Corporation Tax Reliefs: Claiming Losses and Carry-Forwards With Step-By-Step Examples

Corporation Tax Reliefs: Claiming Losses and Carry-Forwards with Step-by-Step Examples in the UK

None of us enjoys tax surprises, especially when a tough trading year leaves your company staring at a loss while you’re still paying Corporation Tax on earlier profits. Yet for UK business owners filing in 2026, getting loss relief right can turn that red ink into real cash in the bank, or a lighter bill down the line. I’ve spent the last 18 years sitting across the desk from directors just like you, helping them navigate these rules without the headaches.

Why Loss Relief Matters More Than Ever for UK Businesses in 2026

The Corporation Tax landscape remains reassuringly stable this year. The main rate stays at 25% and the small profits rate at 19% for profits up to £50,000, with marginal relief kicking in up to £250,000. No dramatic shifts hit the loss relief rules themselves in the latest Budget, which is good news, the framework we’ve lived with since 2017 is still the one we work with.

What has changed for many of my clients is the interaction with capital allowances. From January 2026 we have that new 40% first-year allowance for main-rate plant and machinery, while the writing-down allowance drops to 14% from April. Timing investment correctly can deliberately create or enlarge a trading loss, something we’ll come back to.

The Four Main Ways to Get Relief, and the Order That Counts

HMRC gives you options, but you must choose the right one at the right time. You can:

- Set the loss against other profits in the same accounting period

- Carry it back to an earlier period

- Surrender it via group relief (if you’re in a group)

- Carry it forward to future profits

The golden rule I drum into every client: never assume the default carry-forward is best. A carry-back claim can trigger an immediate repayment; a forward claim only helps next year’s profits.

