Could your 2026 tax refund be blocked simply because your digital records don’t match HMRC’s new real-time expectations? For many subcontractors, a cis repayment claim represents a vital injection of cash, yet the introduction of Making Tax Digital for Income Tax this April has added a new layer of complexity. It’s frustrating to see your hard-earned money held by the Revenue, especially when you’re trying to manage site costs and payroll. You’ve likely felt the pressure of stricter fraud checks and the return of mandatory nil returns, which only adds to the stress of getting your submission right.

We’ve designed this guide to strip away that confusion and give you total confidence in your claim. By following our comprehensive checklist, you’ll learn how to align your records with the latest 2026 standards, avoid the red flags that trigger investigations, and secure your repayment without the typical delays. From understanding the new £50,000 threshold for digital reporting to mastering your monthly audit trail, we’ll ensure you stay compliant and keep your cash flow moving.

Key Takeaways

- Learn how to accurately calculate your cis repayment claim by offsetting deductions against Corporation Tax or PAYE liabilities first.

- Discover the essential pre-claim steps to verify your contractor vouchers and ensure your UTR details match HMRC’s records perfectly.

- Navigate the 2026 digital requirements with ease, including the reinstatement of mandatory nil returns and new software standards.

- Identify the common administrative errors that trigger HMRC investigations and learn how to avoid them through methodical record-keeping.

- Streamline your path to a faster refund by using cloud-based tools that keep your financial data organised and ready for submission.

