Inside IR35 Vs Umbrella , Take-Home Comparison At £500/Day

Inside IR35 vs Umbrella: Take-Home Comparison at £500/Day

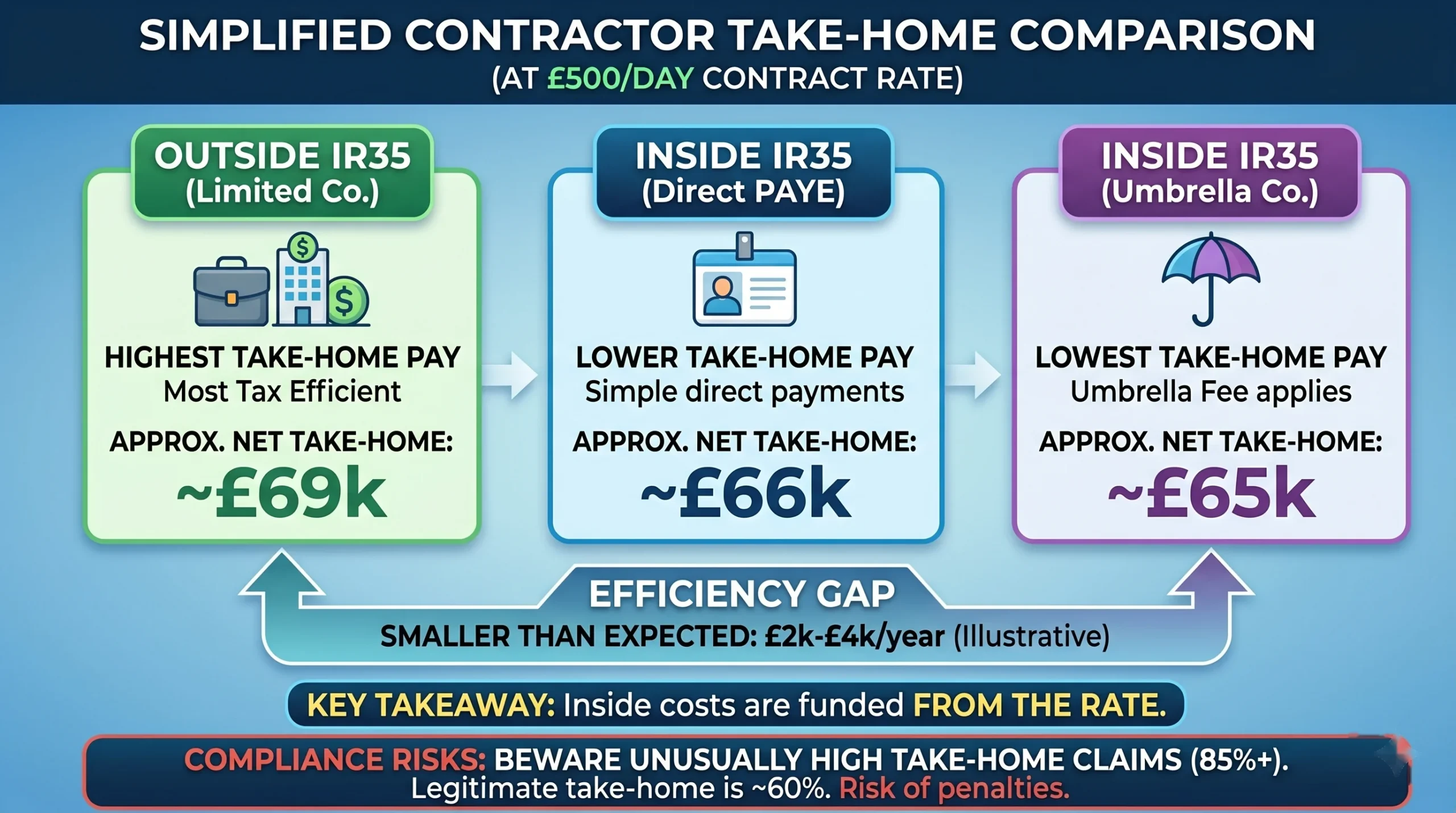

For contractors receiving an inside IR35 determination and wondering whether to work through the fee-payer’s PAYE arrangement or join an umbrella company, the financial difference between the two options is often smaller than expected , and sometimes the umbrella route is actually less efficient than simply accepting the fee-payer’s PAYE deductions directly.