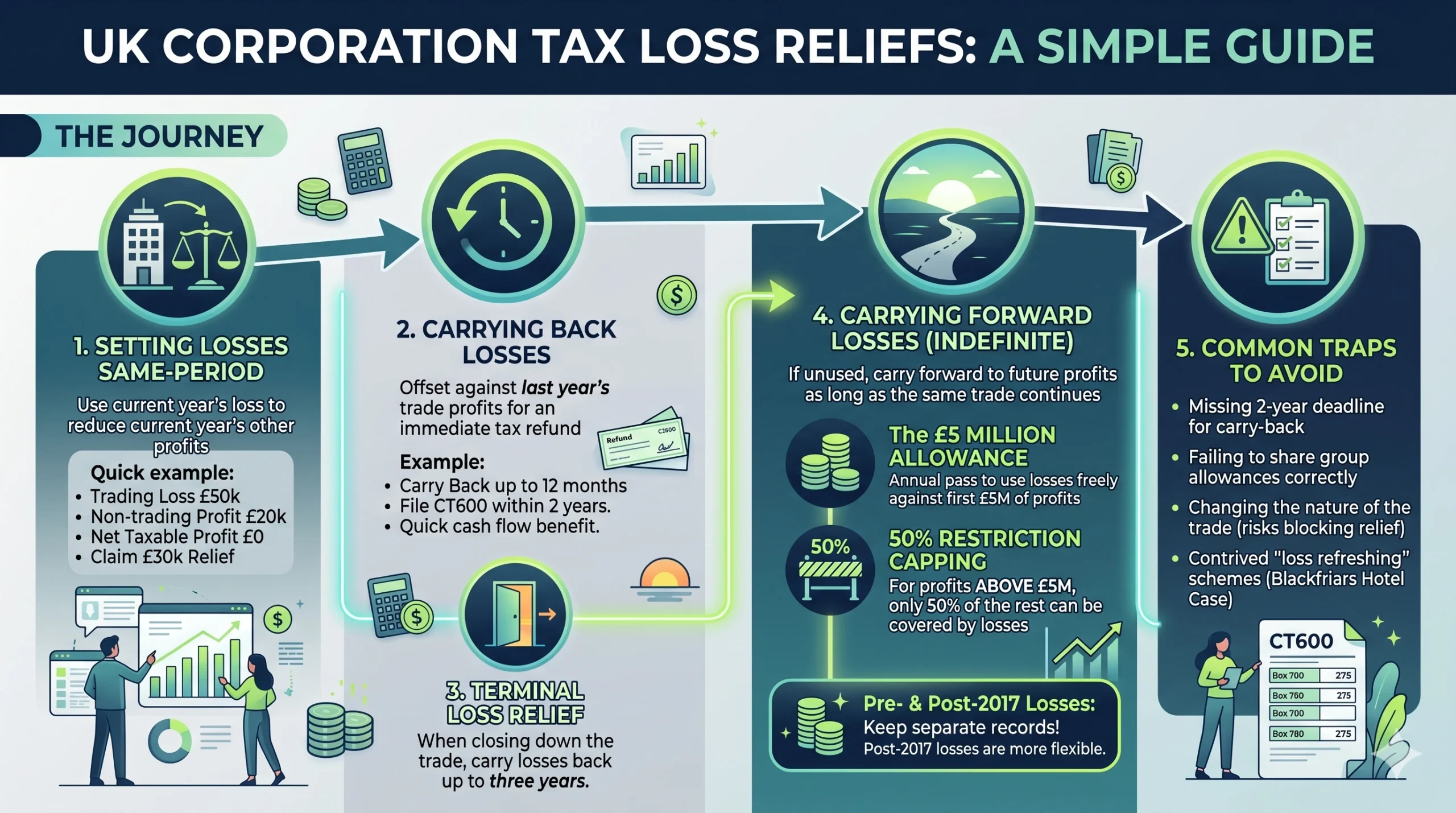

How Same-Period Relief Works in Practice

Start here, it’s the simplest and most automatic. Your trading loss (after capital allowances and before charges) simply reduces your total taxable profits for that same accounting period.

Picture a manufacturing company, Widgets Ltd, with £120,000 trading profit and £45,000 non-trading loan interest in the year ended 31 March 2026. It also makes a £80,000 trading loss in the same period. The loss wipes out the trading profit and £35,000 of the interest, leaving just £10,000 taxable. No carry-forward or back needed.

Simple? Yes. But I’ve seen clients forget to add back capital allowances correctly and end up with a smaller loss than they could have claimed. Always double-check the computation before you file.

Carrying Losses Back, The Refund Route Most Businesses Miss

If same-period relief doesn’t use the whole loss, you can carry it back one full year (12 months) against any profits of the same trade. The claim must be made within two years of the end of the loss-making accounting period.

Here’s a real-life style example I walked through with a client last month:

Year ended 31 March 2025

Trading profit: £150,000

Corporation Tax paid: £37,500 (at 25%)

Year ended 31 March 2026

Trading loss: £80,000 (after full capital allowances)

Step-by-step claim:

- Decide how much of the £80,000 loss to carry back (you don’t have to use all of it).

- Reduce the 2025 profit to £70,000.

- Corporation Tax now due for 2025: £17,500.

- Repayment due: £20,000 (plus interest from HMRC).

- On the CT600 for the 2026 period, tick the “claim affecting an earlier period” box and enter the carried-back amount in the correct losses box.

The client received the cheque within six weeks. None of us enjoys waiting for money, but this really does speed things up.

Terminal Loss Relief, When Closing the Doors Can Still Save Tax

If you’re closing the trade completely, the rules get even more generous. You can carry the loss back up to three years, starting with the latest year first. I’ve used this for several clients winding up family businesses, it’s often the last tax-saving opportunity before the shutters come down.

Claim process is the same as normal carry-back, but you must clearly state it’s a terminal loss claim and provide evidence the trade has ceased.

Claiming on the CT600, The Boxes That Matter

Every claim lives inside your Company Tax Return. For the year the loss arises:

- Box 155: usually 0 if you’re claiming relief now

- Box 780: enter the full loss

- Box 275: the amount actually used this period or carried back

If you’re carrying back to an earlier return, you may need to amend that return or send a separate letter. Get the wording right, HMRC are surprisingly strict on the exact details required.

A Quick Checklist Before You Hit “Submit”

- Have you kept separate records for pre- and post-1 April 2017 losses?