Understanding the CIS Repayment Claim: Why Refunds Occur

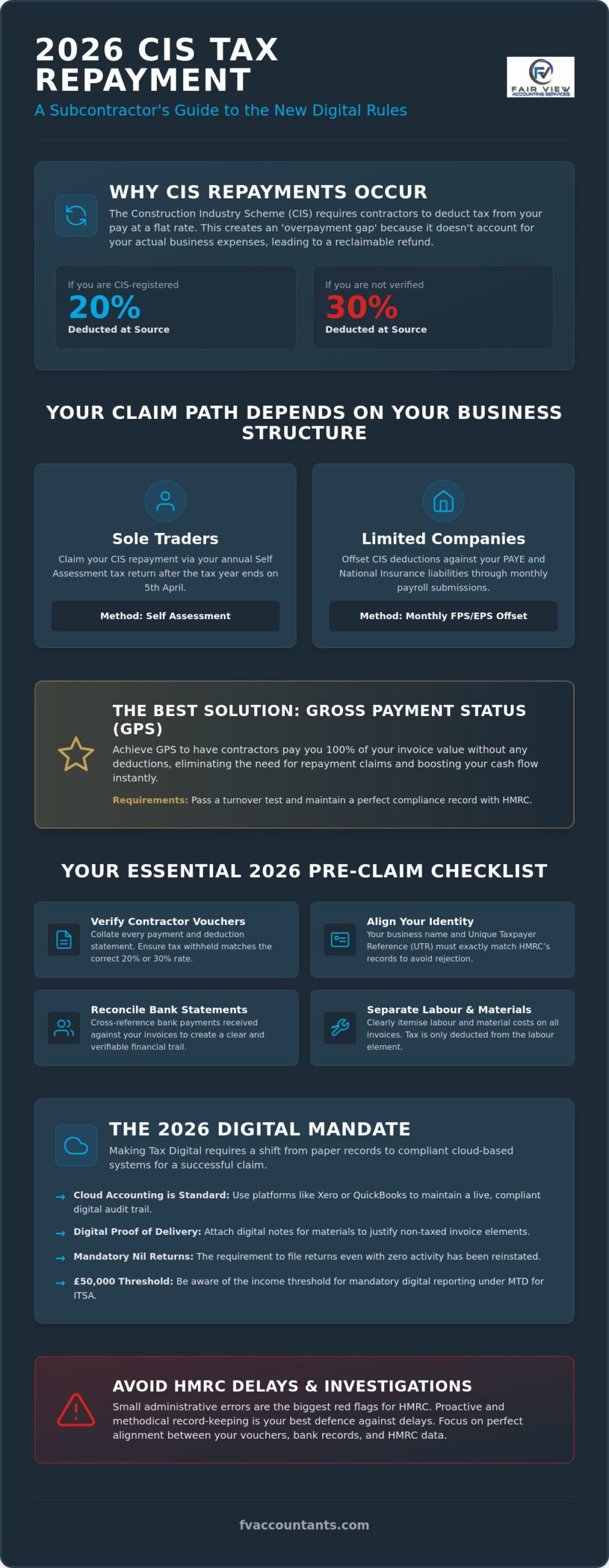

A cis repayment claim is the mechanism to recover cash flow lost to flat-rate tax withholding. Under the Construction Industry Scheme, contractors are legally required to deduct tax at source before they settle your invoices. If you have provided a valid Unique Taxpayer Reference (UTR), they deduct 20%. If you are not registered or cannot be verified, this rate climbs to 30%. These deductions apply specifically to the labour element of your work, yet they are calculated based on your gross pay before any of your own business costs are considered.

This creates what is known as the ‘overpayment gap’. Because these flat rates do not account for your overheads, such as insurance, vehicle running costs, or administrative expenses, the amount HMRC holds is frequently higher than the actual tax you owe on your net profit. Essentially, a cis repayment claim is a formal request to HMRC to refund the tax deducted from your payments that exceeds your actual liability. It ensures that money which should be supporting your business operations is returned to your accounts rather than sitting in the government’s coffers.

Sole Traders vs. Limited Companies: Different Claim Paths

Your business structure dictates how and when you can access your refund. Sole traders usually claim via their Self Assessment tax return after the tax year concludes on 5 April. Limited companies, however, follow a more integrated route. They must claim through their monthly Full Payment Submission (FPS) and Employer Payment Summary (EPS), offsetting CIS deductions against their own PAYE or Corporation Tax liabilities. This distinction is vital for your 2026 cash flow planning, as it determines how quickly you can reinvest that capital into new projects.

The Role of Gross Payment Status

Qualifying for Gross Payment Status (GPS) is the most effective way to eliminate the need for future repayment claims. When you hold GPS, contractors pay you in full without any deductions, keeping 100% of your earnings in your business from day one. To qualify in 2026, you must pass a turnover test and maintain a clean compliance record with HMRC. Demonstrating that you pay your taxes and file your returns on time is the best way to move away from the cycle of waiting for refunds.

Pre-Claim Checklist: Essential Documentation and Data

Success with your cis repayment claim depends entirely on the quality of your evidence. HMRC’s 2026 anti-fraud measures are more rigorous than ever, meaning small discrepancies can lead to lengthy delays or formal enquiries. Before you begin the submission process, you must ensure your records are “HMRC-ready” by verifying the following:

- Contractor Vouchers: Collate every CIS payment and deduction statement. Ensure they are correct and that the tax withheld matches the expected 20% or 30% rates.

- Identity Alignment: Your business name and Unique Taxpayer Reference (UTR) must match HMRC’s records exactly. Even a minor spelling variation can trigger a system rejection.

- Bank Reconciliation: Cross-reference your bank statements against your invoices to confirm the net payments received. This provides a clear trail of the money that actually hit your account.

- Labour vs Materials: Clearly separate material costs from labour on every invoice. Since tax is only deducted on labour, accurate bookkeeping here prevents you from overpaying tax in the first place.

The Digital Audit Trail

In 2026, paper-based systems are no longer sufficient. Cloud accounting platforms like Xero or QuickBooks are now the standard for maintaining your primary evidence. These tools allow you to attach “Proof of Delivery” notes for materials, which justifies the non-taxed elements of your invoices during a cis repayment claim. If you need help digitising your records, our team offers specialised bookkeeping for construction to keep your data compliant year-round.