The comparison matters because many contractors assume an umbrella company offers some meaningful tax advantage over a standard inside-IR35 engagement. For most contractors at £500 per day, that assumption does not hold. What matters more is the fee structure of the umbrella company, the holiday pay treatment, and whether the contractor can negotiate a rate that accounts for employer NIC being deducted from their contract fee.

The Fundamental Problem: Employer NIC Eats the Contract Rate

When a contractor is inside IR35, the income is treated as employment income. This means both employee and employer National Insurance contributions apply to the deemed salary. The employer NIC , at 15% from April 2025 , is typically funded from within the contract rate rather than paid on top of it.

This is the central financial reality of inside IR35 work that no comparison calculator makes sufficiently clear. At £500 per day, assuming 220 working days per year, the gross contract income is £110,000. But that £110,000 is not the starting point for calculating the contractor’s net income , it is the budget from which employer NIC, the umbrella’s margin, holiday pay provisions, and the apprenticeship levy are all deducted before the deemed salary is established.

The comparable outside IR35 position starts with £110,000 reaching the contractor’s company in full, from which corporation tax is paid and a mix of salary and dividends extracted.

The inside IR35 position starts with £110,000 being subjected to costs before the contractor sees any of it.

The Calculation at £500/Day

Assumptions:

- 220 days worked per year (allowing for holidays, sick, and bank holidays)

- Contract rate: £500/day

- Gross contract income: £110,000

- Umbrella margin: £25 per week (approximately £1,300 per year , a competitive mid-market rate)

- Holiday pay: accrued within the contract rate (not paid as additional)

- 2026/27 tax rates and NIC thresholds

Step 1: Gross Contract Value and Deductions Before Deemed Salary

From the £110,000 gross:

Deduction | Amount |

Employer NIC at 15% (on amount above secondary threshold £9,100) | approximately £14,685 |

Apprenticeship levy (0.5% of payroll above £3m , not applicable for individual umbrella employees) | £0 |

Umbrella margin | £1,300 |

Holiday pay provision (accrued 12.07% of basic , where included in rate) | £0 (treated as part of gross) |

Deemed salary available | approximately £94,015 |

The employer NIC calculation is on the deemed salary itself , this creates a circularity that the umbrella resolves by working backwards. The precise employer NIC on £94,015 above the £9,100 secondary threshold is approximately £12,737. But the employer NIC is funded from the contract rate, so the effective total available for salary and employer NIC combined is £110,000 minus the umbrella margin. Working through the algebra:

Total available: £108,700 (after £1,300 umbrella margin) This is divided between employer NIC and deemed salary. Employer NIC = 15% × (deemed salary − £9,100) Deemed salary ≈ £108,700 ÷ 1.15 + £9,100 × (0.15/1.15) ≈ £95,583 (approximation)

For the purposes of this comparison, the deemed salary is approximately £95,000 after accounting for employer NIC and the umbrella margin.

Step 2: Employee Deductions on the Deemed Salary

From the deemed salary of £95,000:

Deduction | Amount |

Personal allowance | £12,570 |

Taxable income | £82,430 |

Income tax (basic rate band £12,570 to £50,270 = £37,700 at 20%) | £7,540 |

Income tax (higher rate band £50,270 to £95,000 = £44,730 at 40%) | £17,892 |

Total income tax | £25,432 |

Employee NIC (£12,570 to £50,270 = £37,700 at 8%) | £3,016 |

Employee NIC (£50,270 to £95,000 = £44,730 at 2%) | £895 |

Total employee NIC | £3,911 |

Approximate net take-home (umbrella): £95,000 − £25,432 − £3,911 = approximately £65,657 per year

This equates to approximately £5,471 per month or £298 per day net.

