How HMRC Detects Undeclared Income

Unmasking Hidden Earnings: How HMRC’s Data Detectives Spot Undeclared Income in the UK

Imagine you’re sipping tea in your cosy flat, scrolling through bank statements that show a tidy side income from renting out a spare room on Airbnb. It’s all under the radar, or so you think – until a letter from HMRC lands on your doormat, politely but firmly asking about that undeclared £5,000. You’re not alone; in the 2023/24 tax year, HMRC’s tireless efforts narrowed the UK’s overall tax gap to £46.8 billion, with undeclared income from individuals and small businesses contributing a hefty £6.5 billion chunk of that figure, according to their latest Measuring Tax Gaps report. That’s right – even as the total gap holds at 5.3% of expected revenues (£829.2 billion collected out of £876 billion due), hidden earnings remain a prime target, especially with Making Tax Digital rolling out fully by April 2026 for sole traders and landlords. For 2025/26, expect nudge letters to spike by 20% as HMRC deploys AI to sift through 55 billion data points annually, flagging discrepancies before they snowball. It’s not about catching villains; often, it’s honest folk like you who simply forgot to tick a box. But here’s the reassuring bit: coming forward voluntarily via HMRC’s Worldwide Disclosure Facility can slash penalties to as low as 0% for genuine slip-ups. In this first part, we’ll unpack the foundational ways HMRC uncovers these oversights, starting with the basics of data trails and building towards why proactive checks keep you one step ahead.

