Health Insurance Through Your Ltd — Tax Cost Vs Personal Premium

Health Insurance Through Your Ltd — Tax Cost vs Personal Premium in the UK

Private medical insurance (PMI) remains a popular consideration for directors and business owners of limited companies. The choice between having the company pay for it or funding it personally involves more than just cash flow. It requires weighing corporation tax relief against benefit-in-kind (BIK) charges, National Insurance, reporting obligations, and cash timing.

How the Rules Work in 2026/27

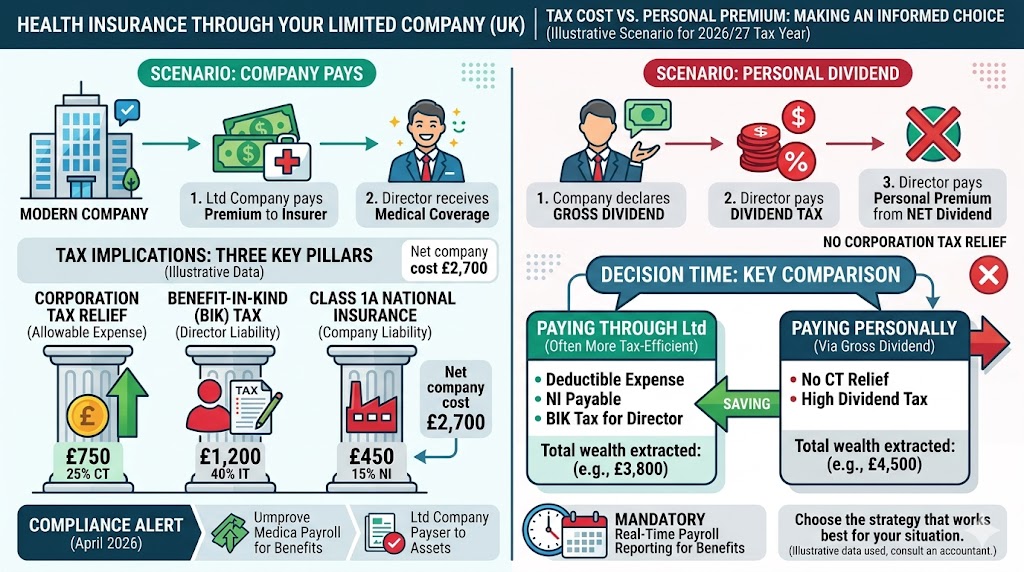

When a limited company pays PMI premiums for a director or employee, HMRC treats the cost as an allowable business expense, provided it meets the “wholly and exclusively” test for the trade. This is usually straightforward for director cover in a small Ltd. The company deducts the premium when calculating its taxable profits.

Corporation tax relief applies at the company’s marginal rate: 19% for profits under £50,000, 25% for profits over £250,000, or a tapered effective rate in between via marginal relief. Most growing Ltd companies sit closer to the 25% end.

However, the premium counts as a taxable benefit in kind for the recipient. The value of the benefit is generally the premium paid (or the cost to the company). The director pays income tax on this at their marginal rate — 20%, 40%, or 45% (plus any Scottish variations if applicable).

The company must also pay Class 1A National Insurance Contributions on the BIK value. This rate stands at 15% following the April 2025 increase.

Reporting changes matter. From April 2026, HMRC has moved most taxable benefits, including PMI, toward real-time payrolling rather than relying solely on end-of-year P11D forms. Employers should ensure their payroll systems handle this to avoid compliance issues or double taxation in the transition year.

Net Cost Comparison: Company vs Personal

Assume a typical family PMI policy costing £3,000 a year (premiums vary widely by age, location, and cover level; use real quotes for accuracy).

Scenario 1: Company pays the premium

- Company deducts £3,000 → Corporation tax saving of £750 (at 25%).

- Net cost to company before NI: £2,250.

- Company pays Class 1A NIC: 15% of £3,000 = £450.

- Total cost to company: £3,000 – £750 CT relief + £450 NI = £2,700.

- Director pays income tax on £3,000 BIK at marginal rate.

- Basic rate taxpayer: £600 extra tax.

- Higher rate: £1,200 extra tax.

- Additional rate: £1,350 extra tax.

Effective net cost to the household (company money is ultimately the director’s) depends on extracting funds anyway. The company route often wins where profits would otherwise be taxed at 25% before dividend extraction.