Step 3: Direct Fee-Payer PAYE (Inside IR35, No Umbrella)

Where the fee-payer operates PAYE directly on an inside IR35 engagement, there is no umbrella margin. The calculation is otherwise the same , employer NIC is deducted from the contract rate before the deemed salary is established. The absence of a £1,300 umbrella margin means the deemed salary is approximately £1,300 higher , around £96,300.

The additional income falls in the higher rate band at 40% (income tax) plus 2% (employee NIC), reducing the net benefit of the additional salary to approximately £754. Direct fee-payer PAYE therefore produces approximately £754 more take-home per year than the umbrella comparison above.

For a contractor working a full year, this is around £14 per week , not transformative, but meaningful over several years of inside IR35 working.

The Holiday Pay Variable: Where Many Contractors Lose Money

The holiday pay treatment is the most commonly misunderstood element of umbrella calculations. Two umbrella companies might quote the same apparent take-home figure, but if one accrues holiday pay within the contract rate and the other pays an uplifted rate that includes holiday pay as additional income, the cash position differs substantially.

Umbrella companies are required to accrue and pay statutory holiday pay to their employees. The minimum is 5.6 weeks per year. Where the contract rate is used as the basis for calculating holiday pay, the holiday pay is funded from within that rate , the contractor is effectively receiving a lower daily fee for the working days they bill, with the surplus funding their holiday pay accrual.

A contractor who bills 220 days and accrues holiday pay within a £500 rate is funding approximately 28 days of holiday pay from those 220 days of billing. The effective working daily rate being retained is lower than £500.

Some umbrellas operate a holiday pay rollup , paying the holiday pay as an enhanced rate on each pay period rather than separately accruing it. Where rolled-up holiday pay is included in the stated daily rate, the contractor should be aware that they are already receiving their holiday entitlement as part of their regular pay and will not receive additional holiday pay when they actually take leave.

HMRC’s view on rolled-up holiday pay has been that it is unlawful in principle under the Working Time Regulations , the Pay Act 2023 and subsequent guidance provided some clarification, but the position remains one where contractors should check carefully how their umbrella is treating holiday pay and ensure they understand whether the stated contract rate is truly £500/day or whether it already includes a holiday pay element.

The Outside IR35 Comparison: What Contractors Are Giving Up

A contractor outside IR35, operating through their own limited company, with the same £500/day contract rate:

Gross: £110,000 Corporation tax (19% on profits up to £50,000 after salary): varies Salary of £12,570: no income tax, minimal NIC Dividends: taxed at 10.75% (basic) and 35.75% (higher) from April 2026

A typical outside IR35 contractor extracting a salary of £12,570 and dividends of approximately £77,000 would pay:

- Corporation tax: approximately £18,905 (at a blended rate)

- Dividend tax: approximately £24,000

- Income tax on salary: nil

- NIC (employer): minimal if Employment Allowance is unavailable for a single-director company

Approximate net outside IR35: approximately £67,000 to £70,000 per year , materially higher than the inside IR35 umbrella take-home of approximately £65,657.

The gap between inside and outside at this rate is approximately £2,000 to £4,000 per year , narrower than many contractors assume, because the contractor’s limited company also incurs costs (accountancy fees, company maintenance) that erode some of the apparent advantage.

Inside IR35 vs Umbrella at £500/Day

A comprehensive take-home comparison for UK contractors. Discover where your £110,000 gross contract value actually goes, the impact of employer NICs, and how it compares to Outside IR35.

Where does the money go?

The fundamental problem with Inside IR35 work is that Employer NIC (15%) eats the contract rate. At £500/day (220 days), your £110,000 gross is not your starting salary. It is the budget from which employer taxes, umbrella margins, and levies are deducted before your deemed salary is established.

Includes a typical £25/week umbrella margin.

Visual Breakdown (£110,000 Gross)

Annual Calculation (220 Days)

Inside vs Outside IR35: What are you giving up?

Many contractors assume outside IR35 pays vastly more. While it is more efficient, the gap at £500/day is narrower than expected because your limited company also incurs costs (accountancy, software, insurance) that erode the advantage.

