be managed. A director who charges themselves interest at the ORI eliminates the P11D benefit but does not eliminate the section 455 charge, which applies regardless of the interest rate.

The Official Rate Trap

What directors and payroll teams must understand about the sudden shift in P11D beneficial loan calculations.

The Arithmetic Has Changed

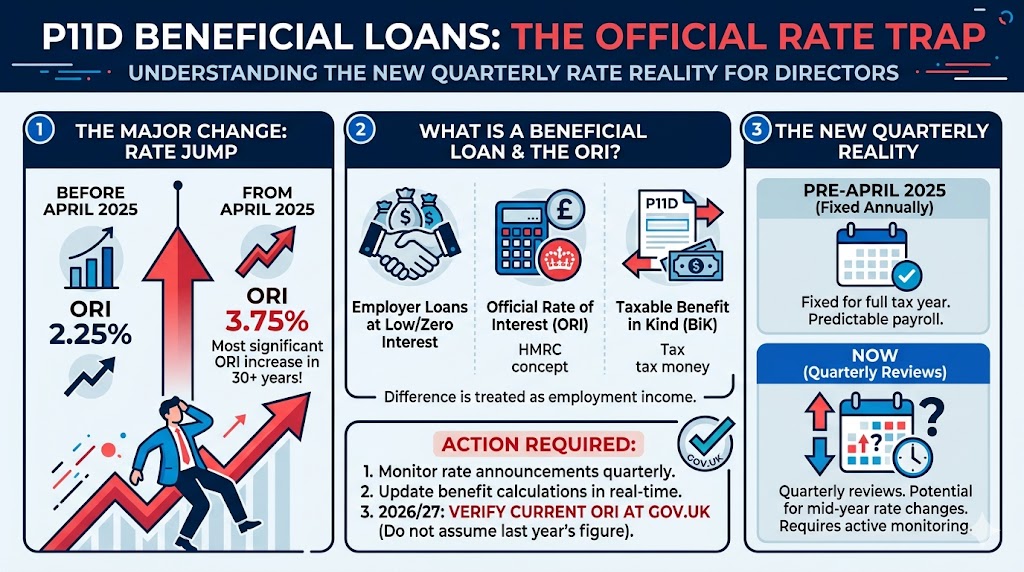

For several years, the Official Rate of Interest (ORI) for beneficial loans sat dormant at a comfortable 2.25%. It was low enough that many directors and payroll teams simply stopped paying close attention, assuming the tax cost of a beneficial loan was negligible. In April 2025, that assumption became a costly trap.

The Most Significant Jump in Over 30 Years

The chart visualizes the stark reality of the April 2025 update. The rate leaped from a static 2.25% to 3.75%. This is not a minor adjustment; it represents a massive proportional increase in the notional interest applied to beneficial loans.

Key Takeaway: The combined personal and corporate tax cost of borrowing from your own company is now substantially higher. Historic assumptions are no longer safe.

Understanding the ORI & Benefit in Kind

Before addressing the policy shift, it is crucial to understand the mechanics of the Official Rate of Interest and why HMRC monitors it so closely.

What is the ORI?

The Official Rate of Interest is set by Treasury Order. It serves as the baseline used by HMRC to calculate the taxable value of employment-related loans and some employer-provided accommodations.

The Loan Scenario

This applies when an employer, or a director's own company, provides a loan to an employee/director at an interest rate that is below the official rate, or at zero interest entirely.

The Taxable Benefit

The difference between the interest actually paid and the interest that would have been paid at the ORI is treated as a "Benefit in Kind". The individual is taxed on this notional interest as if it were standard employment income.

The Structural Policy Shift: Goodbye Predictability

The rate increase is only half the story. The underlying mechanism for how the rate is applied throughout the year has undergone a fundamental transformation, disrupting decades of payroll predictability.

Pre-April 2025

📅- ✓ Fixed Annually: Employers could rely on the ORI being locked in for a full tax year in advance.

- ✓ Predictable: Payroll calculations were straightforward, requiring no mid-year adjustments for rate changes.

- ✓ Public Commitment: HMRC previously committed that the ORI would not increase in-year.

From April 2025 Onwards

⚠️- ❗ Quarterly Reviews: The rate is now actively reviewed on a quarterly basis.

- ❗ Mid-Year Adjustments: Changes (increases, decreases, or maintenance) can occur during the tax year following reviews.

- ❗ Active Monitoring Required: Employers with significant loan balances must constantly monitor announcements and update benefit calculations accordingly.