- Does the trade continue (or has it genuinely ceased)?

- Have you considered group relief first if you’re in a group?

- Is the claim within the two-year window?

- Have you double-checked capital allowances to maximise the loss?

Tick these and you’re already ahead of 70% of the returns I review.

In the next part of this guide we’ll move on to carrying losses forward, the rules that catch out even experienced directors when profits finally return, and the £5 million plus 50% restriction that bites harder than most people realise. We’ll run through a larger-company example with real numbers and show exactly how the deductions allowance works in practice.

I’ll also share the exact anti-avoidance trap that tripped up a company in the Blackfriars Hotel case at the First-tier Tribunal, so you never make the same mistake. See you there, and in the meantime, if you’re sitting on a loss right now, drop your CT600 figures into the boxes above and you could be looking at a repayment before the summer.

Corporation Tax Reliefs

Claiming losses & carry-forwards made interactive. Understand rules, calculate refunds, avoid limits, and minimize CT.

Quick Tax Pathway Finder

Answer a few quick operational questions to find the most tax-efficient and compliant method to utilize your company's trading losses.

Same-Period & Carry-Forward Relief

Since your trade is active and has no group options or prior-year profits to offset against, any unused loss should be carried forward to offset future trading profits. Ensure your active trade does not undergo major changes to keep this relief secure.

Scenario Input (Widgets Ltd Style Model)

Enter current losses and prior periods to calculate instantaneous same-period offsets and cash refund entitlements.

Refund & Relief Outcomes

Repayment Tip: On your current year's CT600 return, check the "claim affecting an earlier period" tick box to activate fast processing. Refunds are usually cleared in 6-8 weeks from submission.

Large Loss Carry-Forward & Deductions Restriction Tool

Simulate how the UK’s £5,000,000 Deductions Allowance and 50% restriction rule limits relief for profits post-2017.

First £5m (standard rate) can be offset with zero restriction. Group limits apply.

Tax Calculation Results

Interactive CT600 Form Locator

Click on the relevant boxes below to see exactly which numbers from your computation should be populated in each box on your HMRC CT600 return.

Restricted Profits Offset

Enter the amount of brought forward losses that are being used to offset taxable profits of this period that falls under the restricted calculation (such as amounts after the £5m Allowance limit).

The Blackfriars Hotel Case

Blackfriars Hotel (UK) Holdings Ltd v HMRC [2024] UKFTT 1095 (TC)

In this crucial recent FTT case, the taxpayer attempted to artificially "refresh" old losses by establishing new loan arrangements that generated non-trading profits. The tribunal interpreted the Targeted Anti-Avoidance Rule (TAAR) purposively.

HMRC strictly denies loss offsets if your tax arrangement exists primarily to utilize legacy losses outside normal trade channels. Ensure any restructuring is purely for genuine commercial reasons.

Pre- vs. Post-1 April 2017 Loss Rules

Pre-Filing Audit Checklist

Review these critical areas before finalizing your corporate computations.

Carrying Losses Forward, The Rules That Catch Out Even Seasoned Directors

Be careful here, carrying losses forward sounds straightforward, but since the 2017 reforms, it’s become one of the most misunderstood parts of the Corporation Tax system. I’ve lost count of the number of clients who’ve come to me assuming they can wipe out every future profit with old losses, only to discover the £5 million deductions allowance and the 50% cap waiting for them.

The basic principle remains: if your trading loss can’t be used in the current period or carried back, it carries forward indefinitely, provided the trade continues. No time limit, which is a relief compared to some other jurisdictions.

But from accounting periods starting on or after 1 April 2017, HMRC introduced restrictions on how much carried-forward loss you can actually use in any one year.

The £5 Million Deductions Allowance, Your Free Hit Every Year

Every company (or group, more on that shortly) gets a £5 million deductions allowance each year. This is the amount of carried-forward losses you can set against profits without restriction. It’s like a free pass for the first £5 million of taxable profit.

Above that, you can only use carried-forward losses to offset 50% of the remaining profits.

Let’s run through a concrete example that mirrors a mid-sized engineering firm I advised last year.