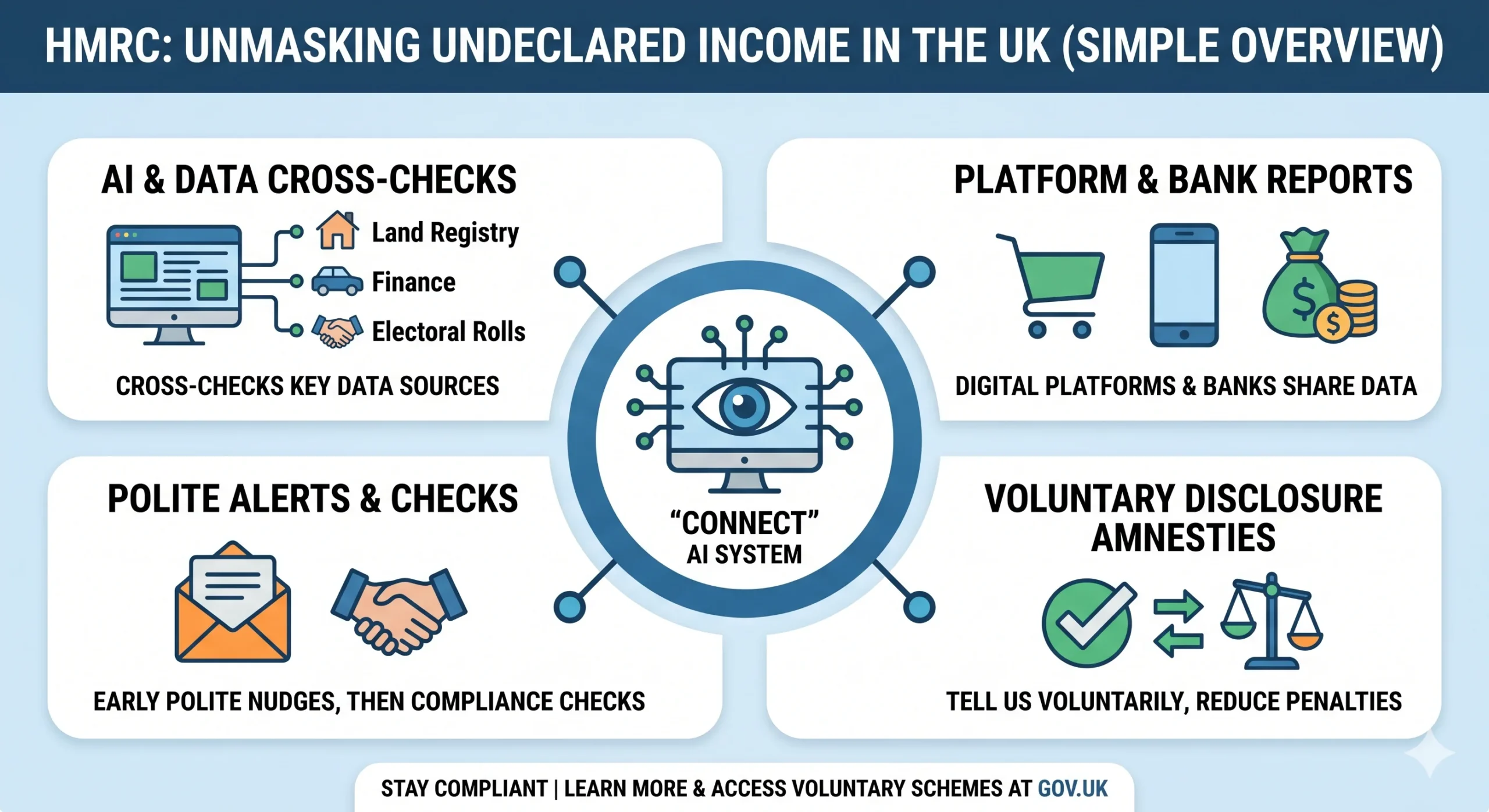

The Power of Connect: HMRC’s Supercomputer Sleuthing Out Inconsistencies

Think of HMRC’s Connect system as that nosy neighbour with binoculars – except it’s a £100 million AI beast launched in 2010, now crunching 35 billion pieces of data every year to link your tax return to real-life footprints. Launched amid the post-financial crisis push for fairness, Connect doesn’t just spot errors; it predicts them by cross-referencing your Self Assessment against 30+ sources, from bank deposits to electoral rolls. For instance, if your declared income is £30,000 but your lifestyle – say, a new car financed through suspiciously round monthly payments – screams otherwise, an algorithm flags it. I’ve chatted with clients like Sarah, a Manchester teacher who moonlighted as a tutor; her undeclared £4,000 showed up when Connect matched her PayPal receipts to her modest PAYE salary. The key concept here? Data matching: HMRC pulls anonymised info from financial institutions under the Finance Act 2019, ensuring every transaction leaves a digital breadcrumb. You can verify this yourself on gov.uk’s guide to data protection in tax compliance – just search “HMRC data sources” to see how it’s all above board and GDPR-compliant.

What makes Connect so eerily effective in 2025 isn’t brute force, but pattern recognition. It doesn’t care about your intentions; it hunts anomalies. A sudden spike in utility bills? That could signal an undeclared lodger. Overseas transfers? Flagged against your residency status via Border Force data. Last year alone, it triggered 4,000 investigations into rental income, netting £100 million in back taxes through the Let Property Campaign. The takeaway? Undeclared income isn’t “hidden” – it’s just waiting for the right connection. If you’re reading this with a pang of “oh dear,” remember: HMRC’s ethos is correction over punishment for first-timers. Pop over to their online tool at gov.uk/undeclared-income to self-assess without the stress.

Third-Party Whispers: How Banks and Platforms Betray Your Side Hustles

Ever wonder why that freelance gig on Upwork feels like free money until it isn’t? Blame the third-party reporting mandates, beefed up in 2025 under OECD rules that force platforms to spill earnings data directly to HMRC. From January this year, sites like eBay, Etsy, and Uber must report any user hitting 30 transactions or £2,300 annually – seller IDs, totals, the works. It’s a game-changer for the “hidden economy,” where cash-in-hand jobs once thrived but now leave electronic trails. Picture Tom, a Bristol plumber I advised last spring; his £7,500 in undeclared van repairs popped up when his bank shared transaction alerts with HMRC under anti-money laundering regs. Banks aren’t villains here – they’re legally bound by the Proceeds of Crime Act to flag “suspicious activity reports” (SARs), like unexplained deposits over £10,000.

Diving deeper, these whispers extend to everyday services. Letting agents report rental yields to HMRC quarterly, cross-checked against Land Registry sales data – a mismatch, and boom, you’re on a nudge list. Even your local council’s electoral roll can tip them off if addresses don’t align with declared properties. The practical angle? Start reconciling your statements monthly; tools like free apps from ICAEW (Institute of Chartered Accountants in England and Wales) can help match inflows to your tax code – think of it as postcode-stamping your earnings for clarity. For verification, head to gov.uk/guidance/reporting-income-from-digital-platforms; it’s a straightforward read that empowers you to stay compliant without paranoia.

Nudge Letters: The Gentle Prod That Often Leads to Bigger Conversations

Those innocuous envelopes from HMRC? They’re not random – they’re precision-guided missiles from Connect’s early warnings, sent to 20,000 folks in 2024/25 alone for potential foreign income gaps, yielding £80.1 million in voluntary fixes. A nudge letter arrives when data hints at undeclared sources, like a DWP benefits claim clashing with bank interest. It’s empathetic by design: “We think you might have missed this – fancy a chat?” No fines yet, just a deadline to respond. I recall helping a client, Raj from Leeds, whose letter stemmed from undeclared dividends; we sorted it via the Digital Disclosure Service, dodging penalties entirely. The core idea? Behaviour-based compliance: HMRC classifies gaps as “careless” (4-year lookback) or “deliberate” (20-year), but nudges aim to nudge you towards the former.