Action Required for 2026/27

Because the rate is now subject to ongoing quarterly reviews, you cannot rely on the prior year figure.

Payrolling Benefits: An Alternative to P11D for Beneficial Loans

Since April 2016, employers have been able to payroll certain benefits in kind — reporting them through the real-time payroll process rather than through a year-end P11D. From April 2026, payrolling of benefits became mandatory for most new benefit arrangements, with a transition period for existing P11D filers.

Beneficial loans can be payrolled, but the practical challenge is that the benefit value is not precisely known until the loan balance and any interest payments for the full tax year are established. For employers using the averaging method, the mid-year estimate is used and then adjusted at year end. For those using the precise method, a month-by-month calculation is required.

Where beneficial loans are payrolled, the tax is collected through PAYE throughout the year rather than through a Self Assessment adjustment or a coding notice adjustment. For directors who use Self Assessment — as most director-shareholders do — the payrolled benefit reduces the need for a year-end adjustment, but the benefit must still be disclosed in the Self Assessment return alongside any other benefits.

Where an employer has not registered for payrolling and continues to use P11D, the benefit is reported by 6 July following the tax year end. The hard deadline to submit P11D forms for the previous tax year is 6 July. Class 1A NIC is due by 22 July if paying electronically. If the return is late, HMRC can impose a penalty of £100 per 50 employees for every month the form is late.

For a small owner-managed business where the director is the only P11D recipient, a single late filing generates a £100 penalty per month — not catastrophic, but avoidable.

What Happens If the ORI Changes Mid-Year

The removal of the guarantee that the ORI will not increase in-year creates a planning uncertainty that was not present before April 2025. The rate may increase, decrease, or be maintained throughout the year, with any changes occurring following a quarterly review.

For employers using the averaging method, a mid-year ORI change complicates the calculation. Where the rate changes partway through the year, the benefit must be calculated using the rates that applied for each period separately — effectively treating the year as two or more distinct calculation periods.

For employers who have set an internal interest charge on the director’s loan at the rate prevailing at the start of the year, a mid-year ORI increase may push the charged rate below the new ORI — inadvertently creating a benefit-in-kind that was not anticipated. Loan agreements should be reviewed to ensure any interest rate provision can be adjusted to track the ORI if it changes during the year.

Where a director has agreed to pay interest at a fixed rate and the ORI rises above that rate mid-year, the gap between the agreed rate and the new ORI generates a benefit. The director would need to pay additional interest to close the gap, or accept the benefit charge — and the P11D reporting obligation — on the differential.

Scottish Taxpayers and the Benefit Calculation

The P11D benefit value is the same regardless of whether the director or employee lives in Scotland. The ORI, the calculation method, and the threshold all apply uniformly across the UK.

What differs for Scottish taxpayers is the income tax rate applied to the benefit value. Scottish income tax rates for non-savings income are higher than rest-of-UK rates above the Basic rate — at the Higher rate, Scotland charges 42% compared to England’s 40%.

For a Scottish director with a £80,000 beneficial loan generating a £3,000 P11D benefit, the income tax cost at 42% is £1,260 — compared to £1,200 for an English director at 40%. The difference is modest at this level, but for a director with a much larger loan — say £300,000 — the annual P11D benefit at 3.75% is £11,250, and the income tax at 42% rather than 40% costs an additional £225 per year compared to a director south of the border on the same figures.

Class 1A NIC is paid by the employer at the UK-wide 15% rate regardless of where the director lives.

The Interest Charge Strategy: When It Makes Sense to Charge Interest

Charging the director interest at the ORI eliminates the P11D benefit entirely. No benefit-in-kind. No personal income tax. No Class 1A NIC for the company. The director pays interest to the company, and the company declares that interest as income.

The question is whether this is the right economic choice. The interest paid to the company is taxed at the corporation tax rate — either 19% or 25% depending on profit levels. The director’s personal income tax on the same sum (if they took it as a dividend instead) would typically be at the dividend higher rate of 35.75%. On a strict comparison, having the company receive interest at corporation tax rates is less efficient than distributing profits as dividends.

But the comparison is not quite that clean. The interest eliminates a benefit-in-kind charge that would be taxed as employment income (not dividend income). The director’s income tax on the P11D benefit is at 40% or 42%, compared to 35.75% on a dividend. So charging interest eliminates income tax at 40-42% but creates corporation tax income at 19-25%. The net saving depends on the specific rates.