£65,657 / yr

~60% Retention Rate

- Employer NICs deducted from contract rate

- Umbrella margins apply

- No travel or subsistence expense claims

- No company administration or accountancy fees

£67k - £70k / yr

~63% Retention Rate

- Corporation Tax (19%-25%) paid on profits

- Tax-efficient Salary (£12,570) + Dividends split

- Business expenses reduce taxable profit

- Must pay accountancy and running costs out of pocket

Variables That Affect Your Take-Home

This is the most commonly misunderstood element. Umbrellas must pay statutory holiday pay (5.6 weeks/yr minimum).

Accrued vs Rolled-Up:

- Accrued (Within Rate): If you bill 220 days, you are funding ~28 days of holiday pay from those 220 days. Your effective daily working rate is lower than £500. The surplus is saved and paid when you take time off.

- Rolled-Up: Paid as an enhanced rate on each pay period. If this is included in your stated £500 rate, you will not get paid when you actually take leave. Check your contract!

Scottish contractors pay Scottish income tax on their deemed salary. The Scottish Higher rate is 42% (vs 40% in rest of UK), and it applies at a lower threshold (£43,662).

Impact: On a £95,000 deemed salary, a Scottish contractor pays approximately £1,000 MORE in annual income tax than an English counterpart on the exact same £500/day contract. This should be factored into your rate negotiations.

If you work part of the year Outside IR35 (Ltd Co) and part Inside IR35 (Umbrella), both incomes flow into the same Self Assessment return.

The Danger: If your Ltd Co salary/dividends already push you into the Higher Rate band (£50,270+), every single pound of your Umbrella deemed salary will be taxed at 40% (or 42% in Scotland) plus 2% Employee NIC. Carefully time your dividend draws in mixed years to manage your marginal tax bands.

Warning: Disguised Remuneration

Contractors who use umbrella companies promising to deliver 80% to 85%+ of contract income as take-home should be extremely wary. At £500/day, legitimate take-home is roughly 60%.

HMRC aggressively pursues users of schemes that route pay through loans, annuities, or advances to avoid tax. You will be liable for the missing tax, plus heavy interest and penalties (e.g., The Loan Charge).

Questions to Ask Any Umbrella Company

-

1How is Employer NIC funded? It should come from within the contract rate. If they suggest it is "avoided", walk away immediately.

-

2What is your weekly margin? It should be transparent. Typically £15 to £30 per week for a compliant umbrella.

-

3How is Holiday Pay treated? Is it accrued within the rate or rolled-up? What happens to accrued pay if the contract ends?

-

4Can you provide a line-by-line worked example? A legitimate company will show exactly how Gross -> Net is calculated without hesitation.

-

5Are you FCSA or Professional Passport accredited? HMRC doesn't formally approve umbrellas, but membership in these bodies indicates baseline compliance.

Scottish Contractors: The Tax Rate Difference

Scottish contractors inside IR35 pay Scottish income tax on their deemed salary, not the rest-of-UK rates used in the calculation above. The Scottish Higher rate is 42% rather than 40%, applying to income above £43,662.

For a Scottish contractor with a deemed salary of approximately £95,000:

Income from £43,662 to £95,000 = £51,338 taxed at 42% instead of 40%. Additional income tax compared to rest of UK: £51,338 × 2% = approximately £1,027 more per year.

The Scottish contractor’s net take-home is therefore approximately £1,000 lower than the same contract worked in England, all else being equal.

This is not a large difference in percentage terms but should be factored into contract rate negotiation. A Scottish contractor who is working on a UK-wide project alongside English counterparts is receiving a lower net income from the same contract rate simply by virtue of their residence , one of the more tangible real-world consequences of the Scottish tax divergence.

Mixed-Status Years: Part Inside, Part Outside

Many contractors face a mixed year , perhaps the first half of the year on an outside IR35 contract through their limited company, and the second half on an inside IR35 engagement (through an umbrella or direct PAYE) after a new project comes with an inside determination.

The challenge in a mixed year is the stacking of income from both routes. The limited company income and umbrella income both flow into the same Self Assessment return, and the combined income determines the marginal tax rate on each element.

