Do Sole Traders Have Company Registration Numbers in the UK?

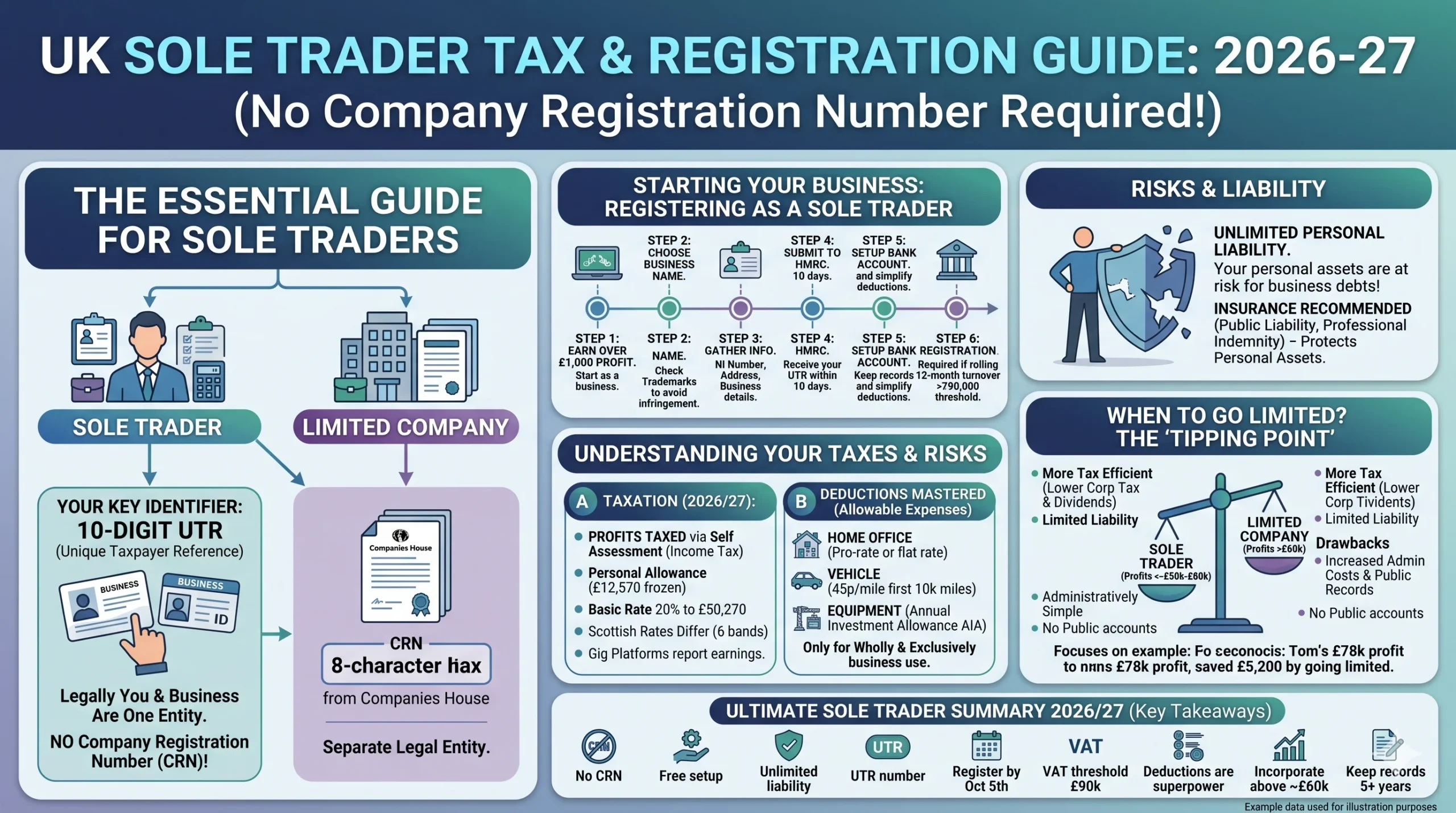

Many individuals transitioning into self employment frequently ask whether they need a company registration number. As a tax accountant based in Manchester with 14 years of experience, I regularly advise tradespeople and creatives on this exact issue. The definitive answer is no; sole traders do not have company registration numbers in the UK. However, understanding what identifiers you do need and how to remain compliant with HM Revenue and Customs is crucial.