Scenario | Tax Cost |

£3,000 P11D benefit, 40% income tax + 15% Class 1A NIC | £1,200 + £450 = £1,650 total |

Interest of £3,000 charged to director, 25% corporation tax on interest income | £750 |

Net saving from charging interest | £900 |

For most directors paying corporation tax at 25%, charging interest at the ORI saves approximately £900 per £3,000 of notional benefit — a meaningful amount where loan balances are large.

The practical complication is the section 455 charge on participator loans. That charge applies regardless of whether interest is charged. So the comparison above addresses only the P11D and income tax dimension, not the section 455 cost which must also be managed.

Common Errors in P11D Beneficial Loan Reporting

Failing to aggregate multiple loans. Where a director has drawn multiple amounts from the company at different times — sometimes with partial repayments in between — the £10,000 threshold applies to the aggregate outstanding balance across all loans at any point during the year. Treating each drawing as a separate sub-£10,000 loan to avoid the threshold is not compliant.

Using the wrong ORI for calculations. The ORI is specific to each tax year and, from April 2025, may change mid-year. Using last year’s rate in the current year’s calculation generates an incorrect benefit value — either under-reported or over-reported. The current rate must be verified each year, and any mid-year change must be incorporated.

Not reporting loans that were outstanding for only part of the year. If a director had a loan of £50,000 from April to October and repaid it fully in November, the benefit still arose for the seven-month period it was outstanding. Failure to report this on the P11D because the balance is nil at year end is a compliance error.

Ignoring the interest actually charged but not paid. Interest that is charged on paper but not actually paid within the tax year does not count as reducing the benefit. The deduction for interest charged requires that the interest is genuinely paid within the tax year — accrued but unpaid interest does not qualify.

Omitting the P11D(b) when there is a Class 1A NIC liability. The P11D reports the benefit to HMRC and the employee. The P11D(b) — the employer’s return — aggregates the Class 1A NIC obligation across all benefits. Where a P11D is filed but the P11D(b) is omitted or incorrect, the Class 1A NIC is not properly settled.

P11D for Beneficial Loans

The 2.25% → 3.75% Official Rate Trap

For years the official rate sat quietly at 2.25%. In April 2025 it leapt to 3.75% — its biggest jump in over three decades — and the Class 1A NIC rate rose to 15%. The cost of a cheap director’s loan changed overnight. Here’s what it means for 2026/27.

What the Official Rate is — and why it suddenly matters

The Official Rate of Interest (ORI) is set by Treasury Order and used by HMRC to value cheap or interest-free loans an employer or a director’s own company provides. Where a qualifying loan is charged below the ORI, the un-charged interest is treated as a benefit in kind and taxed as if it were employment income.

The big shift: from 6 April 2025 the long-standing promise that the rate would never rise mid-year was scrapped. The ORI is now reviewed quarterly and can increase, decrease or hold — with any in-year change taking effect on 6 July, 6 October or 6 January. For 2026/27 it has been confirmed at 3.75%, but that is no longer guaranteed for the whole year.

2026/27 quarterly review points — verify the live rate each quarter on GOV.UK:

Beneficial loan calculator (averaging method)

Enter the loan balances and any interest you actually paid in the year. The widget applies the ORI to the average balance, deducts interest paid, then shows the personal income tax and the company’s Class 1A NIC. Change the ORI box to model a mid-year rate move.

The £10k threshold & the two calculation methods

A P11D charge only bites once the aggregate of all loans from the same employer tops £10,000 at any point in the year — even briefly. Repaying below £10k in March doesn’t erase a benefit that arose earlier. You then pick one of two methods.

Takes the average of the opening and closing balance, applies the ORI, then deducts interest paid. Simple and the default on most P11Ds.

Open £80,000 · Close £60,000 → average £70,000

£70,000 × 3.75% = £2,625 notional interest

Interest paid £0 → taxable benefit £2,625

Works on the actual daily balance throughout the year. More accurate where the balance changed sharply or repayments fell early in the year. The employee (or HMRC) can elect for it if it gives a lower figure — but it must be done loan-by-loan, not on the aggregate.

Best when: a large loan was repaid early in the year, so the average overstates the true cost of credit.

Aggregation: several sub-£10k drawings from the same company are added together — you can’t slice a £15k loan into two £7.5k loans to dodge it.

Part-year loans still count: a £50k loan held Apr–Oct then repaid is reportable for the months it existed, even if the year-end balance is nil.

Charged ≠ paid: interest written into the ledger but not actually paid within the tax year does not reduce the benefit.