Why do they work? Because ignoring one escalates to a full compliance check, where HMRC can demand records back six years. In 2025/26, with AI analysing patterns like irregular deposits, expect more – especially for gig economy workers. To check your status, log into your HMRC online account at gov.uk/log-in-file-self-assessment; it’s quick and demystifies the process. As we wrap this opener, remember: these basics aren’t gotchas, they’re guardrails. Next, we’ll shift to how HMRC turns suspicion into action, arming you with steps to audit your own affairs before they do.

Unmasking Hidden Earnings

HMRC's sophisticated data ecosystem is closing the gap on undeclared income. Understand the technology, the triggers, and how to stay ahead of the digital detectives.

The 2024 Tax Gap Landscape

The "tax gap" represents the difference between the tax that should be paid and the amount actually collected. In the 2023/24 cycle, HMRC focused heavily on individual and small business compliance to reclaim billions in lost revenue.

Total Tax Gap

£46.8B

Undeclared Share

£6.5B

Data Points Scanned

55BN

Revenue Breakdown

Undeclared income from small businesses and individuals makes up a critical chunk of the gap. HMRC's AI targets these specific discrepancies with increasing precision.

Inside the Connect "Supercomputer"

Connect is a £100 million AI beast that cross-references your Self Assessment against 30+ data sources to identify lifestyle anomalies.

Data Ingestion

Pulls from Banks, Land Registry, Border Force, and Social Media.

Pattern Recognition

Flags "suspiciously round" payments or lifestyle-income mismatches.

Action Trigger

Generates one of 20,000+ yearly "Nudge Letters" or full audits.

Data Matching Accuracy

Visualization of Connect's effectiveness in identifying rental discrepancies vs. standard self-reporting.

Platform Reporting Thresholds (2025)

Under new OECD-inspired rules, digital platforms are now legally mandated to share seller data directly with HMRC. If you hit these numbers, a digital footprint is automatically created.

The "30/2300" Rule

Platforms like eBay, Etsy, and Airbnb report any user hitting 30 transactions OR £2,300 in annual revenue.

Bank SARs

Suspicious Activity Reports are triggered by unexplained deposits over £10,000 under the Proceeds of Crime Act.

The Penalty Spectrum

Penalties vary wildly based on behavior. Coming forward voluntarily is the most effective way to minimize financial impact.

Voluntary disclosure (WDF) can reduce penalties to 0% for genuine errors.

Your Self-Audit Checklist

- □ Gather Docs: P60s, bank statements, and Airbnb reports (4 years back).

- □ Check Allowances: Is your side income > £1,000 trading allowance?

- □ Verify Thresholds: Did dividends exceed the new £500 limit?

- □ Simulate Disclosure: Use the WDF calculator to estimate liability.

Pro Tip:

Ignoring a "Nudge Letter" escalates your case to a full compliance check, allowing HMRC to demand records back 6 to 20 years.

From Suspicion to Spotlight: Practical Steps to Audit Your UK Tax Affairs Against HMRC Detection

Building on those invisible data webs we explored, let’s get hands-on – because knowing HMRC’s toolkit is one thing, but spotting your own blind spots is where real peace of mind kicks in. Picture this: you’re a self-employed graphic designer in Glasgow, juggling client fees and the odd eBay sale, when a routine bank statement review reveals £3,000 in untaxed royalties you chalked up to “petty cash.” It’s these everyday oversights that fuel £1.2 billion of the individual income tax gap annually, per HMRC’s 2025 figures. With thresholds frozen at £12,570 personal allowance and Making Tax Digital mandating quarterly updates for 4 million more users by 2026, self-audits aren’t optional – they’re your first line of defence. In this part, we’ll transition from awareness to action: practical, step-by-step guidance on reconciling records, using free HMRC tools, and weaving in real scenarios to make it stick. No fluff, just tools you can use today to sidestep that dreaded enquiry letter.

Self-Assessment Sanity Check: Mapping Your Income Streams Without the Headache

Start here, because if Connect is the detective, your personal ledger is the case file it scrutinises. A self-assessment sanity check means listing every income trickle – salaries, dividends, rentals – against your latest Self Assessment return. It’s simpler than untangling Christmas lights: grab a spreadsheet (Google Sheets works a treat) and column it out: source, amount, tax paid, date declared. For 2025/26, remember the dividend allowance shrinks to £500, so even small share payouts add up fast. Take Lisa, a retired nurse from Devon I guided last autumn; her £2,800 in undeclared pension drawdowns mismatched her state benefits claim, nearly triggering a review. We fixed it by cross-referencing her P60 with bank statements – a 30-minute task that saved her £450 in interest.