Where the outside IR35 portion has already taken the contractor into the higher rate band , because a full-year outside contract would generate significant salary and dividends , any inside IR35 income in the same year falls partially or fully at the 40% rate. If the contractor’s limited company salary was £12,570 and dividends of £40,000 were drawn in the first half, total income before the umbrella income is £52,570 , into the higher rate band. Every pound of umbrella income then falls at 40% income tax (or 42% for Scottish taxpayers) plus 2% employee NIC.

This stacking effect makes mixed-status years particularly expensive and requires careful timing. Where the contractor has flexibility about when to draw dividends from the limited company portion, reducing the dividend draw in a mixed year to manage the effective marginal rate on the umbrella income is worthwhile.

Disguised Remuneration: The Risk With Non-Compliant Umbrellas

The attraction of unusually high take-home claims from some umbrella companies should be treated with significant caution. HMRC warns that some umbrella companies use contrived structures to inflate apparent take-home pay , routing pay through loans, annuities, or other non-salary mechanisms that the umbrella claims are tax-free. These are disguised remuneration schemes. HMRC does not recognise these as legitimate and will pursue both the contractor and the promoter for the tax owed, plus interest and penalties.

Contractors who use umbrella companies that promise to deliver 85% or more of contract income as take-home should be extremely wary. At £500/day, legitimate take-home is approximately 60% of contract income after all deductions. Any claim significantly above that figure likely involves a scheme HMRC will challenge.

The Loan Charge , which has been a major source of controversy since it was introduced , demonstrated that HMRC will pursue historical use of disguised remuneration schemes aggressively, sometimes many years after the payments were made. Contractors who have used such schemes should take specialist advice; those considering umbrella companies should verify that the take-home figure being quoted is consistent with legitimate PAYE processing.

A compliant umbrella’s take-home figure should be explainable from first principles: contract income minus employer NIC minus umbrella margin minus income tax minus employee NIC equals net pay. If a company cannot or will not show this calculation clearly, that is a serious warning sign.

Questions to Ask Any Umbrella Company

Before engaging with any umbrella company, the following questions should have clear, direct answers:

How is employer NIC funded? It should come from within the contract rate , if the umbrella suggests it is somehow avoided, something is wrong.

What is your weekly margin and what does it cover? Margin should be transparent , typically £15 to £30 per week for a compliant umbrella.

How is holiday pay treated? Is it accrued within the rate or paid as separate additional income? What happens to accrued holiday pay at the end of the contract?

Are you on HMRC’s approved umbrella list? HMRC does not formally approve umbrella companies, but the FCSA (Freelancer and Contractor Services Association) and Professional Passport maintain compliance standards. Membership of these bodies indicates a baseline level of compliance commitment.

Can you provide a worked example showing exactly how my contract rate becomes my net pay? A legitimate umbrella can do this without hesitation. If the calculation is obfuscated or relies on non-PAYE mechanisms, walk away.

Inside IR35 vs Umbrella: Take-Home at £500/Day

An interactive breakdown of what a contractor on an inside-IR35 determination actually keeps — through an umbrella, through the fee-payer's PAYE, or outside IR35 — using verified 2026/27 tax rates and the post-Autumn-Budget-2025 dividend changes.

The difference is smaller than most contractors expect

Many contractors assume an umbrella company offers a meaningful tax advantage over a standard inside-IR35 engagement. At £500 a day, that assumption does not hold. What actually moves the needle is the umbrella's margin, how holiday pay is treated, and whether you can negotiate a rate that accounts for employer NIC being taken out of your fee.

The core problem: employer NIC eats the contract rate

When you are inside IR35, your income is treated as employment income, so both employee and employer National Insurance apply to the deemed salary. Crucially, employer NIC — 15% from April 2025 — is funded from within your contract rate, not paid on top of it.

From April 2025 the secondary (employer NIC) threshold also fell from £9,100 to just £5,000, so more of your fee is exposed to that 15% charge than under the old rules. Your £110,000 of gross fee income is therefore not the starting point for your take-home — it is the budget from which employer NIC, the umbrella margin and holiday pay are all deducted before a deemed salary is even established.

Outside IR35 starts here

£110,000 reaches your limited company in full. You pay corporation tax, then extract a salary-plus-dividends mix.