Payroll and P60 Requirements

For limited company directors, the process involves more than just subcontractor data. You must ensure your own salary and National Insurance contributions are correctly logged through payroll. This data directly intersects with your company’s offset claim, as HMRC will first look to settle any outstanding PAYE liabilities. Understanding the specific rules for a CIS refund for limited companies is essential to ensure your P60 information aligns with your year-end figures.

The 5-Step Checklist for a Successful 2026 CIS Claim

Filing a cis repayment claim requires a methodical approach to satisfy HMRC’s digital-first requirements. In 2026, the process is highly automated, meaning your submission must be flawless to avoid being caught in a verification loop. Follow these steps to ensure your refund is processed efficiently:

- Step 1: Finalise your accounts. Before claiming, you must close your year-end books and ensure all 12 monthly CIS returns, including mandatory nil returns, are submitted.

- Step 2: Offset existing liabilities. HMRC requires you to use your CIS credit to settle Corporation Tax or PAYE debts first. Only the remaining balance is eligible for a cash refund.

- Step 3: Submit the formal request. Use the HMRC online portal or instruct a chartered accountant to lodge the claim. Professional submission reduces the risk of administrative errors.

- Step 4: Provide bank details. Ensure your electronic transfer details are current. HMRC has moved away from issuing cheques in 2026, opting for faster, secure digital payments.

- Step 5: Retain your digital records. Keep all supporting vouchers and invoices for at least three years, as HMRC may conduct post-repayment reviews to verify the figures.

Navigating 2026 Anti-Fraud Scrutiny

HMRC’s current automated ‘red flag’ system is designed to spot mismatched deduction figures instantly. If a contractor fails to report the tax they withheld from you, it can stall your cis repayment claim. You have access to a ‘Correction Window’ to fix errors, but acting quickly is essential to prevent a full inquiry. If your records are incomplete or you’ve spotted a discrepancy, you should consult our CIS tax experts to reconcile your accounts before HMRC intervenes.

Verification and Follow-up

Once submitted, you can track the status of your refund through your Business Tax Account. While standard response times in 2026 typically range from four to eight weeks, digital submissions are generally faster than manual reviews. If your claim remains ‘pending’ beyond the standard window, a professional representative can escalate the case with the CIS department to resolve any technical blocks or information requests.

Avoiding HMRC Delays: The Benefits of Professional Oversight

Administrative errors are the most common cause of a stalled cis repayment claim. Mismatched UTRs, incorrect tax periods, and missing contractor details act as immediate red flags within HMRC’s automated systems. When these discrepancies occur, your claim is moved from the fast-track digital lane to a manual review queue, which can add weeks or even months to the process. Ensuring your data is perfect before submission is the only way to maintain your business cash flow.

There is a distinct “Accountant’s Advantage” when dealing with the Revenue. Claims submitted by chartered firms often face less manual scrutiny because HMRC recognises the professional standards applied during the reconciliation process. We act as your tech-savvy guardian, verifying every voucher and invoice to ensure your submission is beyond reproach. If you need to prove your income for a mortgage whilst waiting for a refund, an Accountant’s Certificate can provide the necessary evidence for lenders and financial institutions.

Modernising Your Construction Accounts

Transitioning from manual spreadsheets to automated CIS tracking is a vital step for any growing trade business. Relying on paper records or basic tables often leads to missed deductions and reporting gaps. At Fair View Accounting, we integrate your bank feeds with cloud platforms like Xero or QuickBooks to automate the reconciliation process. This modern approach ensures your cis repayment claim is based on real-time, accurate data, making the final year-end submission a seamless administrative task rather than a stressful hurdle.

Strategic Cash Flow Management

Success in the construction industry requires careful planning for the “tax gap” between your initial deduction and the eventual refund. Whilst the repayment is a welcome boost, relying on it as an emergency fund is risky. We help you implement professional tax planning strategies to reduce your overall liability from the outset. By managing your expenses and deductions proactively, you can keep more cash within your business throughout the tax year, reducing your reliance on the HMRC refund cycle.