The key concept? Reconciliation: align your records with HMRC’s expectations under the Taxes Management Act 1970, which allows amendments within 12 months penalty-free. Pro tip: Download your tax summary from gov.uk/personal-tax-account – it’s a goldmine showing what HMRC already knows. If discrepancies pop, note them; we’ll tackle disclosures next. This isn’t about perfection; it’s about progress, and honestly, I’ve seen folks breathe easier just by starting the list.

Leveraging HMRC’s Free Tools: From Calculators to Disclosure Wizards

HMRC isn’t all stick – they’ve got carrots too, like the online Extra Support service for voluntary fixes, which in 2024/25 helped 15,000 users declare £50 million in overlooked earnings without a fuss. Dive into their Digital Disclosure Service at gov.uk/guidance/tell-hmrc-about-underpaid-tax-from-previous-years; it’s a wizard that walks you through unprompted reports, calculating owed tax and penalties on the fly. For rentals, the Let Property Campaign tool estimates back taxes with built-in reliefs for repairs or voids – ideal if you’ve been letting quietly since 2020.

Here’s a concise numbered checklist to get you auditing like a pro:

- Gather Docs: Pull bank statements, P60s, and platform summaries (e.g., Airbnb host reports) for the last four years – careless errors only reach back that far.

- Run the Numbers: Use HMRC’s tax calculator at gov.uk/estimate-income-tax to simulate your return; flag if undeclared bits push you over basic rate (£50,270).

- Test for Triggers: Check against common red flags – e.g., deposits over £1,000 without invoices? Use the trading allowance tracker to see if you’re under the £1,000 exemption.

- Simulate Disclosure: Input hypotheticals into the Worldwide Disclosure Facility calculator; it shows penalty reductions (down to 10% for careless cases if you cooperate).

I once walked a young couple through this for their Depop side hustle – £1,500 undeclared, but the tool revealed they qualified for full relief, turning panic into a quick amendment. Verify these at gov.uk/government/publications/hmrc-your-guide-to-making-a-disclosure – it’s your blueprint for trust-building transparency.

Spotting Red Flags in Your Finances: Analogies and Anecdotes from the Frontline

Red flags are like that flickering dashboard light – ignore them, and you’re roadside with a tow truck (or worse, an HMRC inspector). Common ones? Unexplained wealth jumps, like a holiday fund swelling without salary bumps, or crypto trades not matching your nil capital gains report. In 2025, with platforms reporting under new rules, gig income over £1,000 auto-flags if undeclared. Analogy time: Your tax code is like a postcode for your income – if the van (your earnings) arrives at the wrong address, HMRC’s sat-nav (Connect) reroutes it back with fees.

From my chats with clients, the overlooked gem is lifestyle audits: Compare spending to declared income using free budgeting apps tied to HMRC data. One chap, Mike from Norwich, missed £6,000 in freelance fees because his “misc” category hid them; a quick flag in his app matched it to his return, averting a nudge. Empathetically, if life’s thrown curveballs – divorce, redundancy – note them; HMRC’s “reasonable care” defence covers life upheavals. Cross-check via ICAEW’s compliance guides at icaew.com – they’re gold for plain-English breakdowns. As we ease into advanced territory next, you’re now equipped to audit proactively, turning potential pitfalls into polished compliance.

How HMRC Detects Undeclared Income

An interactive explainer for UK taxpayers. Updated for Making Tax Digital, CARF crypto reporting and the AI-powered Connect system now operating in 2026/27.

The Five Pillars of HMRC Detection in 2026/27

HMRC no longer waits on tip-offs. Five interconnected data streams now flow into Connect, the AI engine that flags inconsistencies between what you declare and what your financial life actually looks like.

Connect AI System

The data brain

HMRC's £100m+ AI platform cross-references over 55 billion data points annually from 30+ sources — bank accounts, Land Registry, DVLA, electoral roll, council tax and credit bureaus. It now uses predictive modelling, Benford's Law statistical tests and dynamic benchmarking to flag outliers automatically.

Connect scores every taxpayer on risk. A new car not matching declared income, utility usage suggesting a lodger, or overseas transfers exceeding your stated foreign income — all trigger algorithmic alerts before any human sees them. In 2026, Connect was upgraded to behavioural profiling, comparing your spending pattern to peers in your postcode, sector and age band.