Inside IR35 starts here

£110,000 is hit by employer NIC, the umbrella margin and holiday pay provisions before you see a penny of deemed salary.

At £500/day on a compliant umbrella, legitimate take-home lands at roughly 60% of contract income. Any company promising 80–90% is almost certainly using a non-compliant scheme. Open the Calculator tab to model your own rate.

Live take-home calculator

Adjust the inputs to compare all three routes side by side. Figures use 2026/27 thresholds, 15% employer NIC, an £5,000 secondary threshold, and the new April-2026 dividend rates for the outside-IR35 route.

- Deemed salary £95,174

- Employer NIC £13,526

- Margin £1,300

- Income tax £25,502

- Employee NIC £3,914

- Deemed salary £96,304

- Employer NIC £13,696

- Margin £0

- Income tax £25,954

- Employee NIC £3,937

- Corporation tax £21,768

- Dividends drawn £74,526

- Dividend tax £17,164

- Salary £12,570

- Co. running costs £0

How the umbrella route splits the contract value

Net take-home compared

The outside-IR35 figure ignores accountancy fees, insurance and admin. Adding ~£1,800 of real running costs typically narrows the gap to inside IR35 to around £3,000–£3,500 a year, not the dramatic difference many contractors imagine.

Holiday pay: where contractors quietly lose money

This is the most misunderstood line in any umbrella quote. Two umbrellas can show the same headline take-home, yet leave you with very different cash positions depending on how holiday pay is handled.

Accrued within the rate

Statutory holiday is 5.6 weeks (about 28 days). If it is accrued from within your £500 rate, you are effectively billing at a lower daily figure and funding ~28 days of holiday from the 220 you work. Your true working rate is below £500.

Rolled-up holiday pay

Some umbrellas add holiday pay to each payslip ("rolled up"). If that is inside the stated rate, you are already receiving it as you go — and will get nothing extra when you actually take leave.

The Employment Rights legislation and subsequent guidance clarified rolled-up holiday pay, but the position still rewards checking carefully. Always confirm: is the quoted £500/day a true rate, or does it already bake in a holiday-pay element? And what happens to accrued holiday pay if the contract ends before you take it?

Scottish contractors pay materially more

Scottish income tax has six bands. On an inside-IR35 deemed salary near £95,000, the gap to the rest of the UK is bigger than commonly quoted — because the 45% Advanced rate bites above £75,000, on top of the 42% Higher rate.

2026/27 Scottish bands (non-savings income)

At a ~£95,000 deemed salary, a Scottish contractor pays roughly £3,000 more income tax a year than an identical contract worked in England — driven by the 42% Higher rate and the 45% Advanced rate. This is far more than the often-quoted "~£1,000" figure, which overlooks the Advanced band. Switch the Calculator to "Scotland" to see your own gap.

A Scottish contractor on a UK-wide project takes home less than English counterparts on the very same rate — one of the more tangible consequences of Scottish tax divergence, and a real factor for rate negotiation.

Mixed-status years stack income — and cost

A common pattern: the first half of the year outside IR35 through your limited company, the second half inside IR35 after a new project lands with an inside determination. The problem is stacking.

The stacking effect

Limited-company income and umbrella income both flow into the same Self Assessment return, and the combined total sets the marginal rate on each part. Suppose the first half draws a £12,570 salary plus £40,000 of dividends — that is £52,570, already into the higher-rate band.

Every pound of umbrella income then lands at 40% income tax (42% in Scotland) plus 2% employee NIC from the very first payslip, with no fresh basic-rate band to soften it.

Where you have flexibility on when to draw dividends, reducing the dividend draw in a mixed year can lower the effective marginal rate on the umbrella income. Timing, not the route itself, is what makes mixed years expensive.

Disguised remuneration: the 85%+ trap

Treat unusually high take-home claims with serious caution. HMRC warns that some umbrellas use contrived structures — loans, annuities or other "non-salary" mechanisms — to inflate apparent pay. These are disguised remuneration schemes.

