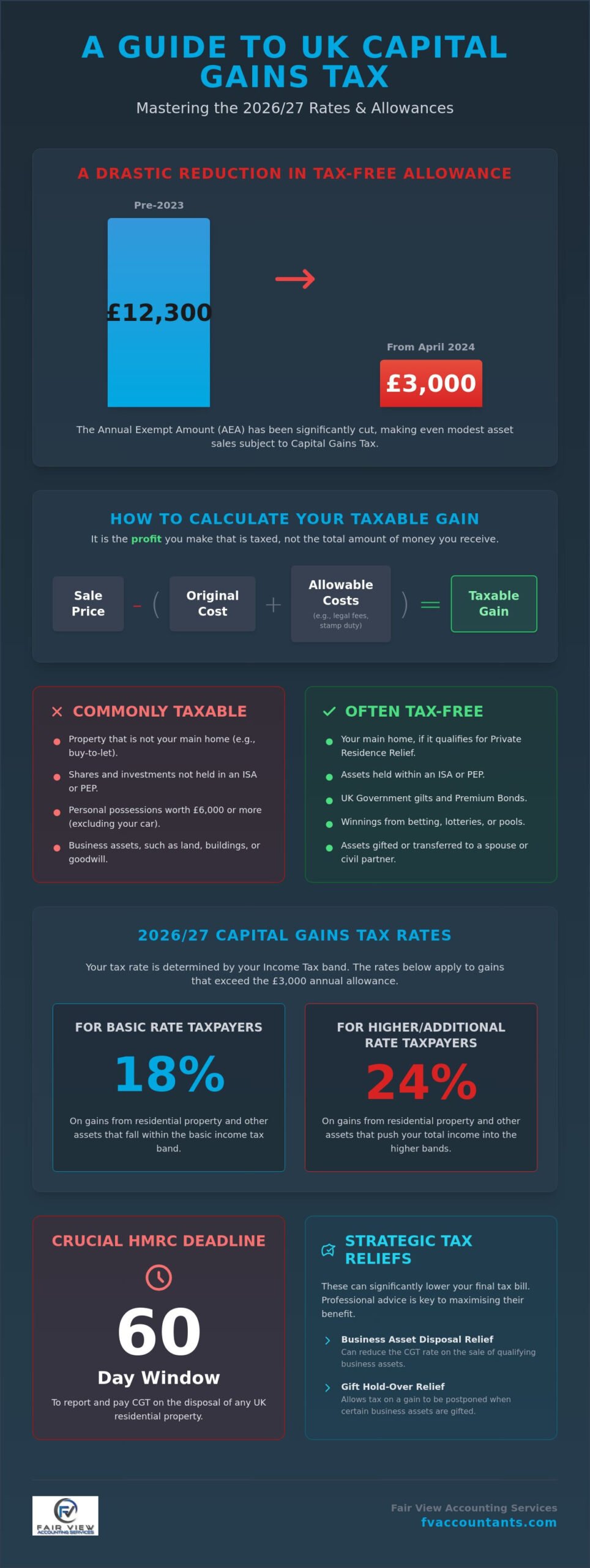

The annual exempt amount for Capital Gains Tax has plummeted from £12,300 to just £3,000 in a remarkably short period, which means that even modest asset sales now trigger a mandatory conversation with HMRC. You likely feel that the goalposts are constantly shifting, making it difficult to distinguish your actual taxable gain from your total proceeds. It is entirely natural to worry about overpaying due to missed reliefs or falling foul of the strict 60-day reporting rules for residential property sales.

We believe that tax compliance should offer peace of mind rather than a source of stress. Our guide helps you master the 2026 rates and allowances, providing a clear path to protect your financial position through strategic planning. We will examine the current 18% and 24% thresholds, explain how to utilise Business Asset Disposal Relief effectively, and outline the exact steps required to ensure 100% compliance. By the end of this article, you will have a professional framework to minimise your liability legally and navigate the modern tax landscape with absolute confidence.

Key Takeaways

- Learn how to accurately calculate your taxable gain rather than your total sale proceeds to ensure you only pay what is legally required.