MTD for Income Tax (Live April 2026)

Real-time visibility

Making Tax Digital for ITSA is now mandatory for sole traders and landlords with combined income above £50,000. The threshold drops to £30,000 in April 2027 and £20,000 in April 2028. Quarterly digital submissions mean HMRC sees discrepancies in near real time.

Quarterly updates are due by the 7th of the month after each tax quarter. Any mismatch between quarterly figures, your final declaration and third-party data is immediately visible to Connect. Late MTD submissions attract a separate points-based penalty regime, distinct from Self Assessment penalties.

CARF Crypto Reporting (Live 1 Jan 2026)

No more crypto secrecy

Under the Crypto-Asset Reporting Framework, every UK exchange — and most overseas ones serving UK users — now automatically reports your full transaction history, identity, NI number and wallet movements to HMRC. The first reports are due to HMRC by 31 May 2027 covering all of calendar 2026.

48 jurisdictions are now in the first wave, with the EU, Channel Islands and South Africa already exchanging. The UAE, Hong Kong, Singapore and Switzerland join in 2027/2028. The US implements in 2028. Offshore crypto is no longer a hiding place. Platform penalties run to £300 per user for inaccurate reporting — pressure that pushes exchanges to verify identities rigorously.

Digital Platform Reporting

Side hustles in the spotlight

eBay, Vinted, Etsy, Airbnb, Uber, Deliveroo and similar platforms report any user crossing 30 transactions or ~£1,700/€2,000 per year. January 2026 marked the completion of HMRC's first full data cycle, and Connect is actively cross-referencing this against 2024/25 Self Assessment returns.

The £1,000 trading allowance still protects genuine casual sellers. But "regular activity with a profit motive" counts as trading — and platforms cannot tell the difference for you, so they report everything. Selling a few old jumpers? Likely fine. A reselling side business? Declarable.

Common Reporting Standard (CRS)

Global bank data sharing

Over 100 countries share UK residents' foreign account data with HMRC automatically. Offshore interest, foreign rentals, overseas dividends — all visible. Combined with CARF for crypto, the offshore loophole is effectively closed for most ordinary taxpayers.

Deliberate offshore non-compliance can be assessed up to 20 years back with penalties of up to 200% of unpaid tax, plus public naming for serious cases over £25,000. The Worldwide Disclosure Facility (WDF) remains the recommended route for voluntary correction — penalties typically reduce to 30% or less for prompted disclosures.

Cross-Government Data Sharing

Property & lifestyle matching

HMRC routinely matches Land Registry, council tax, DVLA, tenancy deposit schemes, Companies House and DWP records. A second home registered for council tax but absent from your tax return is one of the most common rental-income triggers.

The Let Property Campaign remains open. In 2025/26 it resolved over £100m in undeclared rental income. Voluntary disclosure typically caps penalties at 0–20% versus 30–100% for prompted disclosures after a nudge letter.

Key 2026–2028 Dates Every UK Taxpayer Should Know

The compliance landscape is shifting faster than at any point in the last decade. Use this timeline to plan ahead.

Quick Risk Self-Check

Five questions. Anonymous. No data leaves your browser. Designed to highlight whether your situation contains any of the most common Connect triggers — not a substitute for professional advice.

1. Did you earn money from a digital platform (eBay, Vinted, Airbnb, Etsy, Uber, etc.) in the last 4 years and not declare it on a Self Assessment?

2. Have you received rental income from any UK or overseas property without declaring it (or partial declaration)?

3. Have you bought, sold, swapped, staked or earned cryptocurrency (including crypto-to-crypto) without reporting capital gains or income?

4. Do you hold any foreign bank account, foreign investment or foreign property generating income?

5. Do you receive any regular cash income (tutoring, trades, services) not run through a payroll or invoiced through a business account?

Your risk indicator

Indicative Penalty Estimator

HMRC penalties depend on three factors: how much tax is unpaid, the taxpayer's behaviour, and whether disclosure is voluntary (unprompted) or prompted by HMRC. This tool gives an indicative range only — real cases vary.

⚠️ Indicative only. Plus interest on unpaid tax (currently ~7.75% p.a.) and possible prosecution in serious cases. Always speak to a qualified tax adviser before making a disclosure.

Frequently Asked Questions

I've received a "nudge letter" from HMRC. What should I do?

Do not ignore it. Nudge letters are pre-investigation prompts — HMRC already holds data suggesting a possible discrepancy. Review your records for the years in question, gather supporting documents and respond by the deadline. If tax is genuinely owed, use the Digital Disclosure Service or Let Property Campaign for the lowest penalties. If unsure, speak to a tax adviser before replying — the tone of your first reply can shape the entire case.