As of 2026, there are approximately 4 million sole traders in the UK, representing a significant portion of the business landscape. The structure is accessible because it avoids formal incorporation. Based on recent Self Assessment statistics, millions of sole traders file returns annually. For the 2026/27 tax year, the personal allowance remains frozen at £12,570. The basic rate stays at 20% on income up to £50,270, and Class 4 National Insurance contributions are set at 6% on profits between £12,571 and £50,270. Scottish residents have a different system, with a starter rate of 19% up to £15,397 and an intermediate rate of 21% up to £43,662. Welsh tax bands currently align with England, but taxpayers should always verify their position via their personal tax account.

This guide explains the identifiers you need, how to register, and common compliance pitfalls to avoid.

Why Sole Traders Skip the Company Registration Number

A Company Registration Number is an eight character alphanumeric identifier issued by Companies House, reserved exclusively for limited companies and Limited Liability Partnerships. It serves as proof that a business is a separate legal entity. As a sole trader, you and your business are legally the same entity, meaning no separation exists and therefore no Company Registration Number is issued. HM Revenue and Customs defines a sole trader as a self employed individual who runs their own business.

Avoiding Companies House registration means you are exempt from filing annual confirmation statements, publishing public accounts, and paying incorporation fees. Many professionals choose this route for its administrative simplicity.

However, lacking a Company Registration Number does not mean you operate without oversight. Sole traders have unlimited liability, meaning personal assets are at risk for business debts. For tax purposes, profits are declared via the annual Self Assessment system rather than corporation tax. For 2026/27, this involves paying income tax at your marginal rate plus Class 4 National Insurance. Class 2 National Insurance is now voluntary for most, but some pay the weekly £3.65 to protect state pension entitlement.

Comparison of Business Structures

- Registration Body: HMRC for Sole Traders; Companies House and HMRC for Limited Companies.

- Identifier: UTR (10 digits) for Sole Traders; CRN (8 characters) and CT UTR for Limited Companies.

- Setup Cost: Free for Sole Traders; £12 online for Limited Companies.

- Liability: Unlimited personal liability for Sole Traders; Limited to shares for Limited Companies.

- Tax on Profits: Income Tax and National Insurance for Sole Traders; Corporation Tax and dividend tax for Limited Companies.

- 2026/27 Thresholds: Personal Allowance £12,570 for Sole Traders; Corporation Tax 19% up to £50,000 for Limited Companies.

- Filing Requirements: Annual Self Assessment for Sole Traders; Annual accounts and Corporation Tax return for Limited Companies.

- Public Records: None for Sole Traders; Full business details available on Companies House for Limited Companies.

For profits under £50,000, the sole trader structure can be highly tax efficient. However, as profits scale, corporation tax rates may become more favourable.

The Unique Taxpayer Reference and Essential Identifiers

Without a Company Registration Number, you prove your legitimate trading status using a Unique Taxpayer Reference. This 10 digit number is issued automatically when you register for Self Assessment and is essential for filing returns and claiming expenses. You can locate your Unique Taxpayer Reference via your personal tax account or by contacting HM Revenue and Customs.

It is critical to keep this number secure. Missing or losing it can delay your tax filings, potentially resulting in late penalties.

If your rolling 12 month turnover exceeds the £90,000 threshold for 2026/27, you must also register for Value Added Tax. A VAT registration number is nine digits long. For international trade, an Economic Operators Registration and Identification number is required.

Registering as a Sole Trader in 2026 to 2027

The registration process is straightforward. Ensure you complete these steps carefully:

- Assess Your Readiness: If you earn over £1,000 in a tax year from self employment, you must register by 5 October following the end of the tax year.

- Choose Your Name Wisely: You cannot use terms like Limited or Ltd. Check existing trademarks via the official government checker to avoid infringement.

- Gather Documentation: You need your National Insurance number, home address, and business details.

- Submit to HM Revenue and Customs: Register online to receive your Unique Taxpayer Reference, typically within 10 working days.

- Set Up Banking and Records: Opening a dedicated business bank account simplifies record keeping and expense tracking.

- Plan for VAT: Monitor your turnover and register 30 days before breaching the £90,000 threshold.

- File Your Return: Ensure your Self Assessment is filed and paid by 31 January following the tax year end.

Registration Checklist

- Unique Taxpayer Reference received and stored securely.

- Business name checked for trademark conflicts.

- National Insurance contributions up to date.

- Basic record keeping system in place for invoices and receipts.

- Turnover projection monitored against the £90,000 VAT threshold.

- Emergency tax fund established, aiming to save 25% to 30% of profits.