How much more it costs now — the same £80k loan

Nothing about the loan changed — only the rate environment. The combined tax cost on an interest-free £80,000 loan has risen roughly 70%.

Based on £80,000 interest-free for the full year at a 40% income tax band. The BIK cost is flat between 2025/26 and 2026/27 because the ORI held at 3.75% — but the Section 455 and dividend costs around it rose for 2026/27 (see below).

The separate Section 455 charge — and its 2026/27 rise

For director-shareholders of close companies a second, larger charge sits alongside the P11D benefit. If a loan to a participator is still outstanding nine months and one day after the accounting period ends, the company pays Section 455 tax on it. It’s refundable once the loan is repaid (form L2P) — but it’s a real cash cost in the meantime, and it applies whether or not you charge interest.

New for 2026/27: because S455 is pinned to the dividend upper rate, it rose from 33.75% to 35.75% for loans advanced on or after 6 April 2026. Loans made before that date keep the 33.75% rate.

Should you charge interest at the ORI?

Charging interest at (or above) the ORI and actually paying it within the year removes the P11D benefit entirely — no BIK, no personal income tax, no Class 1A NIC. The interest becomes company income taxed at corporation tax rates. On a £3,000 notional benefit for a 40% taxpayer:

Leave it interest-free

Income tax £1,200 (at 40%) + company Class 1A NIC £450 (at 15%). Plus the P11D reporting obligation each year.

Charge interest at the ORI

£3,000 interest paid to the company, taxed as company income at 25% corporation tax. No BIK, no NIC, no P11D for the loan benefit.

Note: from 6 April 2026 the dividend upper rate is 35.75% (additional rate 39.35%), so the salary/dividend/loan mix is more finely balanced than before. And remember — charging interest does nothing for the Section 455 charge above. The numbers shift with your corporation tax rate (19% or 25%) and income band, so model your own figures.

Payrolling & reporting — what’s actually changed

Important update: mandatory payrolling of benefits in kind was originally trailed for April 2026 but has been delayed to 6 April 2027. Crucially, employment-related loans (and living accommodation) are excluded from mandatory payrolling for now — so for beneficial loans the P11D / P11D(b) route continues through 2026/27 and beyond. Employers may still payroll loans voluntarily if they register before the tax year starts.

Five mistakes that trigger HMRC corrections

Key takeaways for 2026/27

ORI is 3.75% for 2026/27 (confirmed from 6 Apr 2026) but reviewed quarterly — it can now move mid-year.

Loans over £10k (aggregate, any point) create a P11D benefit — the gap between ORI and interest paid.

Class 1A NIC stays at 15%, payable by the company on the benefit value.

Charge ORI interest, paid in-year, to wipe out the P11D benefit — often cheaper for larger loans.

Section 455 rose to 35.75% for new loans from 6 Apr 2026 — a separate, larger, refundable charge.

P11D continues for loans — mandatory payrolling (Apr 2027) excludes loans & accommodation.

This widget is a general explainer for the UK 2026/27 tax year and is not personal tax advice. Rates and rules change — in particular the ORI can be revised quarterly. Always confirm the live figure on GOV.UK (search “Rates and allowances: beneficial loan arrangements”) and take advice on your own circumstances. Estimates use simplified assumptions and round figures.

Key Takeaways

- The official rate of interest for beneficial loans increased from 2.25% to 3.75% from 6 April 2025 — its most significant rise in over thirty years. Combined with the Class 1A NIC rate increase to 15%, the cost of low-interest director loans has risen substantially.

- From April 2025, the ORI can change mid-year following quarterly reviews. Employers with significant loan balances must monitor the ORI quarterly and update their benefit calculations if the rate moves.

- Loans over £10,000 at any point during the tax year create a P11D benefit-in-kind, calculated on the difference between the ORI and any interest actually charged and paid. The threshold applies to the aggregate of all loans from the same employer.

- Charging interest at the ORI and paying it within the tax year eliminates the P11D benefit entirely. For directors with larger loans and companies paying corporation tax at 25%, this approach typically produces a lower combined tax cost than leaving the loan interest-free and accepting the P11D charge.

- Class 1A NIC at 15% is payable by the employer on the P11D benefit value. For 2026/27 this rate remains at 15%. UK

- The section 455 charge on loans to participators applies regardless of interest rate and represents a separate — and often larger — tax cost than the P11D benefit. Both must be managed together for any director with a substantial outstanding loan account.