Scenario 2: Director pays personally

- Pay £3,000 from after-tax income.

- No corporation tax relief.

- No Class 1A NIC.

- No BIK reporting.

For a higher-rate taxpayer extracting profits via dividends, the personal route requires more pre-tax profit to net £3,000 after all taxes. The company route leverages the deduction at source.

Health Insurance Through Your Ltd Company

Weighing Corporation Tax relief against BIK charges and NI. Should the company pay, or should you fund it personally?

The Core Dilemma

Private medical insurance (PMI) is a highly valued benefit for company directors. However, deciding who pays the premium involves complex tax calculations. When a limited company pays, it's an allowable business expense, but it triggers personal Income Tax and company National Insurance liabilities.

📈 Corporation Tax Relief

HMRC treats PMI as a deductible expense. The company saves Corporation Tax at its marginal rate (19% for profits under £50k, up to 25% for profits over £250k).

📉 The Hidden Tax Burden

The premium is a Benefit-in-Kind (BIK). The director pays Income Tax on the premium value, and the company must pay Class 1A NI at 15% (updated April 2025).

Crucial 2026 Reporting Shift

Real-time Payrolling is mandatory. From April 2026, HMRC is moving away from end-of-year P11D forms for most taxable benefits, including PMI. Employers must ensure payroll systems are updated to handle real-time processing to avoid severe compliance penalties or transition-year double taxation.

Net Cost Comparison: A £3,000 Policy Example

Assume a £3,000 annual family PMI premium, a company paying 25% Corporation Tax, and a director in the 40% higher rate Income Tax bracket. Which method requires extracting less total wealth from the company?

Worked Example: Higher-Rate Director (25% CT)

Company profit before decision: enough to cover the premium.

Company pays:

- CT relief: £750.

- Class 1A: £450.

- Director’s extra income tax (40%): £1,200.

- Combined tax & NI cost: £1,200 (income tax) + £450 (Class 1A) – £750 (CT) = £900.

- Net economic cost for £3,000 cover: £900 + any cash flow timing.

Personal pays:

- To have £3,000 after higher-rate tax and dividend tax, the company needs to generate significantly more profit (subject to CT then dividend tax).

The company route typically reduces the effective cost by 10-30% depending on exact tax bands, though the Class 1A adds friction. Lower-rate taxpayers see smaller relative savings, and the admin may not justify it.

Nuances and Common Pitfalls

Director-only policies — These are common in one- or two-person companies and remain fully allowable, but HMRC scrutinises whether the cover serves a genuine business purpose (e.g., key person protection or reducing absenteeism). Purely personal cover still qualifies in practice for most small Ltds, but documentation helps.

Family cover — Including spouse and children increases the BIK value proportionally. The full premium paid by the company becomes the taxable amount for the director.

Salary sacrifice or payrolling — Some structures allow salary sacrifice for PMI, potentially saving employer and employee NI in specific cases, though the 2025 NI changes altered the maths. Professional advice is essential.

Landlords and multiple income sources — If you have rental income or other sources, the BIK could push you into a higher band or affect personal allowance taper. Scottish taxpayers face different bands, which can alter the comparison.

Sole traders and partnerships — No equivalent CT relief. Premiums are generally not deductible as a business expense for the self-employed when covering themselves (distinct from employee cover).

Timing and cash flow — Company payment uses pre-tax pounds immediately. Personal payment uses post-tax pounds, often extracted via dividend (extra tax and timing). Late-year decisions can miss full-year relief.

Overlooked costs — P11D (or payrolling) compliance, potential accountant fees, and Insurance Premium Tax (IPT) on the policy itself (standard rate applies).

Common mistakes —

- Assuming full tax-free treatment.

- Forgetting Class 1A NIC.

- Not updating payroll for 2026 changes.

- Claiming personal medical costs directly through the company (generally not allowed; insurance premiums are the route).

When It Makes Sense

The company route often stacks up better for:

- Higher-rate or additional-rate directors with profits taxed at or near 25%.

- Businesses wanting to attract or retain staff with competitive benefits.

- Situations where speedy access to private care reduces business disruption.

It makes less sense for basic-rate only taxpayers with low profits (19% CT but full personal tax still applies) or where admin burden outweighs savings.

Less obvious angles — In multi-director companies, unequal cover can create fairness or discrimination issues. For contractors with IR35 concerns, ensure the benefit does not complicate status assessments. If selling the company, benefits structures rarely affect goodwill materially but should be clean.