- Understand how your 2026 income levels dictate whether you fall into the 18% or 24% Capital Gains Tax bracket for your specific assets.

- Discover strategic reliefs such as Business Asset Disposal Relief and Gift Hold-Over Relief that can significantly lower your tax liability.

- Master the strict 60-day reporting and payment window for residential property disposals to avoid costly HMRC penalties.

- Gain clarity on how proactive professional planning identifies modern tax-saving opportunities that generic software often overlooks.

Understanding Capital Gains Tax: What You Pay it On in 2026

Capital Gains Tax is a levy on the profit you make when you sell or “dispose of” an asset that has increased in value. It is the gain you make that is taxed, not the total amount of money you receive. For instance, if you purchased a painting for £5,000 and later sold it for £12,000, your taxable gain is £7,000. Understanding the historical context and foundational rules of Capital Gains Tax in the UK helps clarify why HMRC monitors these transactions so closely.

Confusing the total proceeds of a sale with the actual taxable gain is a frequent error that leads to overpayment. To calculate the gain accurately, you must deduct the original purchase price and certain allowable costs, such as legal fees or stamp duty, from the final sale price. This precision ensures you only pay tax on the genuine growth of your investment. We focus on these fine details to protect your financial position from unnecessary leakage.

A common misconception is that tax only applies when cash changes hands. In the eyes of HMRC, a “disposal” occurs whenever you stop owning an asset. This includes gifting an item to someone else, swapping it for something different, or receiving compensation for it, such as an insurance payout after an asset is destroyed. When you gift an asset to anyone other than a spouse or civil partner, you must use the current market value to calculate the gain. Professional valuations are essential here; they prevent disputes with tax authorities and ensure your filings remain beyond reproach.

Common Taxable Assets for UK Taxpayers

Most personal and business assets fall under the scope of Capital Gains Tax. You should prepare for a potential tax liability when disposing of the following items:

- Personal possessions: Any items worth £6,000 or more, excluding your private car.

- Property: Any buildings or land that do not qualify as your main residence, such as buy-to-let investments or holiday homes.

- Shares: Investments held outside of a tax-efficient wrapper like an ISA or PEP.

- Business assets: This includes land, buildings, machinery, and even “goodwill” when selling a trading entity.

For landlords and business owners, managing these assets involves navigating various regulatory requirements. Alongside tax planning, ensuring your properties meet safety standards is crucial, and UK Fire Risk Assessments offers professional guidance to help you remain compliant with fire safety laws.

What Qualifies as a Tax-Free Asset?

Not every profit is subject to HMRC’s reach. Private Residence Relief usually ensures you pay no tax on the sale of your primary home, provided it has been your only residence throughout your ownership. Other exempt categories include:

- ISAs and GILTs: Gains made within Individual Savings Accounts or from UK Government gilts are protected from tax.

- Winnings: Profit from betting, the National Lottery, or football pools is entirely tax-free.

- Spousal Transfers: Assets gifted to a husband, wife, or civil partner are generally exempt, allowing for effective “inter-spousal” planning to utilise both annual allowances.

Calculating Your Liability: 2026 Rates and Allowances

For the 2026/27 tax year, the Annual Exempt Amount (AEA) for individuals is set at £3,000. This figure represents a sharp decline from previous years, leaving taxpayers with a much smaller margin for tax-free growth. If your total gains exceed this threshold, you are legally required to report them. Consulting the official government guidance on Capital Gains Tax provides a baseline for compliance, but the actual calculation of your bill depends heavily on your total annual income.

CGT Rates for Individuals

Your Income Tax band directly dictates the percentage of tax you pay on your gains. For the 2026/27 period, basic rate taxpayers generally face a rate of 18% on gains from residential property and other assets. If your combined income and capital gains push you into the higher or additional rate brackets, this rate increases to 24%. To find your band, you must add your taxable gain to your income from salary, pensions, and dividends. If the total exceeds the basic rate threshold, the higher rate applies to the portion of the gain that sits above that line. We provide comprehensive support with Capital Gains Tax filings to ensure you apply the correct rates and avoid overpayment.