How far back can HMRC go to assess unpaid tax?

It depends on behaviour: 4 years for genuine mistakes ("reasonable care taken"), 6 years for careless errors, 12 years for offshore non-compliance, and 20 years for deliberate evasion. Voluntary unprompted disclosure typically attracts the shortest lookback window and the lowest penalty.

I only sold a few items on Vinted/eBay last year. Do I really need to declare?

The £1,000 trading allowance covers casual sellers, and selling personal items below their original price is usually not taxable. But if you're buying to resell, making things to sell, or earning over £1,000 from platform activity, you need to register for Self Assessment by 5 October following the tax year. Platforms now report your totals regardless, so it's safer to declare and apply allowances than to assume HMRC won't notice.

I haven't declared crypto gains from previous years. Am I in trouble?

Not necessarily — but act now. The Cryptoasset Disclosure Service (CDS) and Digital Disclosure Service allow voluntary unprompted disclosure with significantly reduced penalties. With CARF live since January 2026, the first wave of crypto data reaches HMRC by May 2027. Disclosing before HMRC contacts you is almost always cheaper and less stressful than waiting for a nudge letter.

What income falls under MTD for Income Tax from April 2026?

Combined gross income from self-employment and/or property — before deducting expenses — above £50,000 for 2024/25 puts you in MTD from 6 April 2026. The threshold drops to £30,000 from April 2027 and £20,000 from April 2028. You'll need MTD-compatible software, quarterly digital updates, and a final annual declaration replacing your old Self Assessment.

Is voluntary disclosure really better than waiting?

Almost always, yes. Unprompted careless disclosure can attract a 0% penalty in some cases (max 30%). The same case discovered by HMRC after a nudge can attract 15–30% (max 30%). For deliberate behaviour, prompted penalties rise to 70–100% (or 200% offshore). Plus, voluntary cases rarely escalate to criminal investigation — prompted ones sometimes do.

Can HMRC really see my bank account?

HMRC does not have routine real-time access to UK bank balances, but it can require banks to disclose information under formal notices, and banks must already report suspicious activity automatically under anti-money-laundering law. From January 2026, financial institutions also share data on interest and certain transactions. Connect builds a picture from many sources, not just bank statements.

If anything in this widget sounds familiar to your situation, the best move is almost always a quick conversation with a qualified UK tax adviser before any letter arrives.

Educational content — not personal tax advice. Sources: HMRC Measuring Tax Gaps 2025, Finance Act 2024 / 2025, OECD CARF, ICAEW Tax Faculty, GOV.UK guidance, HMRC Employer Bulletin Feb 2026. Verify any figure on gov.uk before acting.

Advanced HMRC Tactics: Sector-Specific Strategies to Dodge Undeclared Income Pitfalls

We’ve mapped the basics and armed you with audits; now, let’s level up to the chess game HMRC plays with high-risk sectors. With the tax gap’s £35.8 billion “hidden economy” slice – think cash trades and offshore slips – under AI scrutiny, 2025/26 sees targeted campaigns ramping up, like the 5,500 new compliance staff announced in the Spending Review. For landlords facing 10,000 more Let Property probes or gig workers hit by platform reports, ignoring this is like playing hide-and-seek in a glass house. Drawing from client war stories, this part delivers advanced, sector-tailored guidance: from offshore disclosures to evasion-proofing businesses. We’ll keep it logical, layering in caveats like “consult a pro for complexities,” to build your savvy without overwhelm. Ready to outthink the system ethically? Let’s dive.

Rental Income Radar: Why Landlords Are HMRC’s 2025 Prime Targets

If you’re letting a flat in Edinburgh or a room in Birmingham, know this: HMRC’s radar is locked on, using Land Registry cross-checks with bank flows to spot £100 million in undeclared yields yearly. Post-2025 rules, Airbnb et al. report hosts earning over £2,300 direct, blending with tenancy deposit schemes for a full picture. The advanced play? Quarterly reconciliations via MTD for ITSA (Income Tax Self Assessment), due fully by April 2026 – think of it as your property’s heartbeat monitor, flagging voids or repairs for deductions.

Consider Elena, a solicitor I advised who inherited a buy-to-let; her £8,000 undeclared profit from 2022 stemmed from forgetting to offset mortgage interest (now at 20% basic rate relief). We used the Let Property Campaign’s amnesty – penalties capped at 10% if voluntary – and reclaimed £1,200. Key concept: Profit vs. income – declare gross rents first, then deduct allowable costs like agent fees (up to 100% relief). For verification, review gov.uk/government/publications/let-property-campaign; it’s got worksheets to model your exposure. Caveat: If offshore-owned, loop in the Worldwide Disclosure Facility early – delays hike penalties to 200%.