Why "85% take-home" cannot be real here

At £500/day, legitimate take-home after all deductions is around 60% of contract income. HMRC does not recognise loan-style schemes; it pursues both the contractor and the promoter for the tax owed, plus interest and penalties. The Loan Charge showed HMRC will chase historical use of these schemes many years later.

A compliant umbrella's figure should be explainable from first principles: contract income − employer NIC − margin − income tax − employee NIC = net pay. If a provider will not show that clearly, walk away.

What a legitimate breakdown looks like (£500/day)

Questions to ask any umbrella company

Tap each question once you have a clear, direct answer. A compliant provider answers all of these without hesitation.

Key takeaways

- At £500/day, a compliant umbrella yields roughly £65,000–£66,000 net a year. Direct fee-payer PAYE adds only about £650 by removing the margin.

- Outside IR35 at the same rate is roughly £68,000–£70,000 before company costs — a gap of about £3,000–£4,000, not the dramatic difference many expect, especially after April 2026 dividend rises.

- Employer NIC at 15% is funded from within the contract rate, with the secondary threshold now just £5,000. This is the single biggest driver of inside-IR35 take-home.

- Scottish contractors pay roughly £3,000 more income tax at this level, due to the 42% Higher and 45% Advanced rates.

- Schemes promising 85%+ take-home are almost certainly non-compliant. Legitimate take-home is around 60% of contract income.

- Holiday pay treatment is the most misunderstood variable — it changes the effective daily rate you actually receive.

- Before choosing an umbrella, demand a line-by-line breakdown of how your rate becomes net pay.

2026/27 figures used in this tool

Looking ahead: income tax thresholds are now frozen to April 2031, so fiscal drag pulls more of every rate rise into higher bands. Dividend ordinary and upper rates rose 2 points from April 2026, narrowing the outside-IR35 advantage further. Inside-IR35 modelling matters more each year, not less.

Key Takeaways

- At £500 per day on an inside IR35 contract, a compliant umbrella company produces approximately £65,000 to £66,000 of net annual take-home after all deductions. Direct fee-payer PAYE produces approximately £750 more per year by eliminating the umbrella margin.

- The equivalent outside IR35 take-home at the same contract rate is approximately £67,000 to £70,000 , a difference of roughly £2,000 to £4,000 per year, not the dramatic gap that many contractors expect.

- Employer NIC at 15% is funded from within the contract rate, not paid on top of it. This reduces the starting point for income tax and employee NIC calculations. Understanding this is essential for accurate take-home modelling.

- Scottish contractors face approximately £1,000 more in annual income tax at the same contract rate due to Scottish Higher rate tax at 42% versus the rest-of-UK 40%.

- Umbrella schemes promising 85% or more take-home at this contract rate are almost certainly non-compliant. Legitimate take-home is approximately 60% of contract income. HMRC actively pursues promoters and users of disguised remuneration schemes.

- Holiday pay treatment is the most commonly misunderstood variable in umbrella take-home comparisons. The way holiday pay is accrued or paid affects the effective daily rate the contractor actually receives.

- Before choosing an umbrella company, request a line-by-line breakdown of how the contract rate becomes net pay. Any legitimate company should provide this without hesitation.

FAQs

Q1: How does working through an umbrella company inside IR35 compare to agency PAYE in terms of take-home pay at a £500 daily rate?

In my experience advising contractors, the difference often boils down to the umbrella’s margin and how they handle statutory costs. With agency PAYE, you might see a lower effective day rate because the agency absorbs some employer costs, but umbrellas frequently quote an uplifted assignment rate to compensate. For someone on £500 a day over 220 days, expect the umbrella route to net you a few hundred pounds more annually after their typical £20-£30 weekly fee, provided you compare illustrations carefully. Always request breakdowns showing employer NI and apprenticeship levy deductions upfront.

Q2: Can a contractor in Scotland expect different take-home figures compared to someone in England on the same £500/day umbrella contract?

Well, it’s worth noting the Scottish income tax bands do bite harder in the higher brackets. A contractor north of the border on this rate could lose an extra 2-3% in tax compared to England and Wales once earnings push into the advanced rate. I’ve seen this catch out clients relocating for family reasons—run your numbers with a Scottish tax code in the umbrella’s calculator to avoid surprises at year-end.