The Annual Exempt Amount: Use it or Lose it

The £3,000 allowance is a strictly annual benefit. You cannot carry any unused portion forward to the next tax year, which makes timely asset disposal a critical planning component. Some individuals utilise “bed and ISA” strategies to sell assets, use their allowance, and immediately repurchase them within a tax-free wrapper. Alternatively, transferring assets to a spouse or civil partner before a sale can effectively double your exempt amount to £6,000, as each person holds an individual allowance. This simple transfer can protect a significant portion of your wealth from unnecessary taxation.

You can also reduce your liability by utilising losses from previous tax years. If you sold an asset for less than you paid for it, that loss can be “carried forward” to offset future gains. You must report these losses to HMRC within four years of the end of the tax year in which the loss occurred. Maintaining precise records of these losses ensures that when you do make a significant gain, you have a legitimate mechanism to lower your final bill.

Identifying Strategic Reliefs to Reduce Your Bill

Reducing your final tax liability requires a move from simple calculation to proactive strategy. Whilst the headline rates can seem high, the UK tax system provides several mechanisms to defer or decrease the amount you owe. Identifying the right relief early in the disposal process ensures you keep more of your hard-earned profit. You can find a complete list of available options in the Official GOV.UK Capital Gains Tax guidance, but applying them to your specific circumstances often requires a more nuanced approach.

Business Asset Disposal Relief (BADR)

BADR remains one of the most effective tools for entrepreneurs and shareholders looking to exit a business. To qualify, you must have owned at least 5% of the shares and voting rights in a trading company for at least two years prior to the sale. You also need to be an employee or office holder of that company. BADR provides a preferential 18% tax rate for qualifying business disposals, significantly reducing the liability for entrepreneurs. This relief is subject to a £1 million lifetime limit. Once you exceed this threshold, any further qualifying gains are taxed at the standard 24% rate. We help you track your lifetime usage to ensure your exit strategy remains tax-efficient.

Other business-focused reliefs allow for the deferral of tax rather than an immediate payment. Gift Hold-Over Relief is particularly useful when passing business assets to others without receiving payment; the tax is deferred until the recipient eventually sells the asset. Similarly, Business Asset Rollover Relief allows you to defer paying Capital Gains Tax if you sell a trade asset and reinvest the proceeds into a replacement asset within specified time limits. This supports business growth by keeping capital within the company rather than losing it to immediate taxation.

Property-Specific Reliefs and Deductions

Property disposals often involve significant costs that can be used to lower your taxable gain. HMRC allows you to deduct the expenses of buying and selling, such as solicitor fees, estate agent commissions, and stamp duty. You can also deduct the cost of capital improvements. This includes permanent additions like an extension or a new conservatory, but it does not include general maintenance like repainting or fixing a roof. Distinguishing between these two categories is vital for an accurate filing.

For those who have let out a property that was once their main home, Lettings Relief may provide additional protection. However, its scope in 2026 is limited to situations where the owner lived in the property at the same time as the tenant. Transfers between spouses or civil partners also remain a cornerstone of effective planning. By transferring a portion of an asset to a partner before a sale, you can utilise two sets of annual allowances and potentially access lower tax bands if one partner has a lower annual income.

HMRC Compliance: Reporting and Paying on Time

Compliance isn’t just about paying the right amount; it’s about doing so within the strict windows HMRC defines. For 2026, the complexity of reporting has increased due to tighter digital oversight. Whether you’ve sold shares or a second home, your reporting route depends entirely on the asset type. Missing these windows leads to immediate financial penalties that can erode your investment profits. We prioritise precision to ensure your filings are both timely and accurate.

The 60-Day Property Rule

If you dispose of a UK residential property that isn’t your main home, you face the most aggressive deadline in the UK tax system. You must report and pay the Capital Gains Tax due within 60 days of the completion date. This isn’t done through your usual tax return. Instead, you must set up a specific “Capital Gains Tax on UK Property” account through the GOV.UK portal. This requires a Government Gateway user ID and specific details about the property’s acquisition and sale.