Always model your exact numbers. A £2,000–£5,000 annual premium changes the equation differently than a £10,000+ executive policy. Use current quotes and run scenarios with your accountant.

Health Insurance Through Your Ltd

Tax Cost vs Personal Premium • UK 2026/27Interactive comparison for Ltd directors. Models real-time payrolling, Class 1A NIC, CT relief, and dividend extraction.

🏢 Company Route

👤 Personal Route

How the Rules Work (2026/27) UPDATED

When a Ltd pays PMI premiums for a director, HMRC generally allows it as a deductible business expense (passing the "wholly and exclusively" test). However, it triggers specific tax events:

- Corporation Tax Relief: Applied at your company's marginal rate (19% under £50k profits, 25% over £250k, or tapered via marginal relief).

- Benefit-in-Kind (BIK): The full premium is taxable income for the director at their marginal rate (20%, 40%, or 45%).

- Class 1A NIC: The company pays 15% on the BIK value (increased from April 2025).

- Real-Time Payrolling From April 2026, HMRC expects most taxable benefits (including PMI) to be processed through payroll monthly/quarterly rather than year-end P11Ds. Ensure your software is updated to avoid compliance penalties. replaces traditional P11D reporting for most SMEs.

Nuances & Common Pitfalls

- Family Cover: Including spouses/children increases the BIK proportionally. The full company-paid premium becomes taxable.

- Sole Traders: Cannot claim personal PMI as a business expense. Ltd structure is required for CT relief.

- Timing & Cash Flow: Company route uses pre-tax pounds immediately. Late-year setup may miss full-year relief.

- Common Mistakes: Assuming full tax-free treatment, ignoring Class 1A NIC, failing to update payroll for 2026 real-time rules, or claiming treatment costs directly (not allowable).

When It Makes Sense

- ✅ Higher/Additional rate directors with company profits near the 25% CT bracket.

- ✅ Businesses using benefits to attract/retain key talent or reduce operational disruption.

- ❌ Less efficient for Basic Rate directors on low profits (19% CT vs 20% IT + 15% NIC creates minimal/negative net benefit).

- ⚠️ IR35/Contractors: Ensure benefits don't inadvertently signal "employment" status to HMRC.

Key Takeaways

Tax arbitrage exists but is reduced by Class 1A NIC and personal BIK tax. Net savings are real for most Ltd directors but not automatic. 2026 payrolling changes increase compliance importance. Always model exact numbers, obtain current premium quotes, and verify treatment with your accountant before implementation.

Key Takeaways

- Tax arbitrage exists but is reduced by Class 1A NIC and personal income tax on the BIK. Net savings are real for most Ltd directors but not automatic.

- 2026 payrolling changes increase the importance of correct payroll setup — plan ahead to avoid penalties or cash flow surprises.

- Company payment usually beats personal funding for higher-rate taxpayers due to corporation tax relief, but quantify your marginal rates, NI exposure, and admin costs.

- Rules are clear from HMRC guidance, yet real-world application benefits from tailored advice, especially with family cover, multiple income streams, or transitional reporting issues.

Consult your accountant or tax adviser before implementing. Tax rules, rates, and individual circumstances interact in ways a general article cannot fully capture. Premiums and cover levels change; always obtain current quotations and verify treatment for your specific situation. This is not personalised advice.

FAQs

Q1: Can a single-director limited company legitimately pay for private medical insurance without it looking like a personal perk to HMRC?

Well, in my experience advising many one-person Ltds, yes it can, provided the policy is in the company’s name and treated as a business expense. The key is documenting a clear business rationale, such as protecting key person continuity or reducing potential downtime from health issues. I’ve seen clients in tech or consulting where this holds up well on review. Just ensure it’s not mixed with purely personal reimbursements.

Q2: What happens if the company pays for family cover including spouse and children – does the BIK only apply to the director’s portion?

No, the full premium paid by the company typically becomes a taxable benefit in kind for the director. In practice with clients who have growing families, this can push the total BIK value higher and affect marginal tax rates more noticeably. It is worth modelling the exact split versus separate personal policies, as the company route still often nets better after corporation tax relief, but the personal tax hit scales with the whole amount.

Q3: How do the 2026 real-time payrolling changes for benefits in kind affect someone adding PMI mid-tax year?