TechForge Ltd, Year ended 31 December 2025

- Brought-forward trading losses (post-1 April 2017): £12 million

- Current year taxable profits (before any loss relief): £18 million

Step-by-step calculation:

- Deductions allowance: £5 million (full amount available as a single company).

- Profits covered fully by allowance: £5 million, tax at 25% = £1.25 million saved.

- Remaining profits: £18m, £5m = £13 million.

- 50% restriction applies: you can use losses to offset only 50% of £13m = £6.5 million.

- Total losses used this year: £5m + £6.5m = £11.5 million.

- Taxable profit after relief: £18m, £11.5m = £6.5 million.

- Corporation Tax due: £6.5m × 25% = £1.625 million.

Without the restriction, the company could have used all £12 million of losses and paid tax on just £6 million. Instead, £500,000 of losses remain carried forward. That’s a real cash-flow hit, roughly £125,000 extra tax paid that year.

Pre- and Post-1 April 2017 Losses, Why the Split Still Matters

Losses arising before 1 April 2017 can generally only be set against profits of the same trade (not total profits), unless used under the streamed rules.

Post-2017 losses are more flexible, they can go against total profits.

But both types are caught by the £5m + 50% restriction when carried forward into periods starting after 1 April 2017.

I always advise clients to keep these pots separate in their records. Mixing them up is one of the most common errors I see when reviewing draft computations.

Group Companies and the Shared £5 Million Allowance

If you’re in a group, the £5 million deductions allowance is shared across the group. You must nominate one company to allocate it via a group allowance allocation statement (submitted with the CT600 of the nominating company).

Get this wrong and HMRC can deny part of the relief. I’ve seen groups lose out because the statement was late or incomplete, don’t let that be you.

The Blackfriars Hotel Case, Don’t Try Loss-Refreshing Tricks

In Blackfriars Hotel (UK) Holdings Ltd v HMRC [2024] UKFTT 1095 (TC), the First-tier Tribunal looked at anti-avoidance rules designed to stop contrived arrangements that “refresh” carried-forward losses.

The company had substantial non-trading loan relationship deficits carried forward. They entered arrangements involving new loans that generated profits, hoping to use the old losses against those new profits.

HMRC invoked the targeted anti-avoidance rule (TAAR) under CTA 2010 s 730G, arguing the profits were “relevant profits” from a “tax arrangement”. The Tribunal agreed, broadly and purposively interpreting the legislation, and denied the loss relief.

The takeaway? HMRC and the Tribunal take a dim view of artificial steps taken solely to unlock old losses. If your loss carry-forward plan involves complex restructurings or new income streams that smell contrived, get proper advice early.

Claiming Carry-Forward Relief on the CT600, Boxes to Watch

When you finally have profits again:

- Box 160: Trading losses brought forward used this period.

- Box 240: Losses brought forward against trading profits (if streamed).

- Box 275: Trading losses carried forward to next period (what’s left after use).

Always attach a detailed computation showing:

- Pre- vs post-2017 split

- Deductions allowance claimed

- 50% restriction calculation

HMRC’s guidance stresses that white space explanations or separate notes are essential if the figures aren’t self-explanatory.

Common Pitfalls I See Every Year

- Assuming the full loss wipes out profits, forgetting the 50% cap bites above £5m.

- Failing to allocate the group allowance properly, leading to denial of relief.

- Not continuing “the same trade”, a change in trade can block carry-forward entirely (CTA 2010 s 45).

- Overlooking streamed losses for pre-2017 deficits.

- Missing the window to amend earlier returns if you later decide to carry back instead.

Run through this checklist before finalising your return:

- Trade continuing? Yes/No evidence?

- Pre/post-2017 losses separated?

- Deductions allowance allocated (group/single)?

- 50% restriction calculated correctly?

- Computation attached with full breakdown?

Tick these, and you’ll sleep easier.

Corporation Tax Reliefs: Claiming Losses & Carry-Forwards

An interactive guide to turning a trading loss into a refund or a lower future bill — same-period relief, carry-back, terminal loss relief, and the post-2017 carry-forward restriction. Includes live calculators and step-by-step worked examples.