- Public liability insurance arranged.

UK Sole Trader vs Limited Co.

The 2026/27 Tax Year Blueprint

Do you really need a Company Registration Number?

Do Sole Traders have a Company Registration Number (CRN)?

Sole traders and their businesses are the same legal entity. There is no separation, so no Companies House registration or CRN is required.

What do you need instead?

The UTR (10 Digits)

Unique Taxpayer Reference. This is your official ID for HMRC.

- Used for Self Assessment.

- Issued automatically on registration.

VAT Number (9 Digits)

Required only if rolling 12-month turnover exceeds £90,000.

- Must register within 30 days.

- Allows claiming input VAT.

The 2026/27 Structural Showdown

Sole Trader

Limited Company

The Incorporation Tipping Point

When does trading your UTR for a CRN become tax efficient?

Simpler admin usually outweighs minor tax savings.

Corporation tax & dividend structure becomes highly favourable.

Crucial Admin Checklist

-

1

Registration Deadline

Register by 5 October following the end of the tax year in which earnings exceeded the £1,000 trading allowance.

-

2

Record Keeping

Keep all financial records (invoices, receipts, bank statements) for a minimum of five years after the 31 January submission deadline.

-

3

Risk Management

Because of unlimited liability, securing Public Liability Insurance is strongly advised, even though it's not legally mandatory.

Tax Strategies and Managing Variable Incomes

Earning above the basic rate threshold requires proactive tax planning. In the 2026/27 tax year, profits are treated as personal income. Multiple income streams, such as a concurrent part time job, complicate the calculation.

Tax Bands (England, Wales, Northern Ireland)

- Personal Allowance: £0 to £12,570 at 0%

- Basic Rate: £12,571 to £50,270 at 20%

- Higher Rate: £50,271 to £125,140 at 40%

- Additional Rate: Over £125,140 at 45%

- Class 4 NI: £12,571 to £50,270 at 6%

It is vital to ensure your tax code accurately reflects all income sources. If you have a primary employment income, your Personal Allowance may be entirely utilised there, meaning all sole trader profits are taxed at the basic or higher rate.

Payments on account often catch new business owners off guard. If your previous tax bill exceeded £1,000, HM Revenue and Customs requires advance payments towards the next year, due in January and July.

Allowable Business Deductions

Claiming allowable expenses reduces your taxable profit. You must keep accurate records to support these claims.

- Home Office: Requires a Council tax bill and floor plan. A common error is claiming full rent if the space is shared.

- Travel (Mileage): Requires a mileage log with dates and purpose. A common error is forgetting to log return journeys.

- Phone and Internet: Requires an itemised bill showing business usage. A common error is claiming 100% of a personal mobile contract.

- Training: Requires invoices showing relevance to your trade. A common error is claiming unrelated subscriptions.

- Equipment: Requires receipts for capital items. A common error is forgetting the Annual Investment Allowance.

- Marketing: Requires invoices for advertising and hosting. A common error is mixing personal social media costs.

You can use the £6 per week flat rate for home office expenses or calculate the actual proportion of utilities used. For vehicles, claiming 45p per mile for the first 10,000 miles is often more straightforward than calculating exact running costs.

Do Sole Traders Have a Company Registration Number?

The definitive answer for UK taxpayers in 2026/27

Sole traders do not receive a Company Registration Number (CRN)

CRNs are issued exclusively by Companies House to limited companies and LLPs. As a sole trader, you and your business are the same legal entity.

As of 2026: ~4 million sole traders in the UK. Simple setup, unlimited liability, profits taxed via Self Assessment.

| Feature | Sole Trader | Limited Company |

|---|---|---|

| Registration Body | HMRC only | Companies House + HMRC |

| Identifier | UTR (10 digits) | CRN (8 chars) + CT UTR |

| Setup Cost | Free | £12 online |

| Liability | Unlimited (personal assets at risk) | Limited to company shares |

| Tax on Profits | Income Tax + Class 4 NI | Corporation Tax (19-25%) + Dividends |

| Public Records | None | Full details on Companies House |

Tip: Sole trader often better for profits under £50k–£60k. Consider incorporation above that.

Register with HMRC by 5 Oct following tax year

Usually within 10 working days

£90,000 rolling 12 months

6 years recommended

£0 – £12,570 (0%)

£12,571 – £50,270 (20%)

£50,271 – £125,140 (40%)

Over £125,140 (45%)

Class 4 NI: 6% between £12,571–£50,270. Scottish rates differ.