Securing Your Financial Future in a Digital Tax Landscape

Navigating the updated 2026 HMRC regulations requires more than just basic bookkeeping; it demands a proactive approach to digital compliance. By maintaining a precise audit trail and reconciling your labour and material costs throughout the year, you protect your business from the automated red flags that often stall progress. A successful cis repayment claim is the result of methodical preparation and a clear understanding of how offset rules apply to your specific business structure.

Fair View Accounting provides the stability you need to manage these complexities with ease. As chartered accountants specialising in CIS compliance, we offer national coverage for UK construction firms and tradespeople. Our expertise in Xero and QuickBooks digital integration ensures your financial data remains seamless and ready for submission at a moment’s notice. We handle the technical intricacies of the HMRC portal so you can focus on your projects on-site.

Take control of your cash flow today and ensure your hard-earned tax deductions are returned to your business without unnecessary friction. Secure your CIS refund with Fair View Accounting's professional support and gain the peace of mind that comes from expert, tech-forward tax management. We are ready to help you build a more organised and tax-efficient future.

Frequently Asked Questions

How long does a CIS repayment claim take in 2026?

Most digital submissions are processed within four to eight weeks, provided there are no discrepancies in your data. If your records trigger a manual review due to mismatched deduction figures or missing contractor information, this timeframe can extend significantly. Using cloud-based software ensures your data is verified before submission, which typically results in a faster electronic transfer directly into your nominated bank account once approved.

Can I claim a CIS refund if I have outstanding tax debts?

You can still file a cis repayment claim if you have outstanding tax debts, but HMRC will automatically use the refund to settle those liabilities first. This includes any overdue Corporation Tax, VAT, or PAYE balances. Only the remaining surplus after these debts are cleared will be issued as a cash payment. It is a methodical way for the Revenue to ensure all tax obligations are met before releasing funds.

What happens if my contractor hasn’t given me a CIS statement?

If a contractor fails to provide a statement, you should first check your HMRC Business Tax Account to see if the deductions have been reported digitally. Contractors are legally required to provide these vouchers; if they don’t, you can use your bank statements and invoices as secondary evidence. We can help you contact the Revenue’s CIS department to reconcile these missing figures and ensure your claim remains accurate and compliant.

Is there a deadline for claiming back my CIS deductions?

The standard deadline for a cis repayment claim is four years from the end of the tax year in which the deductions were made. For work completed in the 2026/27 tax year, you have until 5 April 2031 to submit your request. Whilst this provides a generous window, most construction businesses choose to claim immediately after the tax year ends to maintain healthy cash flow and support ongoing site costs.

Can I claim CIS repayment if my company is in a loss-making position?

Yes, you are eligible for a full cis repayment claim if your company is in a loss-making position, provided you have no other tax liabilities to offset. Because CIS deductions are advance tax payments, a business loss means you have no actual tax liability to satisfy for that period. This makes the entire withheld amount refundable, providing an essential cash injection to help sustain your operations during difficult trading periods.

Article by

Adnan Khalid

Qualified chartered accountant with years of experience in small business accounting & taxes.

Disclaimer

The information provided in this article is for general guidance only and is not intended to constitute professional advice, tax advice, financial advice, legal advice, or any other form of regulated guidance. Although every effort has been made to ensure accuracy at the time of publication, Fair View Accounting Services, including its director, employees, contractors, writers, and content-creation team, accepts no responsibility for any loss, damage, penalty, or consequence arising from reliance on the information contained herein. UK tax legislation changes frequently, and HMRC interpretations, thresholds, and rules may vary depending on the individual circumstances of each taxpayer. Nothing in this article should be considered a substitute for obtaining formal, personalised advice from a qualified accountant or tax professional. Readers should not take action or refrain from taking action based solely on the content published on this website. Fair View Accounting Services does not guarantee the completeness, accuracy, or ongoing validity of the information provided and assumes no liability for omissions or errors, whether typographical, factual, or technical. By using this content, the reader acknowledges that all responsibility for decisions remains solely with the user.