- P11D forms must be submitted by 6 July following the tax year end. Class 1A NIC is due by 22 July. Late filing penalties are £100 per 50 employees per month.

FAQs

Q1: What should a company director do if their overdrawn loan account has fluctuated above and below £10,000 during the tax year?

A1: Well, it’s worth noting that the £10,000 threshold is tested at any point during the year. In my experience with clients running family businesses, many get caught out by short-term peaks. Even if the balance ends the year below the limit, if it exceeded £10,000 at any time and interest charged was below the official rate, a P11D entry is usually required. Keep detailed monthly reconciliations to support your position if HMRC queries it.

Q2: Can a beneficial loan be payrolled instead of reported on a P11D?

A2: Generally no for most beneficial loans. Unlike many other benefits, these (along with accommodation) cannot usually be included in voluntary payrolling. You’ll still need to report the cash equivalent on form P11D and settle the Class 1A National Insurance on P11D(b). I’ve seen several directors assume payrolling covers everything—it’s a common mix-up that leads to late filing penalties.

Q3: How does the official rate change mid-year affect beneficial loan calculations for P11D?

A3: Since quarterly updates were introduced, you may need to split the year into periods and calculate the benefit separately for each. This adds complexity. One client with a large bridging loan had to rework their figures when the rate rose. Always check the latest HMRC table before finalising P11Ds, especially if your loan spans rate changes.

Q4: Does a loan to a director’s adult child trigger the beneficial loan rules?

A4: Yes, if it’s provided because of the director’s employment or directorship. HMRC can treat it as a benefit to the director. I’ve advised several clients in the Midlands who helped their children with house deposits through the company— these arrangements need careful documentation to avoid unexpected tax charges on the parent.

Q5: What happens if a beneficial loan is written off after the tax year but before P11D submission?

A5: The write-off is normally treated as earnings in the year it happens, separate from the beneficial loan charge. This can create a double hit in some cases. In practice, timing these decisions thoughtfully with your accountant can help manage cash flow and tax exposure.

Q6: Are there special rules for beneficial loans in Scottish or Welsh resident employees?

A6: The benefit calculation and P11D reporting remain the same UK-wide, but Scottish income tax rates may mean a higher or different personal tax bill on the benefit. Welsh residents follow the same income tax bands as England. Always factor in the individual’s marginal rate when advising on the net cost.

Q7: Can a self-employed contractor receive a beneficial loan from a client without P11D implications?

A7: If they’re genuinely self-employed rather than an employee or office holder, the employment benefit rules usually don’t apply. However, it could still have corporation tax or disguised remuneration implications for the payer. I’ve seen grey-area contractor relationships where HMRC later reclassified them—substance over form is key.

Q8: How long should records of beneficial loans be kept for P11D purposes?

A8: At least six years from the end of the relevant tax year, in my view. Detailed loan agreements, interest payment records, and balance histories have saved several of my clients during enquiries. Digital records with clear dates work well, but make sure they’re easily accessible.

Q9: Does taking a beneficial loan affect an employee’s ability to claim tax reliefs elsewhere?

A9: It shouldn’t directly, but the additional taxable income from the benefit can push someone into a higher tax band, affecting things like personal allowances or pension contributions. One high-earning client in London found their student loan repayment threshold impacted indirectly.

Q10: What if interest is charged on the loan but paid after the tax year end?

A10: For the beneficial loan charge, it’s the interest actually charged (and due) during the year that counts. Late payment might not help for that year’s calculation. I recommend clients set up standing orders to ensure interest is paid on time each year.

Disclaimer

The information provided in this article is for general guidance only and is not intended to constitute professional advice, tax advice, financial advice, legal advice, or any other form of regulated guidance. Although every effort has been made to ensure accuracy at the time of publication, Fair View Accounting Services, including its director, employees, contractors, writers, and content-creation team, accepts no responsibility for any loss, damage, penalty, or consequence arising from reliance on the information contained herein.

UK tax legislation changes frequently, and HMRC interpretations, thresholds, and rules may vary depending on the individual circumstances of each taxpayer. Nothing in this article should be considered a substitute for obtaining formal, personalised advice from a qualified accountant or tax professional. Readers should not take action—or refrain from taking action—based solely on the content published on this website.

Fair View Accounting Services does not guarantee the completeness, accuracy, or ongoing validity of the information provided and assumes no liability for omissions or errors, whether typographical, factual, or technical. By using this content, the reader acknowledges that all responsibility for decisions remains solely with the user.