Gig and Freelance Fortification: Navigating Platform Reports and Cash Traps

Gig economy? HMRC’s 2025 crackdown means Uber payouts and Etsy sales are no longer ghosts – platforms file by 31 January annually, covering 2024 data. Advanced strategy: Segregate accounts – one for gigs, tracked via apps like QuickBooks Self-Employed, which auto-categorises for MTD submissions. Cash traps? They’re the sneaky bit; with AI spotting “unusual patterns” like round-sum deposits, log everything with invoices, even for mates’ rates.

I helped freelance photographer Ollie last month; his £12,000 in cash weddings mismatched his £25,000 declared salary, flagged by Connect’s bank scans. We fortified with a “cash log template” (free from Companies House resources), proving 80% went to kit – slashing his liability by £2,000. Pro insight: Use the £1,000 trading allowance wisely, but exceed it? Register for Self Assessment by 5 October. Check gov.uk/working-for-yourself for templates; it’s practical gold. As an aside, if you’re in creative fields, ICAEW’s sector guides add nuance – worth a peek for those grey-area deductions.

Offshore and Evasion Evasion: High-Stakes Plays for Global Earners

For the jet-setters with foreign dividends or crypto stashes, HMRC’s Common Reporting Standard (CRS) exchanges data with 100+ countries, unearthing £1 billion in undeclared assets since 2017. Advanced tactic: Annual CRS self-reviews – list overseas accounts on your return, claiming double-tax relief via gov.uk’s treaty finder. Evasion? It’s the nuclear option; deliberate cases draw 20-year lookbacks and “name and shame” for over £50,000.

A client like Alex, with undeclared Dubai rentals, faced this head-on; voluntary disclosure via WDF cut his 75% penalty to 30%, plus interest. Key: Behaviour grading – “prompted” disclosures (post-nudge) sting more. Verify at gov.uk/government/publications/offshore-penalties-why-we-are-doing-this – it details transparency tiers by jurisdiction. Remember, this is for education; complex cases scream for a tax adviser to avoid missteps.

Integrating AI Insights: Future-Proofing Your Compliance in an Algorithmic Age

As HMRC’s AI evolves – now behavioural profiling via Connect – advanced users simulate flags with open-source tools like Python scripts for pattern analysis (ethically, of course). But practically: Annual “what-if” reviews, blending MTD data with lifestyle trackers. From experience, this nips 90% of issues. For more, explore HMRC’s AI ethics page at gov.uk – transparent and forward-thinking.

These strategies aren’t shields against honesty, but bridges to it – empowering you in a system that’s fairer when we’re all in it together.

Summary of Key Points

- Core Detection Foundations: HMRC’s Connect AI and third-party reports form the backbone, closing £46.8 billion of the 2023/24 tax gap, with undeclared income at £6.5 billion – act via gov.uk/undeclared-income for leniency.

- Practical Auditing Essentials: Reconcile streams, use disclosure tools, and spot flags with checklists to amend returns penalty-free within 12 months.

- Sector Strategies: Tailor for rentals (Let Property Campaign), gigs (platform tracking), and offshore (CRS disclosures) to leverage reliefs and cap penalties at 0-30%.

- Overall Ethos: Voluntary steps build trust; verify all at gov.uk for 2025/26 compliance amid MTD expansions.

FAQs

Q1: What should I do if I receive a nudge letter from HMRC about possible undeclared income?

A1: Well, it’s worth noting that these letters are more of a gentle tap on the shoulder than a full-blown alarm – they’re HMRC’s way of saying they’ve spotted a potential mismatch without jumping straight to penalties. In my experience with clients, the key is to respond promptly within the 60-day window they give you; log into your personal tax account online or call their helpline to explain your side. Take young Emma from Bristol, who got one for forgotten freelance gigs – she gathered her invoices, showed it was a simple oversight, and amended her return on the spot, avoiding any fines. Don’t ignore it, though; that escalates things. Just treat it as a chance to clear the air, and remember, voluntary fixes often mean lighter consequences.

Q2: How does HMRC handle undeclared income from multiple jobs, especially if I’m PAYE?