The process involves calculating your gain, applying your £3,000 allowance, and making an estimated payment. If you miss this 60-day window, HMRC applies an initial £100 penalty. Interest begins accruing from day 61, and further penalties apply if the return is more than three months late. Professional filing ensures these estimates are accurate, preventing a situation where you overpay upfront or face a “top-up” bill with interest later. If you need assistance meeting this deadline, our team can manage your Capital Gains Tax reporting to ensure total compliance.

For assets like shares, business equipment, or personal possessions, the timeline is more traditional. You report these through your annual Self Assessment tax return. For a gain made in the 2026/27 tax year, you have until 31 January 2028 to file and pay. Some taxpayers prefer the “Real Time” Capital Gains Tax Service. This allows you to report and pay as soon as the sale is finished rather than waiting for the end of the year, which can help with personal cash flow management.

Digital Record Keeping for Modern Taxpayers

HMRC requires you to keep records for at least 22 months after the end of the tax year in which you sold the asset. For business assets, this requirement extends to five years. We take a “tech-savvy guardian” approach by integrating cloud platforms like Xero and Dext into your workflow. These tools allow you to capture and store essential evidence the moment a transaction occurs; businesses needing robust infrastructure for such systems can discover SolaaS Limited for scalable IT support.

Storing digital images of solicitor letters, valuation reports, and improvement receipts ensures no deduction is forgotten. Lost paperwork is the primary reason taxpayers overpay. Digital integration provides real-time visibility of your potential liabilities, allowing you to set aside the necessary funds well before the deadline arrives. This methodical approach transforms a stressful administrative task into a streamlined, manageable process that protects your financial stability.

Why Professional CGT Planning is Essential

Tax software often treats compliance as a static calculation. However, Capital Gains Tax is a dynamic variable that responds to your specific financial history and future goals. Fair View Accounting Services provides the professional oversight required to uncover hidden reliefs that automated platforms frequently miss. We identify niche opportunities, such as negligible value claims or complex loss offsets, that generic tools aren’t programmed to recognise. This methodical approach ensures you never pay more than is legally required.

Our tailored solutions cater specifically to those with complex portfolios, including e-commerce sellers and multi-property landlords. We organise your digital records to ensure every allowable expense is captured, which directly reduces your final bill. This proactive approach prevents overpayment and ensures you remain 100% compliant with HMRC regulations. Accurate filings lead to total peace of mind. You can focus on your next investment whilst we handle the administrative burden.

Beyond the Calculator: Professional Oversight

Automated calculators struggle with nuanced transactions. If you’re dealing with a “part-disposal” of land or an exit strategy involving “deferred consideration”, the risk of error is high. We provide the stability and expertise needed to navigate these complexities. Having a chartered accountant handle HMRC enquiries provides an invaluable layer of security. We ensure your interests are protected during any regulatory review and centre your financial affairs on long-term efficiency.

- Precision: We verify every figure to prevent costly amendments.

- Security: Our team acts as your dedicated point of contact for HMRC.

- Growth: We identify how current disposals affect your future tax position.

Next Steps: Securing Your Financial Future

Timing is the most critical factor in tax efficiency. You should contact an accountant before your sale is finalised to ensure all reliefs are properly structured and documented. Our modern, online approach allows us to support clients across the United Kingdom with seamless digital integration. We combine traditional expertise with contemporary efficiency to make your tax obligations feel manageable and under control.

Ensure your Capital Gains Tax is handled with precision by Fair View Accounting Services. Our proactive guidance transforms a stressful requirement into a streamlined part of your financial growth strategy.

Securing Your Assets for the Long Term

Managing Capital Gains Tax in 2026 requires a proactive approach that blends traditional regulatory knowledge with modern digital tools. You’ve seen how the reduced £3,000 allowance and the 60-day reporting window for property sales leave very little room for administrative error. By distinguishing your taxable gain from your total proceeds and identifying strategic reliefs early, you can protect your financial position and avoid unnecessary HMRC penalties.