Q3: What happens to take-home pay if you have a second job or pension income alongside an umbrella contract at £500/day?

This is a common mix-up. Your umbrella will usually issue a BR (basic rate) tax code for the contract if they know about other income, meaning no personal allowance on that pay. In practice, this can reduce your net by £100-£200 per week until you update HMRC. One Leeds-based IT contractor I advised had this happen and reclaimed over £2,000 via Self Assessment by sorting the code early.

Q4: How do holiday pay and sick pay entitlements affect the effective take-home when comparing umbrella to inside IR35 limited company setups?

In my 15 years working with business owners, many overlook that umbrella employees accrue statutory holiday and sick pay, which can add real value equivalent to 1-2 extra weeks’ pay annually if utilised. Unlike a limited company inside IR35 where you’d need to manage this yourself (often with less protection), the umbrella builds it in—though it’s funded from your rate. Factor this into your comparison rather than just the weekly payslip.

Q5: Is salary sacrifice into a pension a worthwhile way to boost net pay on a £500/day umbrella contract?

Absolutely, and it’s one of the smarter moves for higher earners. By sacrificing part of your gross pay into a pension, you can reduce both income tax and NI, and some umbrellas pass on employer NI savings too. I’ve had clients in Manchester increase their effective take-home equivalent by 5-8% this way while building retirement pots. Check if your umbrella offers this, not all do it optimally.

Q6: What should someone with irregular contract lengths (e.g., 3-6 months) consider when choosing umbrella over trying to operate inside IR35 via limited?

For shorter gigs, the admin simplicity of an umbrella often outweighs the marginal tax differences. Setting up and winding down company filings for brief periods eats into time and fees. A client of mine in Birmingham switched mid-year and saved hours that were better spent winning the next contract.

Q7: How do travel and subsistence expenses work differently under umbrella versus limited company inside IR35?

Under umbrella, post-2016 rules strictly limit what you can claim for home-to-site travel, often treating you as having a permanent workplace. Limited companies sometimes have more flexibility if genuinely outside, but inside it’s similar. Always keep detailed records; one freelancer I advised recovered several thousand by properly logging site-based expenses through their umbrella.

Q8: Can you switch from umbrella to limited company mid-contract if the IR35 status changes to outside?

It’s possible but requires careful negotiation with the agency and client. In practice, I’ve seen contractors do this successfully after a determination review, boosting take-home significantly. Get everything in writing and consult an accountant early to avoid gaps in compliance or pay.

Q9: What are the risks of choosing a cheap umbrella company for a £500/day contract?

It’s a false economy. Low-margin providers sometimes cut corners on compliance, leading to HMRC disputes years later. Stick to FCSA-accredited ones—I’ve helped clients untangle messes from dodgy setups that promised higher nets but delivered penalties instead.

Q10: How does student loan repayment impact take-home pay calculations for umbrella workers at this rate?

Plan 2 or postgraduate loans can take a noticeable chunk (around 9% or 6% above thresholds). At £500/day, you’re likely well into repayment territory, so your net could drop by £200-£300 monthly. Factor this when comparing to limited company structures where dividend planning might ease the burden slightly.

Disclaimer

The information provided in this article is for general guidance only and is not intended to constitute professional advice, tax advice, financial advice, legal advice, or any other form of regulated guidance. Although every effort has been made to ensure accuracy at the time of publication, Fair View Accounting Services, including its director, employees, contractors, writers, and content-creation team, accepts no responsibility for any loss, damage, penalty, or consequence arising from reliance on the information contained herein.

UK tax legislation changes frequently, and HMRC interpretations, thresholds, and rules may vary depending on the individual circumstances of each taxpayer. Nothing in this article should be considered a substitute for obtaining formal, personalised advice from a qualified accountant or tax professional. Readers should not take action—or refrain from taking action—based solely on the content published on this website.

Fair View Accounting Services does not guarantee the completeness, accuracy, or ongoing validity of the information provided and assumes no liability for omissions or errors, whether typographical, factual, or technical. By using this content, the reader acknowledges that all responsibility for decisions remains solely with the user.