● The four ways to get relief — and the order that counts

HMRC gives you options, but timing matters. The golden rule: never assume the default carry-forward is best. A carry-back can trigger an immediate cash repayment; a carry-forward only helps next year's profits.

- Same-period reliefSet the loss against other profits in the same accounting period. Simplest and most automatic — start here.

- Carry backCarry the loss back 1 year (or up to 3 years on cessation) for a fast refund.

- Group reliefSurrender the loss to other group companies (if you're in a group). Consider this before carrying forward.

- Carry forwardCarry it forward indefinitely against future profits — but watch the £5m + 50% restriction.

● Same-period relief — worked example

Widgets Ltd, year ended 31 Mar 2026:

The £80k loss wipes out trading profit and £35k of interest — no carry-forward or back needed.

● What changed for 2026

The loss-relief framework (in place since 2017) is unchanged. What shifts is the capital allowances interaction:

Timing investment correctly can deliberately create or enlarge a trading loss — useful where you want a carry-back refund.

● Terminal loss relief — when closing the doors still saves tax

If you cease trading completely, you can carry the loss back up to three years (latest year first) — far more generous than the normal one-year carry-back. Often the last tax-saving opportunity before the shutters come down. The claim process mirrors a normal carry-back, but you must clearly state it is a terminal loss claim and provide evidence the trade has ceased.

● Carry-back refund calculator

If same-period relief doesn't use the whole loss, carry it back one full year against profits of the same trade. The claim must be made within two years of the end of the loss-making period. Use the slider to choose how much of the loss to carry back.

● Step-by-step: the refund route most businesses miss

- Decide how much to carry backYou don't have to use all of it — match it to the prior-year profit.

- Reduce the prior-year profite.g. £150,000 − £80,000 = £70,000.

- Recalculate the tax dueCT on the reduced figure (with marginal relief where relevant).

- Claim the repaymentThe difference is repaid, plus interest.

- Complete the CT600Tick the earlier-period box and enter the carried-back amount correctly.

● Carry-forward restriction calculator (£5m + 50%)

Carried-forward losses last indefinitely while the trade continues. But for periods starting on/after 1 April 2017, you can only use the £5m deductions allowance plus 50% of remaining profits in any one year. The £5m is shared across a group.

● Pre- vs post-1 April 2017 losses

Pre-2017 losses can generally only be set against profits of the same trade (streamed). Post-2017 losses are more flexible — they can go against total profits. Both are caught by the £5m + 50% restriction when carried into post-2017 periods.

● Groups & the shared £5m

In a group, the £5m deductions allowance is shared. Nominate one company to allocate it via a group allowance allocation statement, filed with that company's CT600. A late or incomplete statement can mean HMRC denies part of the relief.

● CT600 — the boxes that matter

When the loss arises:

When profits return (carry-forward used):

● Pre-submit checklist

- ✓Kept separate records for pre- and post-1 April 2017 losses

- ✓Confirmed whether the trade continues or has genuinely ceased

- ✓Considered group relief first (if you're in a group)

- ✓Claim is within the two-year carry-back window

- ✓Double-checked capital allowances to maximise the loss

- ✓Deductions allowance allocated (group or single)

- ✓50% restriction calculated explicitly

- ✓Computation attached with full breakdown

● The Blackfriars Hotel case — don't try loss-refreshing tricks

In Blackfriars Hotel (UK) Holdings Ltd v HMRC [2024] UKFTT 1095 (TC), the First-tier Tribunal applied anti-avoidance rules designed to stop contrived arrangements that "refresh" carried-forward losses. The company had large non-trading loan relationship deficits carried forward, then entered arrangements involving new loans that generated profits — hoping to use the old losses against them.

HMRC invoked the targeted anti-avoidance rule (TAAR) under CTA 2010 s.730G, arguing the profits were "relevant profits" from a "tax arrangement". The Tribunal agreed — interpreting the legislation broadly and purposively — and denied the loss relief.

● Common pitfalls (tap to expand)

CTA 2010 s.45. Evidence continuity of the trade.● Summary — key insights

Carry-forward is indefinite while the trade continues — but post-2017 relief is limited to £5m + 50% of remaining profits.