The Incorporation Tipping Point and Compliance

As profits increase, operating as a sole trader may become less tax efficient. The decision to incorporate and obtain a Company Registration Number usually becomes viable when annual profits consistently exceed £50,000 to £60,000.

Evaluating the Financial Benefit of Incorporation

Operating as a limited company allows you to extract profits through a combination of a low salary and dividends. For 2026/27, the dividend allowance is £500, with basic rate dividends taxed at 10.75% and higher rate dividends at 35.75%.

While a limited company might incur a corporation tax rate of 19% on profits up to £50,000 (increasing to 25% for profits over £250,000), the overall tax burden is often lower than the combined income tax and Class 4 National Insurance paid by a sole trader at the same profit level. Additionally, incorporation provides limited liability, protecting your personal assets from business creditors.

However, incorporation introduces additional administrative burdens and accountancy fees. You must balance the estimated tax savings against the increased operational costs.

Key Regulatory Considerations for 2026/27

The High Income Child Benefit Charge affects households where one partner earns above £60,000. Benefit is gradually withdrawn, reaching full clawback at £80,000. Operating through a limited company allows owners to manage their personal income to retain this benefit.

Gig economy workers should be aware that digital platforms now report earnings directly to HM Revenue and Customs. Discrepancies between platform data and your Self Assessment will trigger an investigation.

FAQs

Q1: Do sole traders need to register their business name separately in the UK?

A1: You are not required to formally register your business name. However, you must ensure your chosen name does not infringe on existing trademarks by checking the Intellectual Property Office register.

Q2: What happens if a sole trader exceeds the VAT threshold unexpectedly?

A2: If your 12 month rolling turnover exceeds £90,000 in 2026/27, you must register for Value Added Tax within 30 days. You must then charge VAT on your services and can reclaim input VAT on allowable business expenses.

Q3: Can a sole trader operate under multiple business names?

A3: Yes, you can run multiple businesses under different names. It is critical to maintain separate accounting records for each to ensure accurate tax reporting.

Q4: Is there a deadline for registering as a sole trader after starting?

A4: You must register for Self Assessment by 5 October following the end of the tax year in which your self employment income exceeded the £1,000 trading allowance.

Q5: Do sole traders in Scotland face different registration rules?

A5: Registration is handled centrally by HM Revenue and Customs across the UK. However, Scottish residents are subject to different income tax bands, such as the 21% intermediate rate, which will impact your total tax liability.

Q6: What if a sole trader wants to protect their business name without incorporating?

A6: You can register a trademark through the Intellectual Property Office. This provides legal protection against competitors using a similar name, which domain registration alone does not offer.

Q7: Can non UK residents set up as sole traders in the UK?

A7: Yes, provided they hold the appropriate visa that permits self employment. Tax residency rules apply, and you may still be liable for UK tax on income generated within the country.

Q8: How does a sole trader handle registration if they have a primary employment?

A8: You declare your self employment income alongside your employment income on your Self Assessment return. Ensure HM Revenue and Customs has your correct tax code to avoid overpaying tax.

Q9: What records must sole traders keep without a Company Registration Number?

A9: You must retain all financial records, including invoices, bank statements, and receipts, for a minimum of five years after the 31 January submission deadline of the relevant tax year.

Q10: Do sole traders need insurance without formal registration?

A10: While not legally mandatory, public liability and professional indemnity insurance are strongly advised. As a sole trader, you have unlimited liability, meaning your personal assets are at risk in the event of a legal claim.

Disclaimer

The information provided in this article is for general guidance only and is not intended to constitute professional advice, tax advice, financial advice, legal advice, or any other form of regulated guidance. Although every effort has been made to ensure accuracy at the time of publication, Fair View Accounting Services, including its director, employees, contractors, writers, and content-creation team, accepts no responsibility for any loss, damage, penalty, or consequence arising from reliance on the information contained herein.

UK tax legislation changes frequently, and HMRC interpretations, thresholds, and rules may vary depending on the individual circumstances of each taxpayer. Nothing in this article should be considered a substitute for obtaining formal, personalised advice from a qualified accountant or tax professional. Readers should not take action—or refrain from taking action—based solely on the content published on this website.

Fair View Accounting Services does not guarantee the completeness, accuracy, or ongoing validity of the information provided and assumes no liability for omissions or errors, whether typographical, factual, or technical. By using this content, the reader acknowledges that all responsibility for decisions remains solely with the user.