From April 2026, most benefits like PMI need handling through payroll in real time rather than just year-end P11D. In my work with clients, this means your payroll provider must update your tax code promptly to avoid under-deducting tax and a surprise bill later. If you’re adding cover part-way, plan the timing carefully – I’ve seen transitional double-taxation risks in the first year for those who delay setup.

Q4: Is there any way for a higher-rate taxpayer to minimise the income tax on company-paid PMI through salary sacrifice?

Salary sacrifice for PMI is possible in some setups but less straightforward than for pensions. With several clients, we’ve found it can save employer and employee National Insurance in specific cases, though the 2025 NI rate changes altered the maths. It requires careful structuring and professional advice to avoid HMRC challenges – it’s not a blanket solution.

Q5: As a Scottish taxpayer running a Ltd company, does the BIK from PMI get taxed differently compared to the rest of the UK?

Yes, Scottish income tax bands and rates apply to the BIK value. For higher earners in the Scottish higher or additional rates, this can increase the personal tax cost slightly compared to England or Wales. I’ve advised several Edinburgh-based directors where the difference was material enough to tip the comparison toward personal payment in lower-profit years.

Q6: What if my company is loss-making – does it still make sense to route PMI through the Ltd?

Corporation tax relief has limited immediate value if you’re not profitable. In such cases with clients, we’ve often recommended personal payment to preserve cash, then revisit once profits return. However, carrying forward losses can still interact usefully in future years, so it’s worth running the projections rather than dismissing the company route outright.

Q7: Can landlords who also run a Ltd company use the business to cover health insurance related to their property activities?

Generally no for the rental side directly, as property letting is usually treated separately. But if you’re a director with operational involvement in the Ltd (perhaps a property management company), the cover can relate to that trade. I’ve seen confusion here with mixed-income clients – keep clear separation to avoid queries on the “wholly and exclusively” test.

Q8: How does company-paid PMI interact with IR35 for contractors?

It can be a double-edged sword. Providing benefits like PMI might strengthen an “inside IR35” argument if it looks like disguised employment. Conversely, for those comfortably outside, it’s a standard perk. In my experience reviewing contractor situations, document it as a genuine business decision and ensure consistency with your overall working practices.

Q9: What are the reporting obligations if I switch from personal to company-paid PMI halfway through the year?

You’ll need to notify your payroll of the new benefit for real-time reporting under the 2026 rules. Failure here can lead to incorrect tax codes and penalties. One client in Manchester switched in January and had to back-adjust – it was manageable but required quick accountant input to avoid over or underpayment.

Q10: Does taking company PMI affect my ability to claim other medical-related tax reliefs or benefits?

It doesn’t directly block personal reliefs, but the BIK increases your taxable income, which could taper your personal allowance or affect means-tested benefits. For high earners near thresholds, I’ve seen this create unexpected interactions with things like the high income child benefit charge.

Q11: Is health cash plan cover treated the same way as full private medical insurance for tax purposes?

Health cash plans often fall under similar BIK rules when company-funded, though the exact treatment can vary by scheme. With several small business clients, the lower cost makes the tax friction more noticeable proportionally. Always check the specific policy wording against HMRC guidance.

Q12: What should a freelancer who has recently incorporated do about existing personal PMI?

Consider transferring or taking out a new company policy. Cancelling personal cover and starting fresh via the Ltd can unlock corporation tax relief, but watch for any waiting periods or pre-existing condition exclusions. I’ve guided several new incorporations through this – timing it at incorporation often works smoothly.

Disclaimer

The information provided in this article is for general guidance only and is not intended to constitute professional advice, tax advice, financial advice, legal advice, or any other form of regulated guidance. Although every effort has been made to ensure accuracy at the time of publication, Fair View Accounting Services, including its director, employees, contractors, writers, and content-creation team, accepts no responsibility for any loss, damage, penalty, or consequence arising from reliance on the information contained herein.

UK tax legislation changes frequently, and HMRC interpretations, thresholds, and rules may vary depending on the individual circumstances of each taxpayer. Nothing in this article should be considered a substitute for obtaining formal, personalised advice from a qualified accountant or tax professional. Readers should not take action—or refrain from taking action—based solely on the content published on this website.

Fair View Accounting Services does not guarantee the completeness, accuracy, or ongoing validity of the information provided and assumes no liability for omissions or errors, whether typographical, factual, or technical. By using this content, the reader acknowledges that all responsibility for decisions remains solely with the user.