As Chartered Accountants with national UK coverage, Fair View Accounting Services specialises in cloud-based tax compliance for landlords and SMEs. We provide the methodical oversight needed to ensure your filings are 100% accurate and submitted well before the deadline. We invite you to book a Capital Gains Tax consultation with Fair View Accounting Services to streamline your reporting process. Our team is here to act as your tech-savvy guardian, ensuring your wealth remains protected and your compliance is seamless. You can move forward with your next investment knowing your tax affairs are in expert hands.

Frequently Asked Questions

Do I have to pay Capital Gains Tax if I sell my main home?

You usually don’t pay any tax when selling your main home because of Private Residence Relief. This relief applies automatically if the property has been your only or main residence throughout the entire period of ownership. You may have a liability if the grounds exceed 0.5 hectares, if you used part of the home exclusively for business, or if you let out part of the property.

What is the Capital Gains Tax allowance for the 2025/26 tax year?

The annual exempt amount for the 2025/26 tax year is £3,000 for individuals. This tax-free threshold is also set to remain at £3,000 for the 2026/27 tax year. It’s important to remember that this is a “use it or lose it” allowance. You cannot carry any unused portion of the £3,000 over into the next tax year.

How much time do I have to report a property sale to HMRC?

You must report and pay any Capital Gains Tax due on the sale of a UK residential property within 60 days of the completion date. This deadline is strictly enforced by HMRC. For other types of assets, such as shares or business machinery, you report the gains through your annual Self Assessment tax return by 31 January following the end of the tax year.

Can I give my assets to my spouse to avoid Capital Gains Tax?

Gifting assets to a spouse or civil partner is treated as a “no gain, no loss” transfer, meaning no Capital Gains Tax is due at the time of the gift. This is a common planning strategy used to utilise two sets of annual allowances. It can also help move the gain to a partner who sits in a lower Income Tax bracket, potentially reducing the rate from 24% to 18% on the final sale.

What expenses can I deduct to reduce my Capital Gains Tax bill?

You can deduct the costs of buying and selling the asset to lower your taxable gain. Allowable expenses include solicitor fees, estate agent commissions, and any Stamp Duty Land Tax paid when you originally purchased the asset. You can also deduct the cost of capital improvements, such as a loft conversion or a permanent extension, but you cannot deduct general maintenance or repair costs.

Is Capital Gains Tax different for limited companies?

Limited companies don’t pay Capital Gains Tax. Instead, they pay Corporation Tax on any “chargeable gains” made from selling business assets. The gain is calculated similarly to an individual’s gain but is added to the company’s total taxable profits. It is then taxed at the prevailing Corporation Tax rate, which currently sits between 19% and 25% depending on the company’s profit levels.

What happens if I make a loss on an asset sale?

If you sell an asset for less than you paid for it, you can use that loss to reduce the total gains you’ve made in the same tax year. If your total losses are greater than your gains, you can carry the unused losses forward to offset against gains in future years. You must report these losses to HMRC within four years of the end of the tax year in which the loss occurred.

How do I pay my Capital Gains Tax bill online?

You pay your bill online through the GOV.UK portal using a debit card or via a bank transfer. For residential property, you must pay through your “Capital Gains Tax on UK Property” account. For other assets, you pay through the Self Assessment system using your Unique Taxpayer Reference. Using digital payment methods ensures your payment is tracked accurately and credited to your account without delay.

Disclaimer

The information provided in this article is for general guidance only and is not intended to constitute professional advice, tax advice, financial advice, legal advice, or any other form of regulated guidance. Although every effort has been made to ensure accuracy at the time of publication, Fair View Accounting Services, including its director, employees, contractors, writers, and content-creation team, accepts no responsibility for any loss, damage, penalty, or consequence arising from reliance on the information contained herein.

UK tax legislation changes frequently, and HMRC interpretations, thresholds, and rules may vary depending on the individual circumstances of each taxpayer. Nothing in this article should be considered a substitute for obtaining formal, personalised advice from a qualified accountant or tax professional. Readers should not take action or refrain from taking action based solely on the content published on this website.

Fair View Accounting Services does not guarantee the completeness, accuracy, or ongoing validity of the information provided and assumes no liability for omissions or errors, whether typographical, factual, or technical. By using this content, the reader acknowledges that all responsibility for decisions remains solely with the user.