The £5m allowance is per group — allocate it carefully via a group statement.

Keep pre- and post-2017 losses separate; they're treated differently.

Always calculate the 50% cap explicitly — many directors overstate relief.

Anti-avoidance rules (Blackfriars) catch contrived loss-refreshing — stick to genuine commercial steps.

Use the correct CT600 boxes (160, 240, 275) and attach detailed computations.

Terminal relief can bypass restrictions in the final year of trade — a valuable last chance.

If losses exceed immediate needs, weigh a faster carry-back refund against waiting for future profits.

Summary of Key Insights

- Carry-forward remains indefinite if the trade continues, but post-2017 restrictions limit relief to £5m deductions allowance plus 50% of remaining profits.

- The £5 million allowance is per group, allocate it carefully via a group statement to maximise use.

- Pre-2017 losses are usually restricted to same-trade profits, while post-2017 losses can offset total profits, keep them separate in records.

- Always calculate the 50% cap explicitly; many directors overlook it and overstate relief.

- Anti-avoidance rules (as in Blackfriars Hotel) catch contrived loss-refreshing arrangements, stick to genuine commercial steps.

- Use the correct CT600 boxes (160, 240, 275) and attach detailed computations showing splits and restrictions.

- Terminal carry-forward relief can bypass restrictions in the final year of trade, a valuable last-chance opportunity.

- Common errors include changing the trade nature, missing group allocations, and failing to evidence continuation.

- Review loss pots annually; small tweaks like timing capital allowances can create or preserve more usable losses.

- If losses exceed immediate needs, consider whether carry-back gives a faster cash refund than waiting for future profits.

There you have it, a practical roadmap through the loss rules as they stand in 2026. If your company has unused losses sitting on the balance sheet, now’s the time to model the best relief route. Drop me your headline figures if you’d like a quick sanity check, I’ve guided dozens through exactly this scenario.

FAQs

Q1: What happens to carried-forward trading losses if a company changes ownership?

In my experience advising business owners through sales and acquisitions, this is one question that catches even seasoned directors off guard. Under the rules, carried-forward losses can be restricted or lost if there’s both a change in ownership and a major change in the nature or conduct of the trade within a three-year window either side of the change. It’s not an automatic block, but HMRC looks closely at whether the business has fundamentally shifted, think moving from manufacturing widgets to providing software services. I once had a client in Birmingham who sold their family engineering firm and the new owners pivoted the operations; we had to fight to preserve the losses by proving continuity. Always model the impact early and consider restructuring options before signing any deal.

Q2: Can property business losses be carried forward and set against trading profits in future years?

Well, it’s a common mix-up for landlords who run their rentals through a limited company. Yes, unused UK property business losses can generally be carried forward indefinitely and deducted from the company’s total profits in later periods, including trading profits. This flexibility only applies to losses arising on or after 1 April 2017 though, older ones are more restricted. I’ve seen property companies in Leeds turn a corner after a rental slump by offsetting those losses against new trading income from a side business they launched. The key is keeping clear records separating property from trading activities so nothing gets disallowed on review.

Q3: How does surrendering carried-forward losses via group relief actually work in a group structure?

Picture this: you’ve got a profitable holding company and a loss-making subsidiary, group relief for carried-forward losses (post-2017 only) can be a lifesaver. The surrendering company can pass eligible losses to other group members to offset against their total profits, but only after the surrendering company has used its own deductions allowance. In practice, you need to file a group relief claim with the CT600 and make sure the companies meet the 75% ownership test throughout the overlapping period. One client group I worked with in Manchester saved over £80,000 in tax by timing the surrender correctly across two subsidiaries. Just be careful, you can’t surrender more than the claimant can actually use.

Q4: Are there any special options for carried-forward losses when a company enters liquidation?