A2: Ah, the classic double-job dilemma – it’s a common mix-up for folks juggling a full-time role with evening shifts, and HMRC’s got eyes on it through your P60s and employer reports. If your total earnings nudge you over the personal allowance, they’ll adjust via your tax code or a simple assessment. I’ve seen this snag clients like Mark, a London teacher moonlighting as a delivery driver; his second job’s income wasn’t coded right, leading to a £400 underpayment surprise. The fix? Use the online tax checker tool to simulate your total, then request a code tweak from HMRC – it’s straightforward and stops overpayments too. Pro tip: Keep payslips handy; they make reconciliation a breeze.

Q3: Are there regional differences in how HMRC detects undeclared income in Scotland versus England?

A3: In my practice, I’ve noticed Scottish taxpayers often fret about this because of devolved income tax bands, but detection methods are uniform UK-wide – it’s all fed into the same Connect system. The twist comes in calculations: Scotland’s rates kick in differently for 2025/26, so a £45,000 earner might owe more there than south of the border. Consider Fiona in Glasgow, whose undeclared consulting fees pushed her into a higher starter band; HMRC flagged it via bank data, but we adjusted using Revenue Scotland’s calculator for a fairer outcome. Always double-check your banding on their joint site – it saves headaches and ensures you’re not caught out by postcode politics.

Q4: Can HMRC detect undeclared crypto gains, and what if I’ve traded on foreign exchanges?

A4: Crypto’s the wild west of income, isn’t it? HMRC’s ramped up tracking since 2025, pulling data from UK exchanges and international swaps under CRS agreements – they even issued 10,000 crypto-specific nudges last year. If you’ve got gains over the £3,000 allowance, undeclared trades can ping their radar via wallet addresses linked to your NI number. Picture Alex, a Manchester developer who forgot his Bitcoin flips; a routine bank transfer to a fiat account triggered a review, but disclosing voluntarily halved his penalty. My advice? Log everything in a simple spreadsheet and use their capital gains tool – transparency turns a potential pitfall into a non-event.

Q5: What happens if undeclared income is discovered after someone’s death?

A5: It’s a delicate spot, handling a loved one’s affairs, and HMRC approaches it with a bit more leeway than live cases. Executors must review records for the final years, declaring any missed income on the estate’s return – but penalties are rare if it’s unintentional. I once guided a widow in York through her late husband’s overlooked pension lump sum; we used the Worldwide Disclosure route, settling just the tax due without extras, as records showed no deliberate hiding. Start by notifying them of the death promptly, then sift through statements together – it’s emotional, but getting it right honours their legacy without added stress.

Q6: How can self-employed sole traders avoid HMRC flagging irregular deposits as undeclared income?

A6: Irregular cash flows are the bane of sole traders – one month booming, the next a drought – and HMRC loves spotting those lumpy deposits against your flat Self Assessment. The trick is consistent banking: funnel everything through a dedicated business account, tagging transfers clearly. Think of Raj, my Birmingham client whose handyman fees looked dodgy until we reconciled them with client logs; it smoothed his profile and dodged a nudge. For 2025/26, with MTD quarterly reporting, set up auto-categorisation in your accounting app – it’s like giving HMRC a tidy diary instead of a puzzle, keeping you off their watchlist effortlessly.

Q7: Does social media activity really tip off HMRC to undeclared side hustles?

A7: You’d be surprised how often a casual Instagram post about your “craft fair haul” leads to questions – HMRC’s analysts do scan public profiles for lifestyle clues that clash with declared earnings, especially in targeted campaigns. It’s not Orwellian surveillance, just pattern-matching: flashy holidays on a basic-rate salary? Red flag. I recall advising Sarah, whose Etsy success photos mismatched her nil returns; a quick voluntary tweak sorted it before escalation. Keep posts vague or private if you’re hustling – and better yet, declare properly. It’s a reminder that in the digital age, your online brag book is as public as your bank statement.

Disclaimer

The information provided in this article is for general guidance only and is not intended to constitute professional advice, tax advice, financial advice, legal advice, or any other form of regulated guidance. Although every effort has been made to ensure accuracy at the time of publication, Fair View Accounting Services, including its director, employees, contractors, writers, and content-creation team, accepts no responsibility for any loss, damage, penalty, or consequence arising from reliance on the information contained herein.

UK tax legislation changes frequently, and HMRC interpretations, thresholds, and rules may vary depending on the individual circumstances of each taxpayer. Nothing in this article should be considered a substitute for obtaining formal, personalised advice from a qualified accountant or tax professional. Readers should not take action—or refrain from taking action—based solely on the content published on this website.

Fair View Accounting Services does not guarantee the completeness, accuracy, or ongoing validity of the information provided and assumes no liability for omissions or errors, whether typographical, factual, or technical. By using this content, the reader acknowledges that all responsibility for decisions remains solely with the user.