None of us likes thinking about winding up, but the rules here can offer a final lifeline. Carried-forward trading losses generally cease once the trade stops, but if the liquidation is part of a genuine cessation you may still claim terminal relief for losses in the final period. Capital losses can sometimes be used differently too. I remember a client in Scotland whose engineering firm went into voluntary liquidation after 25 years, we managed to carry back some losses and offset capital gains on asset sales, recovering a useful repayment. Always involve an insolvency practitioner early so you don’t miss the window.

Q5: Do capital losses carried forward follow exactly the same rules as trading losses?

It’s a frequent point of confusion. Capital losses can only be carried forward and set against future capital gains, not against trading or other income profits. There’s no £5 million deductions allowance or 50% restriction like with income losses either. In one case I handled for a property development company near Manchester, unused capital losses from a previous failed project sat quietly until the company sold a site years later, wiping out a hefty chargeable gain. Keep them tracked separately on your balance sheet and never assume they can offset trading profits.

Q6: What if my company starts a completely different trade, can old carried-forward losses still be used?

Be careful here, because the “same trade” test is stricter than many realise. Pre-2017 losses can only go against future profits of the same trade, and even post-2017 losses can be blocked if the new activity is so different it amounts to a new trade. I’ve seen a retail client in London try to use old shop losses against a new online consultancy arm, HMRC challenged it successfully. The lesson? Document how the new activity links back to the old one if you want to preserve relief, and consider restructuring before the change.

Q7: How are non-trading loan relationship deficits treated when carried forward?

In my 15 years helping companies with financing arrangements, this one trips up businesses with heavy debt. Non-trading loan relationship deficits (NTLRDs) arising after 1 April 2017 can be carried forward and set against total profits, including trading ones, subject to the usual restrictions. Older ones are limited to non-trading profits. One client, a property investor in Cardiff, had substantial interest deficits from development loans; once profits returned we offset them neatly against rental income. Always separate these from trading losses in your computations.

Q8: Can carried-forward losses be used if the company has been dormant for several years?

It depends on whether the trade has genuinely continued or ceased. If the company is dormant but the trade is merely paused (with genuine intention to resume), losses can usually be preserved. But if HMRC views it as a new trade on reactivation, relief may be lost. I once advised a tech start-up in Edinburgh that went dormant for two years during funding talks, we kept detailed board minutes showing continuity and successfully used the losses later. Keep the company active on paper if you want to safeguard those losses.

Q9: Do carried-forward losses interact with R&D tax credits or the patent box in any special way?

This is where planning gets interesting. R&D expenditure credits or enhanced deductions can actually create or increase a loss that then carries forward, but you can’t claim both the credit and loss relief on the same expenditure in a way that double-dips. With the patent box, losses can reduce the qualifying profits before the reduced 10% rate applies. One manufacturing client I worked with maximised both by timing their R&D claims carefully around profitable years. Always run the numbers both ways, it can make a surprising difference.

Q10: What evidence does HMRC typically ask for to prove a trade is still continuing for loss carry-forward purposes?

In practice, HMRC wants more than just a company registration. Board minutes showing ongoing activity, contracts, marketing efforts, or even website updates can all help. I’ve had clients whose losses were queried after a quiet period, we submitted supplier invoices and customer emails to demonstrate the trade hadn’t stopped. It’s worth keeping a simple “trade continuity” file; it has saved several repayments during enquiries.

Disclaimer

The information provided in this article is for general guidance only and is not intended to constitute professional advice, tax advice, financial advice, legal advice, or any other form of regulated guidance. Although every effort has been made to ensure accuracy at the time of publication, Fair View Accounting Services, including its director, employees, contractors, writers, and content-creation team, accepts no responsibility for any loss, damage, penalty, or consequence arising from reliance on the information contained herein.

UK tax legislation changes frequently, and HMRC interpretations, thresholds, and rules may vary depending on the individual circumstances of each taxpayer. Nothing in this article should be considered a substitute for obtaining formal, personalised advice from a qualified accountant or tax professional. Readers should not take action—or refrain from taking action—based solely on the content published on this website.

Fair View Accounting Services does not guarantee the completeness, accuracy, or ongoing validity of the information provided and assumes no liability for omissions or errors, whether typographical, factual, or technical. By using this content, the reader acknowledges that all responsibility for decisions remains solely with the user.